POST-FRAME CONSTRUCTION DATA

Post-frame construction is the modern descendent of timber framing, but it offers far more functionality and design flexibility. The growth of this market segment shows clearly in the data from the Shield Wall Media Construction Survey Insight (CSI) data, as well as reports from people working in the market, such as Todd Carlson, president, A.J. Manufacturing Inc., Bloomer, Wis., and Mark Stover, president, Perma-Column LLC, Ossian, Ind., who says, “It appears the post-frame industry … has continued to outpace the market even with high but steady interest rates.”

Carlson says, “The overall economy has provided both opportunity and challenge. The negative impacts of policies that are more globally friendly and a less fair playing field has been difficult for our raw material suppliers and our intentions to remain substantially American made and sourced. The opportunities have come from our consumer economy and the flow of resources during the pandemic.”

Characteristics of Post Frame Industry

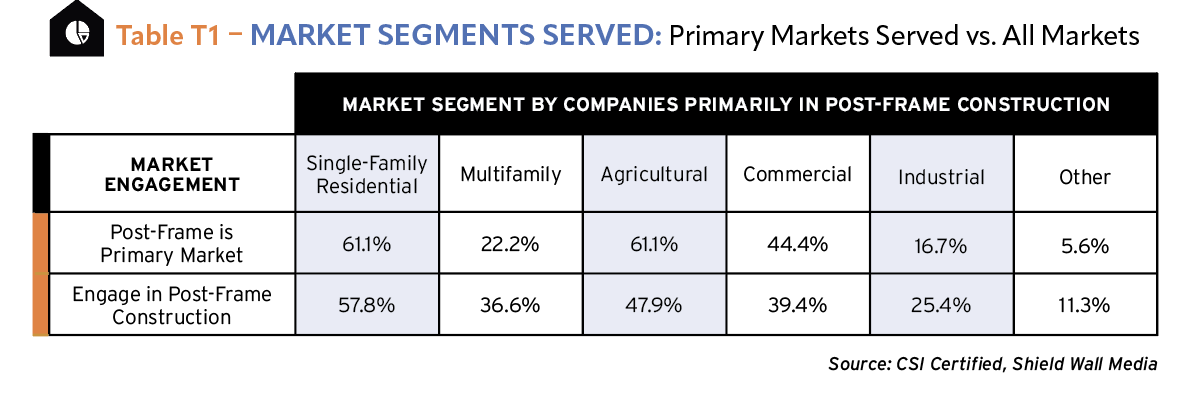

Companies that work in post-frame construction, whether they are contractors, distributors, designers, or manufacturers serve all the market segments. For those who say they are primarily in post-frame construction, the markets they served more specifically are single-family residential (61,1%), agricultural (61.1%), and commercial (44.4%). Very few of these more specialized companies serve multifamily, industrial, or other market segments. Respondents didn’t specify which other market segments, but often companies – especially rural builders – have an additional trade specialty such as concrete work, landscaping, or site preparation, among others.

For respondents who say they are engaged in post-frame construction, those who work in post-frame but don’t identify it as their primary business, the numbers shift mildly. They are slightly less likely to be involved in single-family (57.8%) and commercial (39.4%), and far less likely to be involved in agricultural work (47.9%). This group is far more likely to work in multifamily with 36.6% of them saying they work in that segment compared to 22.2% of respondents whose primary business is post-frame construction. The same is true in industrial construction, where companies engaged in post-frame construction (25.4%) are more likely to do industrial work than those whose primary business is post-frame construction (16.7%). T1

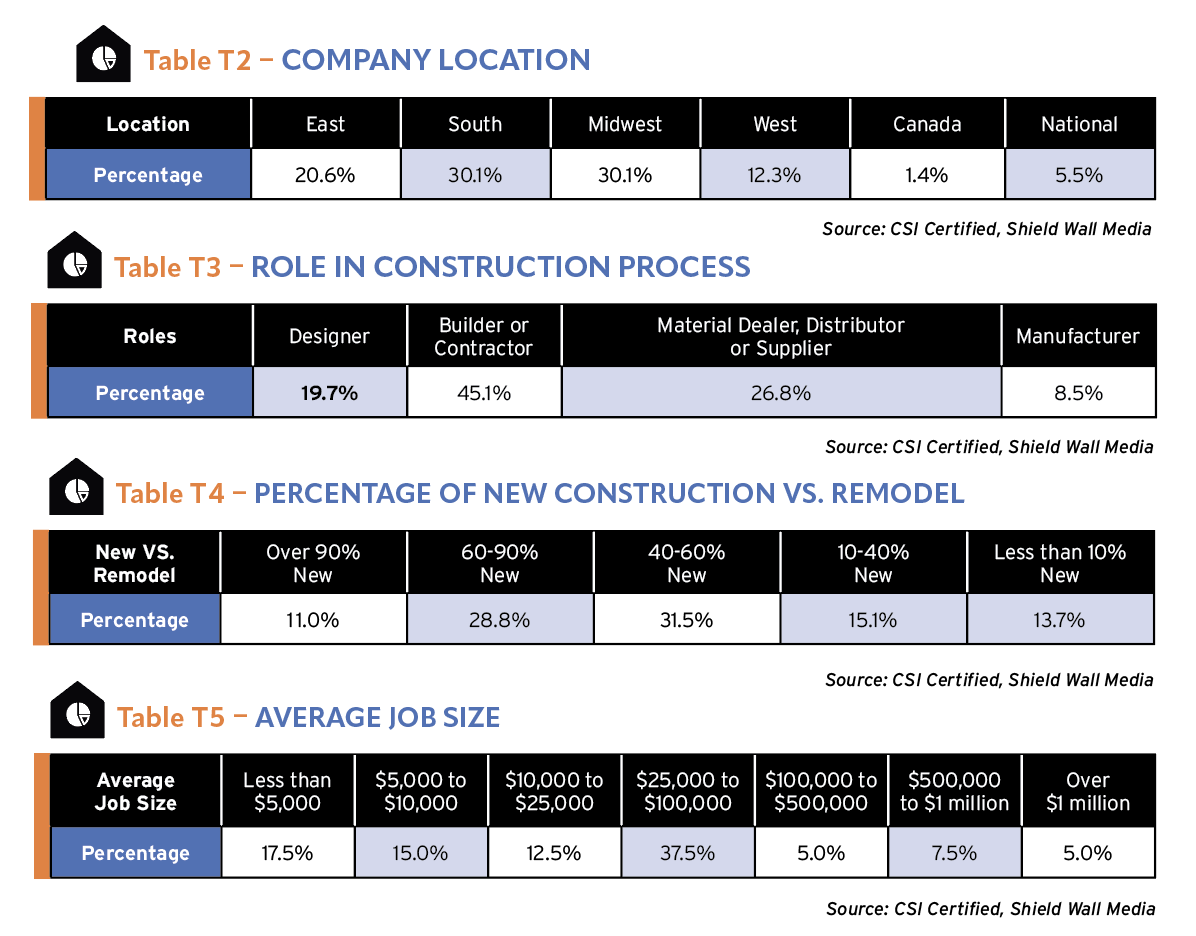

Companies engaged in post-frame construction tend to be grouped in the South and Midwest, according to the CSI data. Nearly two-thirds of post-frame companies are in those regions, split evenly with 30.1% in each region. The next largest representation comes from the East region with 20.6% identifying that as their location, while 12.3% claim the West region as their location. Only 1.4% were from Canada. There are about 5.5% of national companies who responded, and the largest proportion of them are manufacturers. T2

Most of the companies who responded to the survey and were engaged in post-frame construction were contractors (45.1%), but that was still less than half the total of survey takers. Distributors represent 26.8% of respondents while designers’ clock in at 19.7% of all respondents. The smallest faction represented were manufacturers with only 8.5% of respondents. T3

Of the work companies who are engaged in post-frame construction do, less than a third is remodeling. About 11% of those companies do more than 90% of their work in new construction. The predominant number, though, are either roughly half new and half remodel (31.5%) or between 60% and 90% new construction (28.8%). T4

The average job size for companies engaged in post-frame construction works out on a classic bell curve with 26% of them doing work between $25,000 and $100,000. At either end of the curve are the companies doing more than $1 million jobs (5.5%) and those doing less than $5,000 jobs 13.7%). The smallest jobs are likely repair work or materials supplied by a distributor or manufacturer. T5

When you look at the median point, companies averaging job size greater than $25,000 are 50.7% of the total companies. Half the companies have job sizes less than that. Since distributors and manufacturers are included in this mix, representing 35.3% of the total respondents, the job size will be much lower than the put-in-place construction cost of a project.

The rule of thumb for construction costs are that materials represent between 30% and 35% of the job, labor between 30% and 40%, totaling between 60% and 70% of a job cost. The rest is company overhead and profit. It is reasonable to calculate that the average job costs for put-in-place construction for companies engaged in post-frame construction are significantly higher because about a third of the respondents are only supplying material.

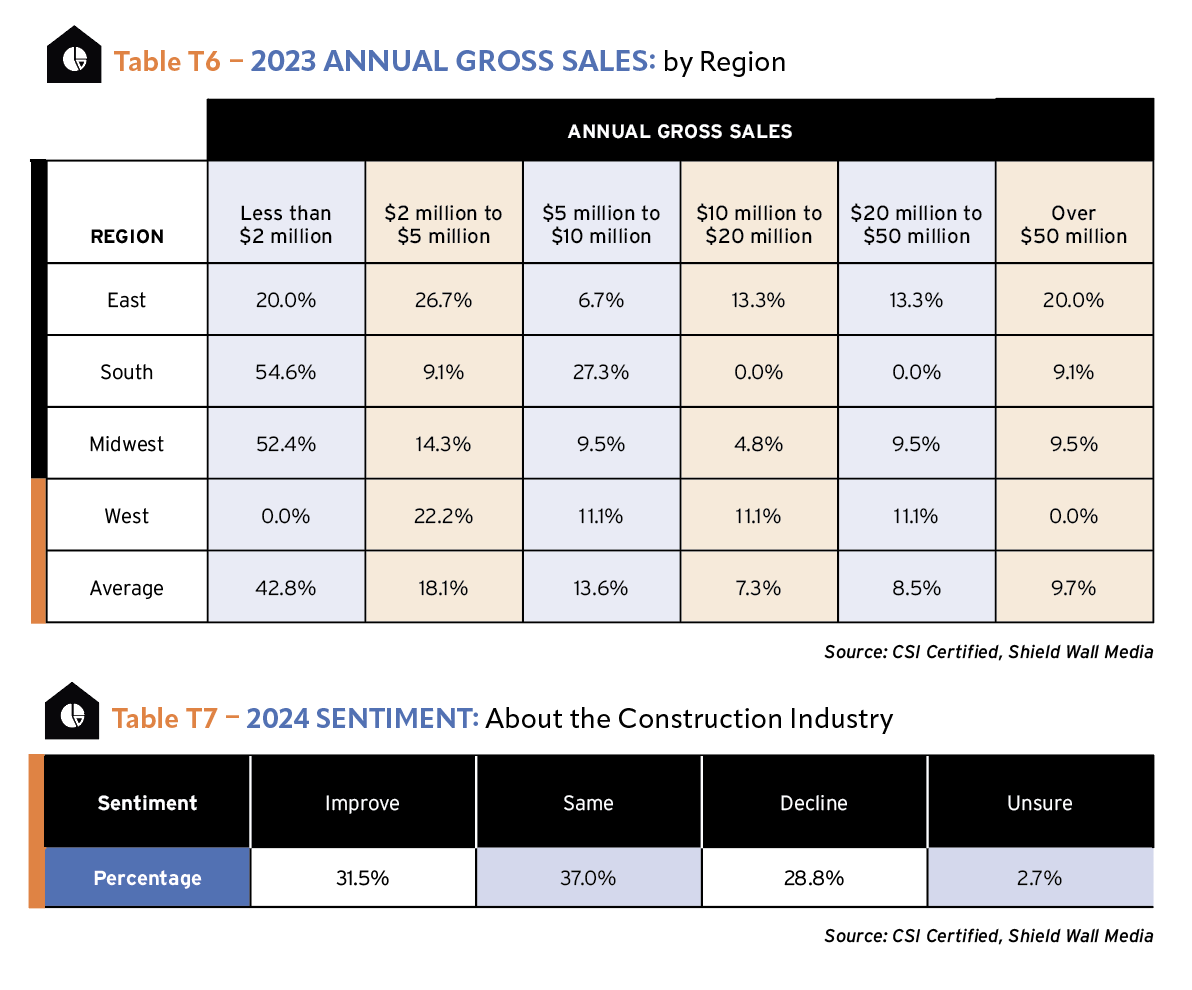

Data for the East region in this chart are a little volatile, so those results should be taken cautiously. When looking at regions where companies engaged in post-frame construction had revenues under $2 million, the East region is significantly lower than other regions. At the other end, for revenues over $50 million, it is significantly higher. That could be attributed to those companies being manufacturers as opposed to contractors or distributors, making the likelihood of their revenues higher. T6

But there are some conclusions we can draw from looking at the gross sales by region for companies engaged in post-frame construction. About half or slightly fewer of the companies had gross sales under $2 million.

Above that, distribution among the different sales ranges was relatively even with the averages for each range running between 7% and 18%. Companies in the South do report a much higher likelihood of having gross sales between $5 and $10 million (27.3%) than the others, and well above the range’s average of 13.6%.

Projected Industry Growth

Among companies engaged in post-frame construction, the outlook for 2024 is generally positive. 31.5% of our respondents report they expect the construction industry business climate to improve in 2024, and 37% tell us they expect it to remain the same. There are some doubters, of course, and during a presidential election year there is always concern about the state of the economy as a whole. More than a quarter of respondents anticipate a decline in the industry in 2024. T7

These respondents are a cross-section of the industry and a lot of variables can be attributed to this. Overall, Dodge Data and Analytics expects the commercial and industrial construction industries to increase about 7%, while the National Association of Home Builder anticipates an 4.7% increase in single-family starts, but a 19.7% decline multifamily starts. So, it depends on which market segment a company works in. And, as Carlson and Stover make clear in their comments at the top, it depends on what type of construction your company does.

The bottom line is that far more companies engaged in post-frame construction expect the 2024 industry to grow or remain constant than expect it to decline. At a ratio of approximately three to one.

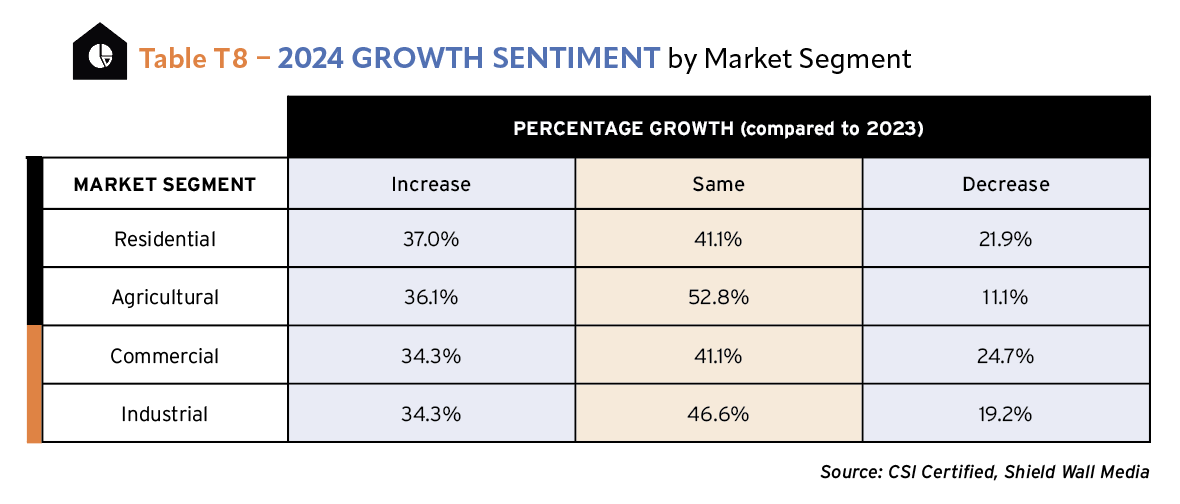

Expectations for growth in 2024 are generally optimistic across the different market segments. About a third of respondents, regardless of the segment they operate in, expected the construction market to increase in 2024. T8

Stover expects the post-frame niche to grow even better than the industry as a whole. “In our industry, growth continues due to barndominiums and increased awareness of post-frame construction versus stud frame, steel, and block construction materials,” he says. “Architects and engineers are starting to seriously look at our construction methods as a new way to build structures both residential and commercial, which is something we have always known. But now the market is realizing what we have and the advantages of Post-Frame.”

The agricultural market, in contrast to other sections of this report, is projected to be more robust in growth compared to single-family, multifamily, or residential. Only 11.1% of companies engaged in post-frame construction expect the agricultural market to decline in 2024.

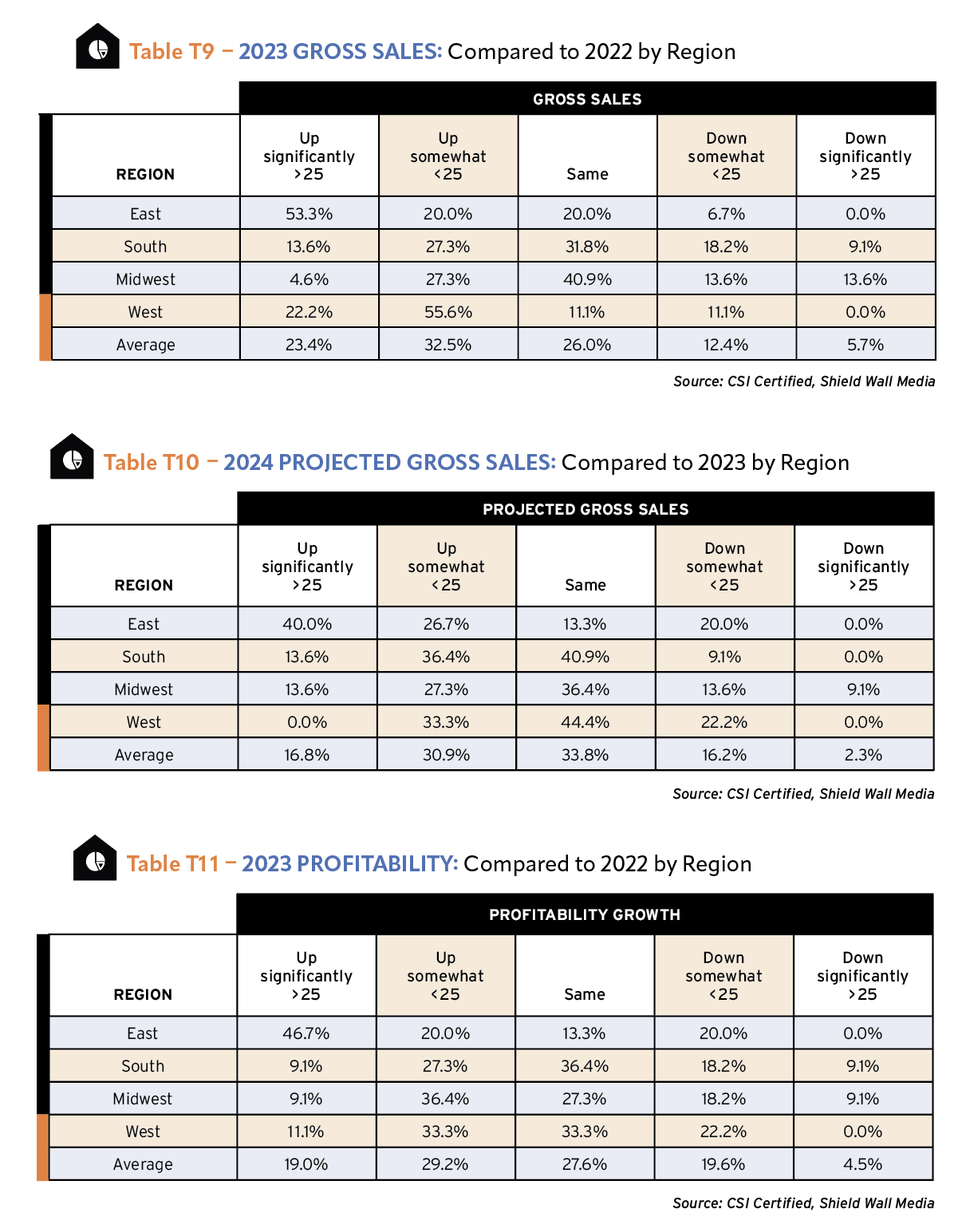

According to Dodge Data & Analytics, In 2023, the commercial construction market grew about 1% compared to 2022, and the residential market declined 8.6% compared to 2022. Among our respondents, we see a much better reaction to the marketplace among companies engaged in post-frame construction. Another caveat about companies from the East who again show significant differences to those from other regions and well off the averages for growth. More than half of those companies reported a greater than 25% increase in gross sales in 2023 compared to 2022. More than half of the companies in the West report gross sales increases of less than 25%.T9

Can this be attributed to a better reaction to the marketplace among companies engaged in post-frame construction. Carlson would agree. “Our customers in the post-frame marketplace were active and growing during that period,” he says. He offers a characteristic for his company, though, that may differentiate it from others, saying, “We were able to produce within reasonable lead times using our domestic sourcing.” Keeping customers happy is a great way to increase sales.

Companies based in the Midwest were less likely to report year-over-year growth in 2023 compared to other regions. Only 4.6% saw significant growth. 77.8% of companies in the West grew in 2023, and overall, 55.9% of companies reported increased sales in 2023.

Projections for growth among companies engaged in post-frame construction for 2024 were not as positive as the growth they experienced in 2023. Companies in the West especially had cooled on growth with only a third expecting this year to grow and none of those significantly. In fact, 22.2% project a decline. T10

The volatility of companies in the East who are engaged in post-frame construction continues with 40% saying they expect gross sales to rise significantly this year. Other regions are more tempered. Surprisingly no region other than the West expect to be down significantly in 2024.

Sales growth and profit growth do not necessarily go hand in hand. Companies may take on more overhead to support sales and see profitability decline until the sales meet the new capacities of the company. T11

Ignoring the companies that are engaged in post-frame construction who are based in the East for a moment, you can see from the chartthat companies in the other regions all experienced similar profitability changes in 2023. About 10% of them saw profits rise more than 25%, while a quarter to a third experience increases less than 25%. And between 18% and 20% were down slightly in profits in 2023 compared to 2022. Only the South and Midwest report significant profitability declines.

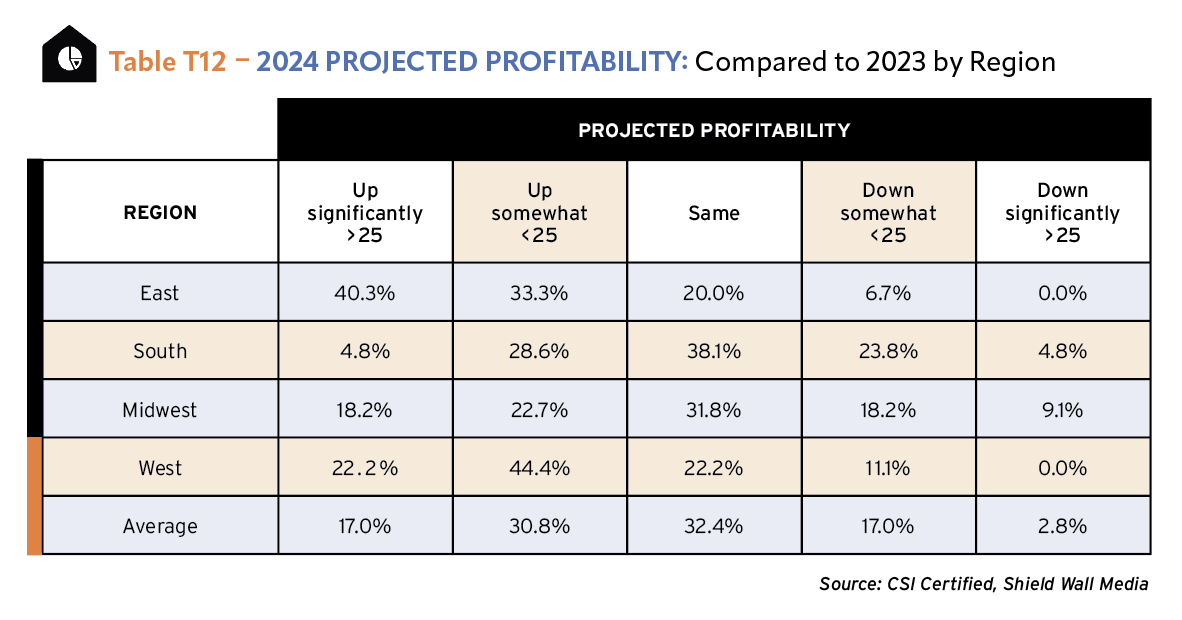

Companies reporting expectations for profitability in 2024 are closely matched to expectations for gross sales. When you compare projected profitability to projected gross sales by region, the averages from companies engaged in post-frame construction are nearly identical. 16.8% of companies across the regions expect to see sales growth in excess of 25%. 17% of companies expect profits to rise equally. There is no statistically significant difference between companies’ projections for growth of profitability in 2024 than those for gross sales when averaged across region. T10 & T12

There are, though, significant differences within a region. Of companies based in the West, 44.4% expect sales to stay the same, while a similar number expect profits to increase somewhat.

Company Size and Growth Projections

If you look at gross sales by companies engaged in post-frame construction broken out by market segment, you get a much more stable picture than if you look at them on a regional basis. Most companies only work in one region (unless they’re national) but they do work in multiple market segments, so the data is more reliable. T13

The obvious first conclusion is that in 2023 gross sales for companies engaged in post-frame construction in general, the multifamily sector was far above other sectors.This matches the overall report on multifamily from other sections, such as the rural builders. (See Section 3)More than 30% of these companies report increased sales of greater than 25% in 2023 compared to 2022. But that is outstripped by companies serving the industrial sector, a third of whom report such an increase.

When averaged across sectors, the largest reported change in gross sales was that companies were up less than 25%. On average, 30.7% of companies serving these sectors who are engaged in post-frame construction saw an increase.

About a third of companies serving the commercial market report sales were even year over year and the companies in the agricultural market who report a slight decline totaled 26.5%.

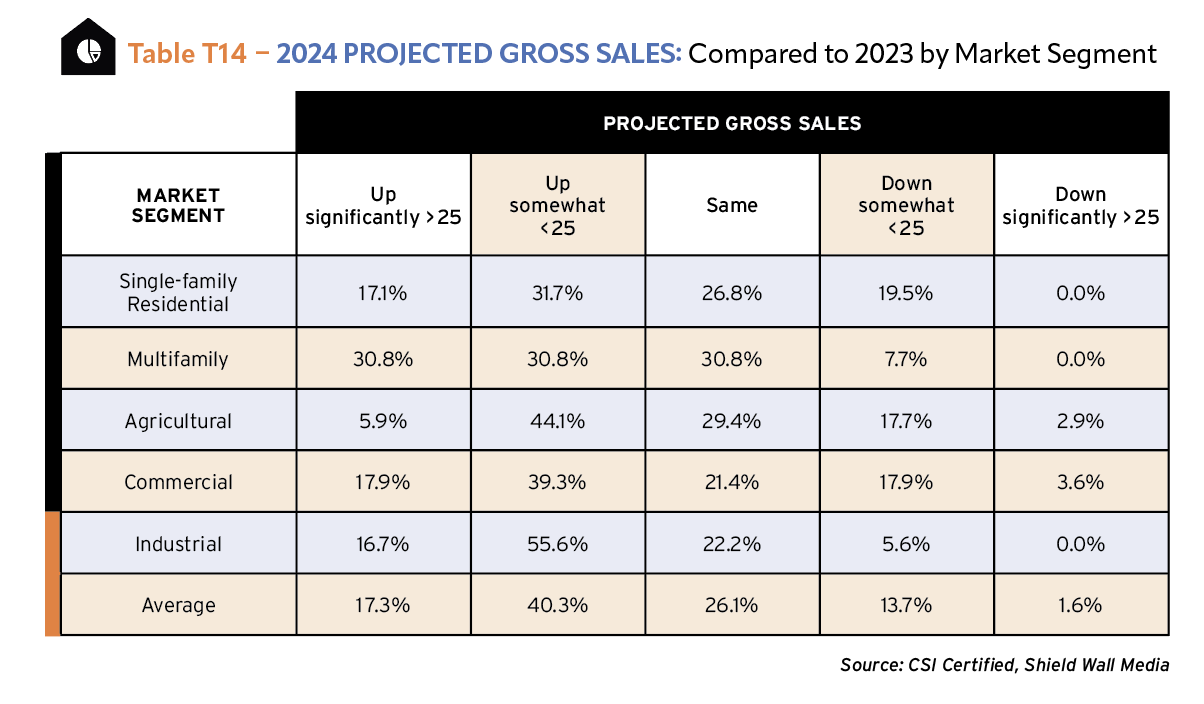

Looking to 2024, multifamily companies also projected another significant increase in gross sales with 30.8% expecting to see such a climb. That matches the percentage of multifamily companies who experienced a similar increase in 2023. T14

Only 5.9% of companies engaged in post-frame construction who serve the agricultural market project a steep increase in gross sales in 2024 even though 14.7% saw such an increase in 2023. Averaging the increases across market segments show that 17.3% of companiesexpect a sales jump of greater than 25% in 2024 while 23.2% say they saw a greater than 25% increase in 2023.T14 & T13

The big outlier for projecting an increase is the industrial market where 55.6% of companies engaged in post-frame construction expect to see some increase in 2024. The average of companies expecting a slight increase is 40.3%. Single-family (48.8%) and agricultural (50%) are not nearly as positive about seeing increases in gross sales – either slight or significant – in 2024 as the other market segment companies. T14

Very few companies expect a significant decline, with on average only 1.6% projecting decreases in excess of 25%. Year over year from 2023 to 2022, 8.5% of companies report a significant decline.

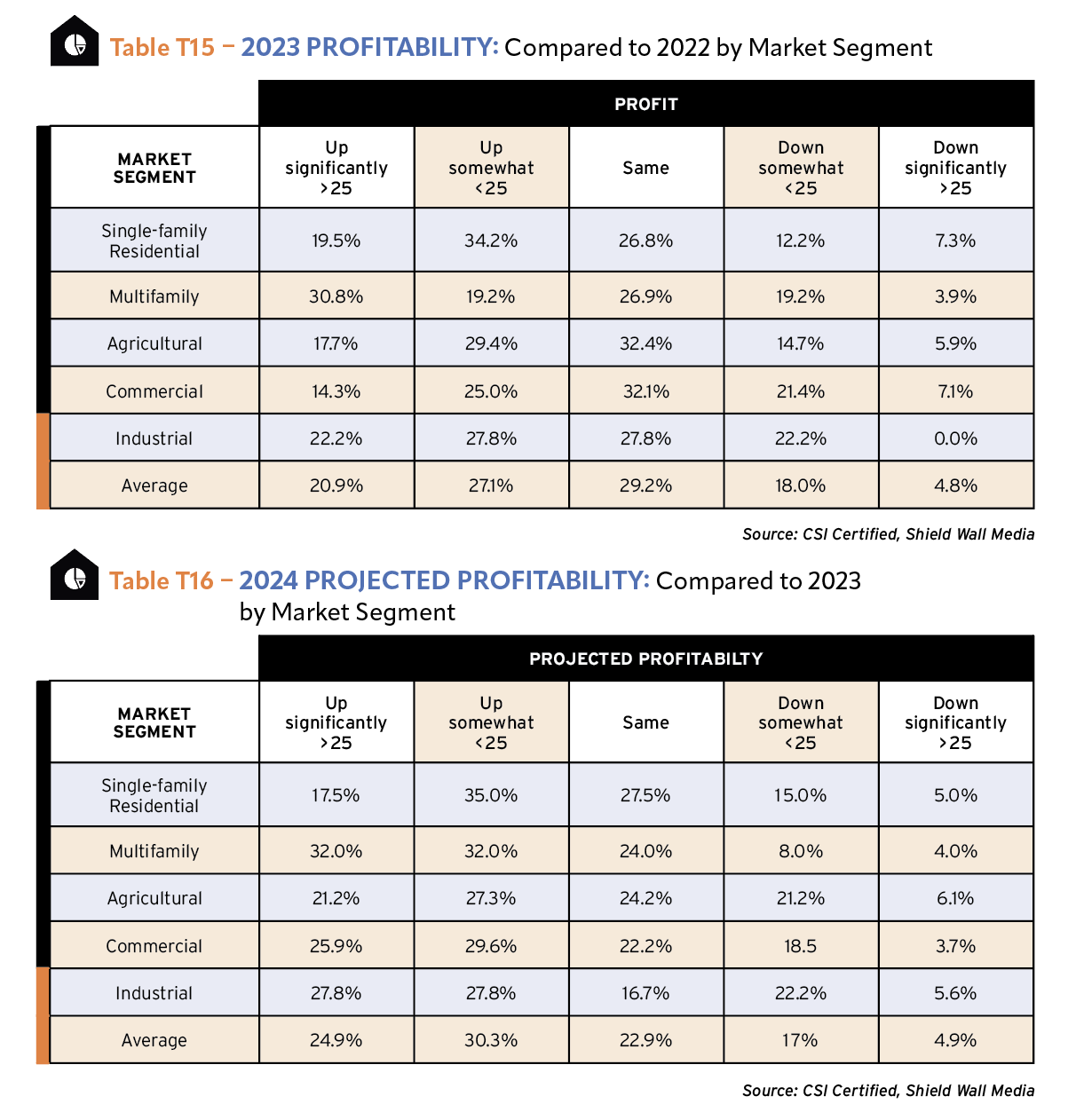

As was mentioned on the regional comparisons, profits and sales growth don’t automatically trend together. The residential sector, though, experienced strong profit growth in 2023 compared to 2022 among companies engaged in post-frame construction. Just over 53% of post-frame companies engaged in single-family market sector saw profits increase, and half of the multifamily companies saw increases. T15

Roughly 30% of all companies engaged in post-frame construction reported profitability staying the same in 2023 regardless of the market segments they served.

Having to deal with rapid inflation, rising material costs, and rising employee costs can outstrip a company’s ability to remain profitable, and those were the realities of 2023. Consequently, about 23% of all companies engaged in post-frame construction averaged across all market segments experience a decline in profitability.

For the most part, companies engaged in post-frame construction are more positive about 2024 profitability. On average, 55.2% of the companies across market segment expect to see an increase in profitability in 2024 with 24.9% of those projecting a significant increase of greater than 25%. In 2023, 48% on average showed increased profits over 2022. About the same percentage anticipate a decline in profitability in 2024 as experienced a decline in 2023. T16

Continuing the overall story of positivity, the companies engaged in post-frame construction working in the multifamily market segment are much more optimistic about their profitability prospects than the other market segments. 32% of them expect a significant increase in profitability in 2024. Only 12% expect any decline in profitability.

The other side of the residential coin, single-family construction, feels good about profitability in 2024, although not as fully as on the multifamily market. Only 20% of companies engaged in post-frame construction working in the single-family market segment anticipate a decline of profitability in 2024.

Future Opportunities and Challenges

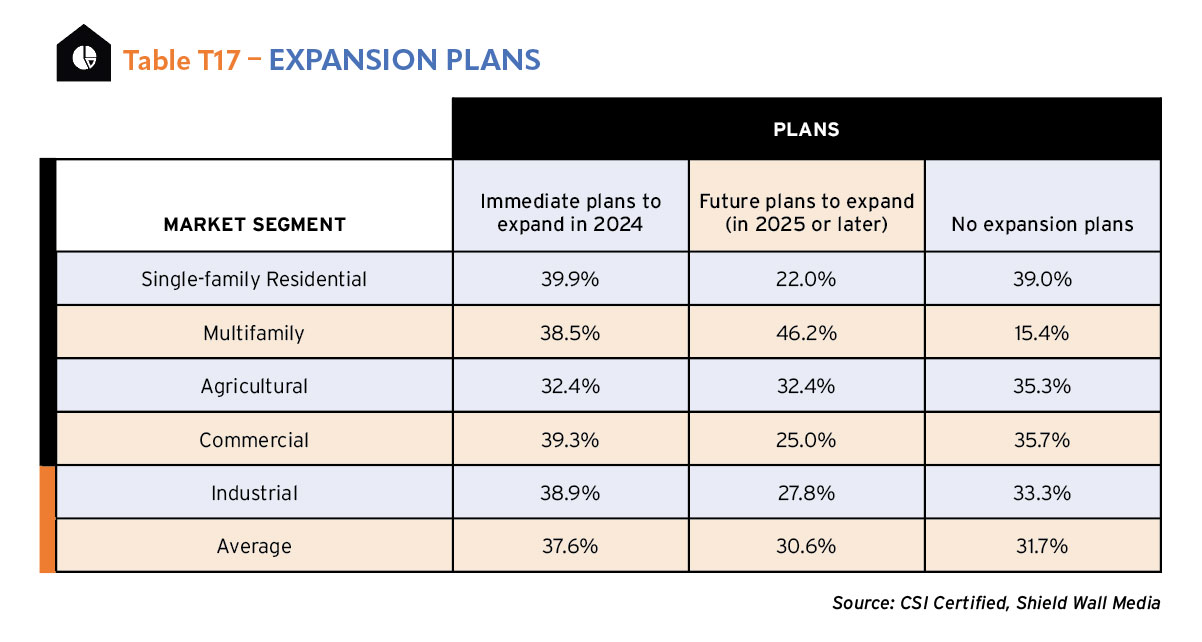

Across market segments, there is remarkable agreement about the immediate plans to expand in 2024 by companies engaged in post-frame construction. About 39% of each four segments have plans while the agricultural market segment is being more cautious with only 32.4% of companies saying they have immediate plans. T17

After that, different segments tend to break off into different attitudes. The multifamily segment says at a 46.2% rate that it plans to expand in the future with only 15.4% of those companies expressing no expansion plans.

Companies engaged in post-frame construction in the single-family market are least likely (39%) to say they have plans to expand while about a third of companies in the other segments – agricultural, commercial, and industrial – suggest they have no plans to expand.

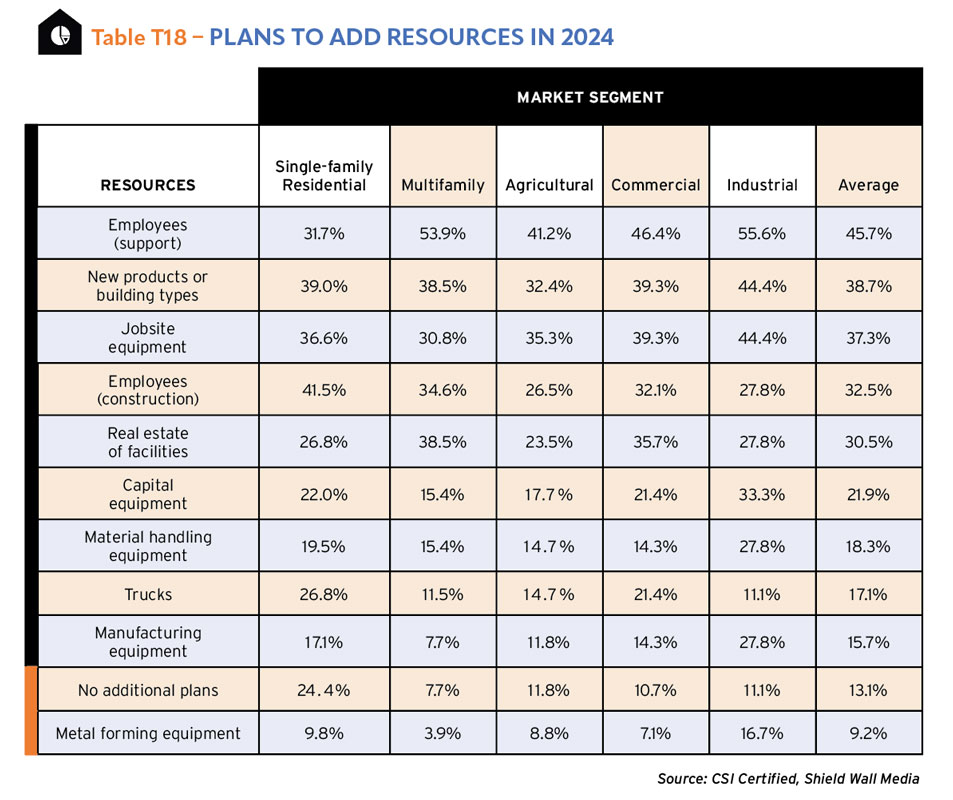

Companies engaged in post-frame construction who work in the commercial and industrial segments are far more likely to want to add support employees than companies in the other sectors. In fact, companies in the single-family sector point show support-employee hiring as the fourth most important thing to add.

In another change from industry wisdom, the shortage of skilled labor ranks fourth among the plans to add. That may be because companies are pessimistic about their ability to do it, or it could be slower growth makes this less important.

Many companies engaged in post-frame construction plan to add new products or building types to their mix in 2024, and are nearly as likely to add jobsite equipment, although for multifamily companies’ jobsite equipment is a lower priority than adding field employees or real estate or facilities. The same is true with commercial companies. T18

When ranking the needs for companies in the future, after the fifth ranked real estate or facilities plans, the average of the following resources are mostly propped up by the high interest in either the industrial segment or single-family segmentCompanies engaged in post-frame construction who serve the industrial market are far more likely to plan to add capital equipment, material handling equipment, manufacturing equipment, or metal forming equipment than companies in the other market segments.

Meanwhile, companies working in the single-family market segment are more likely than other segments to be planning to add trucks or have no addition plans.

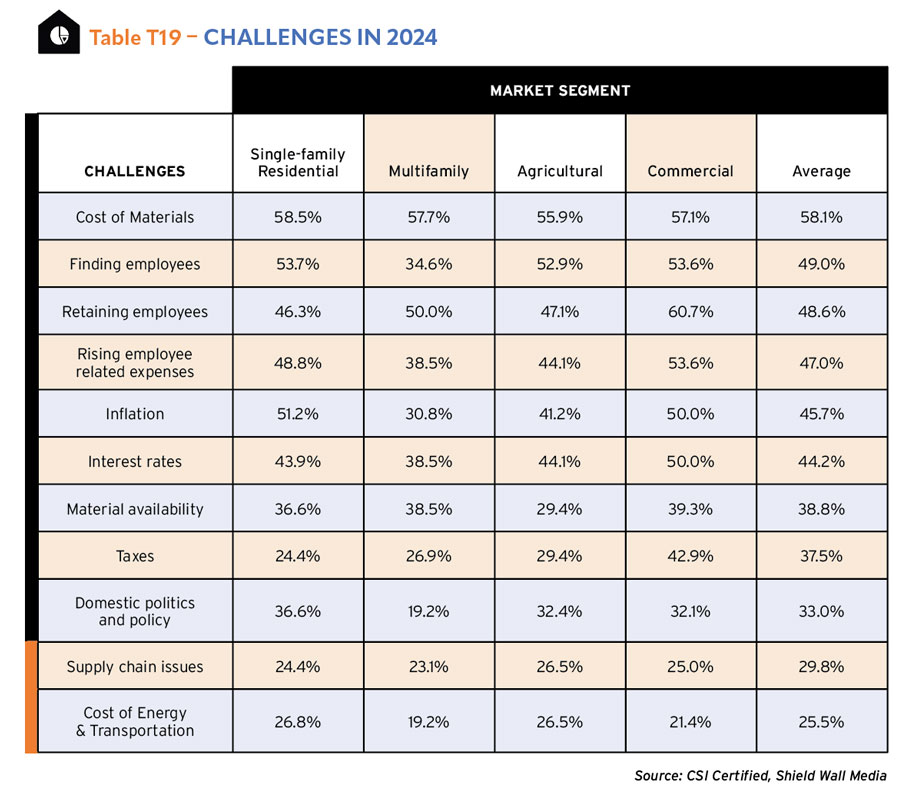

The construction industry is difficult in the best of times. For 30 years, it has tried to resolve the shortage of skilled labor, turning for the most part to immigrant help to meet demands. But recent economic tides have shifted those challenges and among companies engaged in post-frame construction the biggest challenge they face is the rising cost of materials. T19

With lengthening lead time due to regulatory reviews, the cost of materials can change significantly from when job estimates have been completed. As costs rise, building owners can get squirrely about their own plans, so managing those rising costs are an essential part of a company’s ability to get to job completion.

Todd Carlson, president, A.J. Manufacturing Inc., Bloomer, Wis., says, “The biggest challenges affecting our business are those outside of our control. They include regulatory standards such as trucking and logistical regulation, the assault on our fossil fuel and energy sources from one perspective and not understanding the implications of unplanned and too rapid pace of change.”

That sentiment is reflected in how respondents reacted to the list of challenges given in the survey. Cost of materials, interest rates, taxes, inflation, material availability, domestic politics, supply chain issues, and the cost of energy and transportation are all outside the control of most companies engaged in post-frame construction.

They are all on the list and rank highly. But the labor shortage continues in spite of the efforts of so many to address it. For Mark Stover, president, Perma-Column LLC, Ossian, Ind., “Labor continues to be the biggest challenge.”

Check out the whole Construction Survey Annual & Market Data 2024!