GENERAL ECONOMY TRENDS AND DATA

By Paul Deffenbaugh, Contributing Editor

Since Spring 2020, the world economy has been roiled by the pandemic, supply chain disruptions, inflation, and a host of other economic issues. Today’s economic environment is formed by those wild fluctuations, and the uncertainty we see today can be attributed in part to what has happened in the recent past. Only in the last few months has a more predictable pattern emerged.

Still, as Mark Twain famously said, “There are lies; there are damned lies; and there are statistics.” In today’s political environment, those statistics are being used to support a wide variety of conclusions, some at distinct odds with others. The University of Michigan Survey of Consumer Sentiment (see below) points this out more specifically.

How We Got Here

The following is a snapshot of what has happened in the overall U.S. Economy since the pandemic began in 2020. It gets us to the current economic environment with low unemployment, high inflation, high interest rates, and rising wages. Of those markers, none are close to historic levels. Unemployment has been lower, inflation has been higher, andwages have increased much more rapidly in the past than we’re experiencing now. And anyone who was around the construction industry in the early 1980s remembers that interest rates have been much higher.

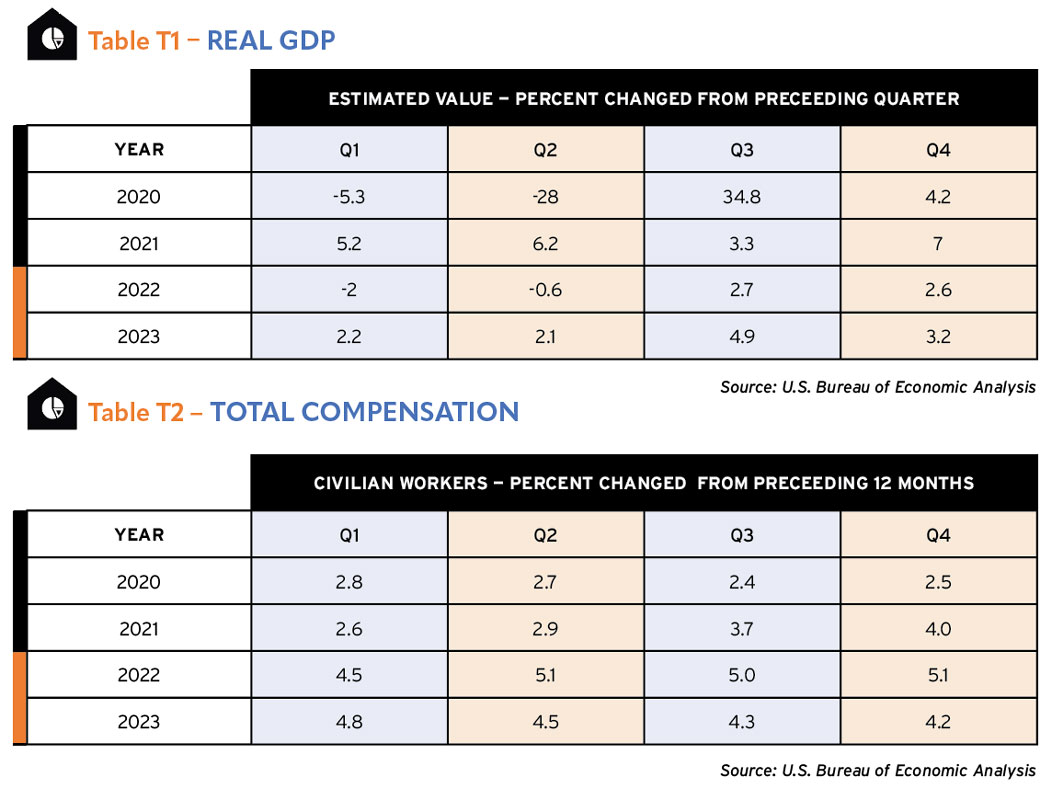

GDP

The U.S. passed through a tumultuous economic journey from 2020 to 2023, largely shaped by the COVID-19 pandemic’s impact. In 2020, the GDP took a sharp downturn due to widespread lockdowns and disruptions across industries, resulting in a contraction of approximately 3.5%.However, as the economy gradually reopened and stimulus measures were implemented, the nation saw a notable rebound in 2021, with annual GDP growth reaching around 5.7%. T1

In 2022, recovery momentum persisted, albeit at a slightly slower pace, with GDP expandingby approximately 4.2%.Various factors including increased consumer spending, infrastructure investments, and business expansions contributed to this growth. By 2023, the economy continued its upward trajectory, albeit with moderation, achieving a growth rate of around 3.8%. While challenges such as supply chain disruptions and inflationary pressures persisted, overall economic resilience and adaptive policies played pivotal roles in steering the U.S. economy towards gradual recovery throughout this period.

Wages

Total compensation for civilian workers since 2020 were influenced by various economic factors and policy changes. Amidst the onset of the COVID-19 pandemic, many workers faced uncertainty as businesses shuttered and unemployment rates soared. Consequently, compensation growth was modest or stagnant in some sectors as employers grappled with financial challenges. T2

However, as the economy gradually rebounded in 2021 and 2022, compensation trends showed signs of improvement. Labor markets tightened and competition for talent intensified. Employers began offering more competitive wages and benefits to attract and retain skilled workers. This trend was particularly notable in industries experiencing rapid growth or facing shortages in specific skill sets, such as construction.

Inflationary pressures during this period also influenced compensation dynamics, as workers sought higher wages to offset rising living costs. Employers responded by adjusting compensation packages to keep pace with inflation with varying degrees of success depending on industry and geographic location.

By 2023, total compensation for civilian workers had generally increased, but it was uneven across sectors and regions. Government policies, such as minimum wage adjustments and changes to labor regulations, also played a role in shaping compensation trends during this period. Overall, the trajectory of total compensation reflected the broader economic conditions and workforce dynamics experienced during these years.

Unemployment

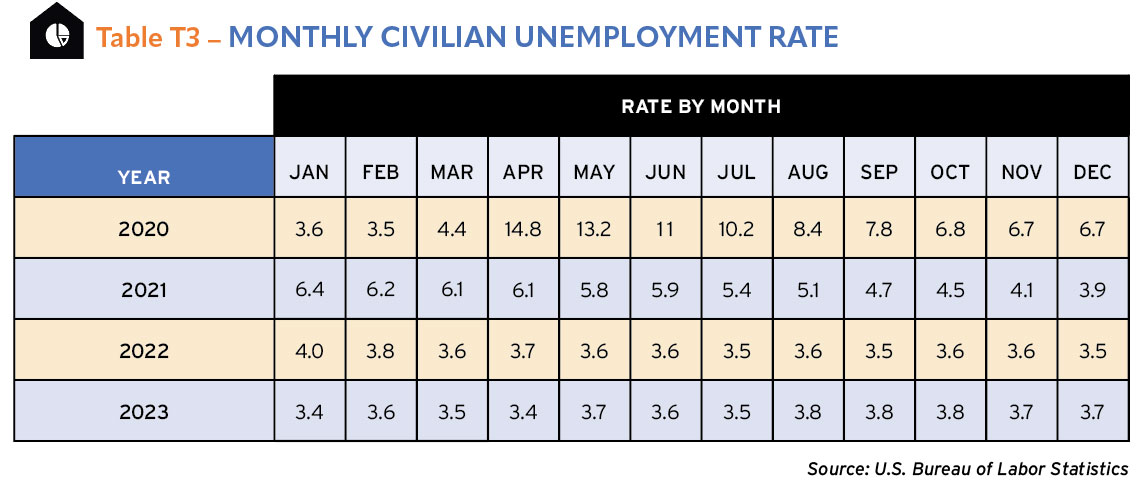

In early 2020, the unemployment rate skyrocketed to levels not seen since the Great Depression, peaking at around 14.8% in April 2020. Lockdowns and restrictions to curb the spread of the virus forced many businesses to shutter temporarily, leading to mass layoffs and furloughs across various sectors. T3

Throughout 2020 and into 2021, concerted efforts were made to mitigate the economic fallout of the pandemic. The implementation of stimulus measures such as the CARES Act provided financial relief to individuals and businesses, and vaccination efforts gradually allowed for the easing of restrictions. Consequently, the unemployment rate began to decline steadily from its peak, although at varying rates across different states and industries.

As 2021 progressed, the unemployment rate continued its downward trend, though the pace of improvement slowed compared to the initial stages of recovery. Structural shifts in the labor market, such as increased remote work and shifts in consumer behavior, also influenced employment dynamics during this period.

By 2022 and into 2023, the U.S. economy had largely rebounded from the depths of the pandemic-induced recession. The unemployment rate stabilized at pre-pandemic levels, hovering around 3-4%. While this represented a significant improvement from the peak of the crisis, challenges such as labor shortages in certain industries and disparities in employment opportunities persisted, highlighting the ongoing need for targeted policy interventions to foster inclusive economic growth and job creation.

Manufacturing

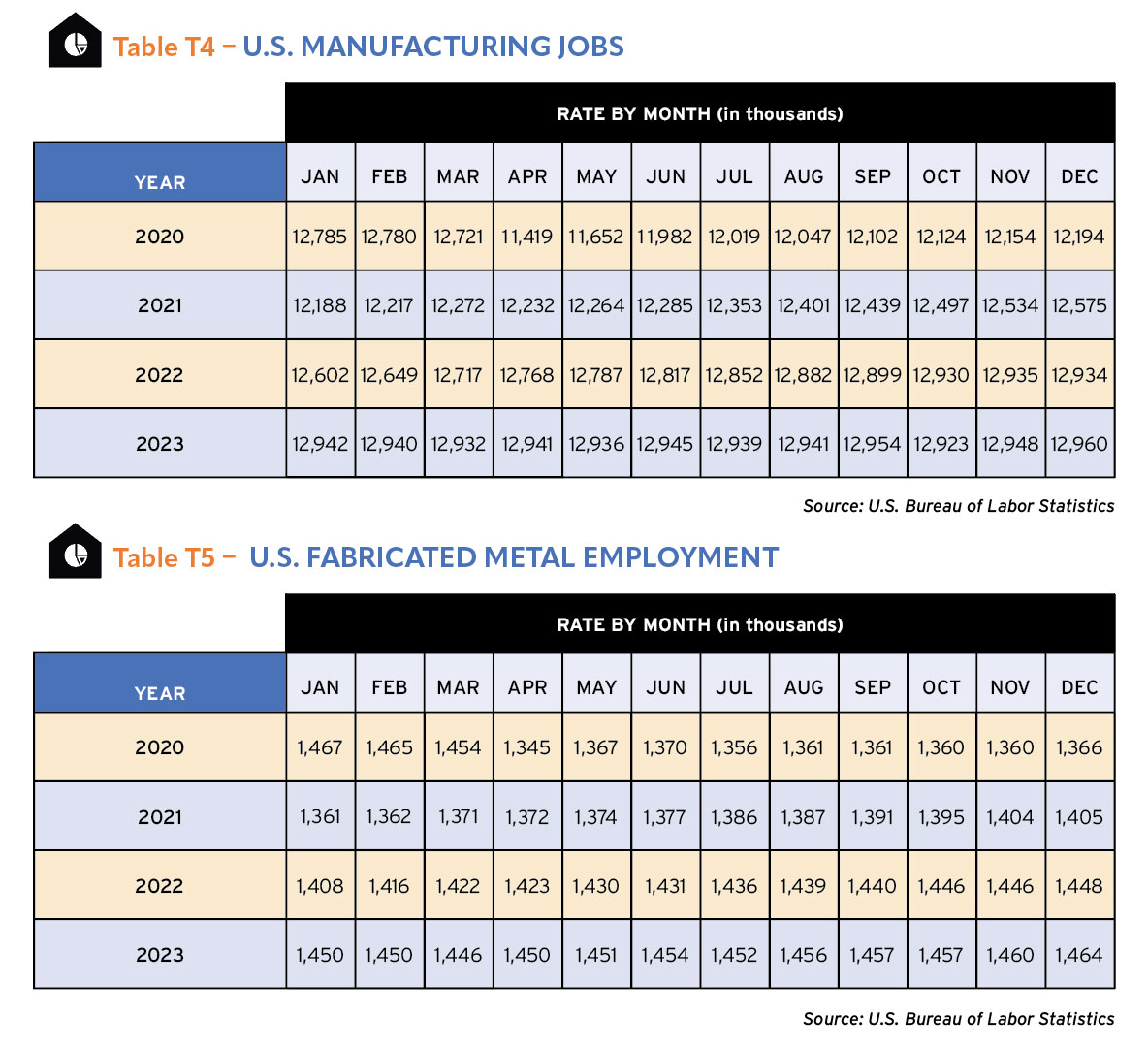

Employment in the manufacturing sector followed the same patterns as overall private employment was shaped by the repercussions of the COVID-19 pandemic, economic policies, technological advancements, and shifting consumer behaviors. T4

The pandemic-induced lockdowns led to widespread layoffs and furloughs across the manufacturing sector as factories halted operations to comply with containment measures. Uncertainty and decreased demand further exacerbated job losses, resulting in a significant downturn in manufacturing employment globally.

As economies gradually reopened and adapted to the new normal in 2021, manufacturing employment began to recover. Stimulus measures, government support programs, and increased consumer spending contributed to the rehiring of workers and the stabilization of employment levels in some regions.

By 2022, as vaccination campaigns progressed and supply chains adapted to disruptions, manufacturing employment saw a modest uptick. However, automation and digitalization trends also influenced the job landscape, leading to a restructuring of roles within the sector.

In 2023, while manufacturing employment showed signs of improvement, challenges such as skills gaps and labor shortages persisted. Efforts to reskill workers and invest in workforce development became increasingly crucial for sustaining employment growth amidst evolving industry dynamics.

Fabricated Metal

The COVID-19 pandemic disrupted the fabricated metal employment sector just as it did every other sector. But in 2021, increases in demand in construction, automotive, and infrastructure sectors boosted employment and the sector began to recover. Despite supply chain challenges and inflationary pressures, employment in fabricated metal industries in 2022 showed signs of stabilization. In 2023, as the economy continued to adapt to post-pandemic realities, fabricated metal employment remained relatively steady, reflecting resilience amidst ongoing uncertainties and evolving market dynamics. T5

Purchasing Managers Index

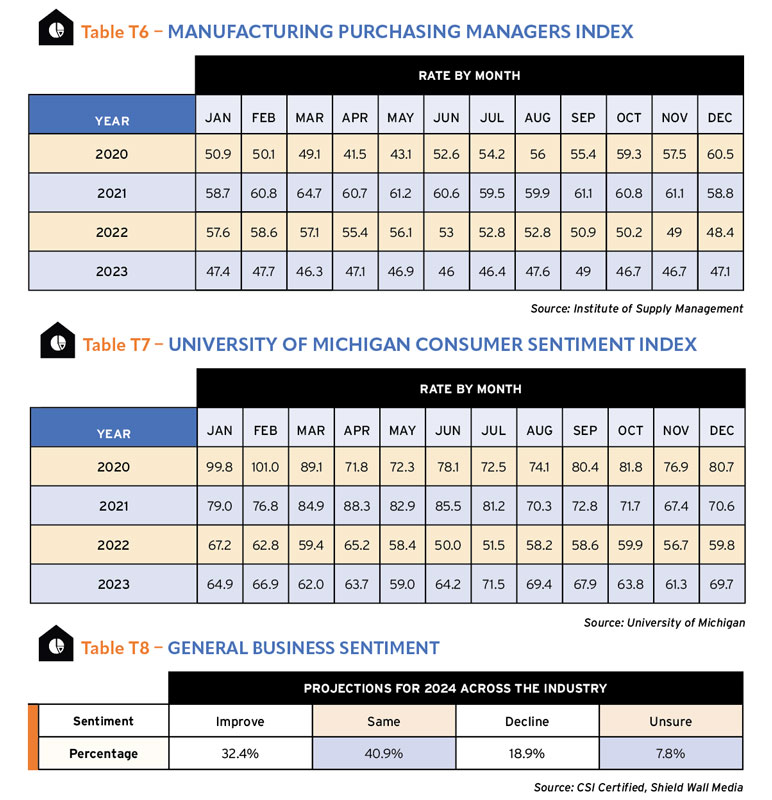

The manufacturing Purchasing Managers Index (PMI) is a key indicator reflecting the health of the manufacturing sector within an economy. The index is based on a survey of manufacturing supply executives conducted by the Institute of Supply Management. A PMI above 50 designates an overall expansion of the manufacturing economy whereas a PMI below 50 signifies a shrinking of the manufacturing economy. T6

In 2020, the PMI plummeted as the pandemic disrupted supply chains, halted production, and dampened demand worldwide. Many countries witnessed PMI readings well below the threshold of 50, indicating contraction.

As economies gradually reopened and adapted to new norms, the manufacturing PMI showed signs of recovery in 2021.Stimulus packages, vaccination campaigns, and pent-up demand spurred a resurgence in manufacturing output, leading to PMI readings moving back towards expansionary levels.

By 2022, despite ongoing challenges such as supply chain disruptions and inflationary pressures, the manufacturing sector exhibited resilience. PMI figures stabilized, reflecting improved business confidence and sustained growth momentum.

In 2023, while uncertainties persisted, particularly surrounding geopolitical tensions and environmental concerns, the manufacturing PMI dropped a little, then remained relatively steady, underlining the sector’s adaptability and stability amidst evolving global dynamics.

Consumer Sentiment

The fluctuations in the University of Michigan Consumer Sentiment Index – a widely recognized gauge of consumer confidence – from 2020 to 2023 reflect the tumultuous economic and social landscape during this period. T7

The index plummeted in 2020 but as the economy gradually recovered in 2021, the sentiment index began to rebound unevenly. Government stimulus measures and vaccine rollouts bolstered optimism, but persistent challenges such as inflationary pressures and supply chain disruptions tempered consumer confidence.

In 2022, the index stabilized as the economy adapted to the new reality. However, geopolitical tensions, such as the Russian invasion of Ukraine, and lingering economic vulnerabilities continued to influence consumer sentiment, leading to fluctuations throughout the year.

By 2023, the sentiment index reflected a cautiously optimistic outlook as the economy regained momentum and uncertainties eased. Since May 2022 when it was at its lowest point, the index has trended upward.

Construction Survey Insights Attitudes Toward the Future

In the Shield Wall Media survey of contractors, designers, manufacturers, and material suppliers and distributors, we found a generally positive attitude toward the general economy in 2024. Often during presidential election years, there is enough uncertainty and political strife that positive sentiment about the economy can be undermined. In this election year, the concern is even greater. T8

In February 2024, the University of Michigan’s Joanne Hsu, director of its Surveys of Consumers, and her research team reported on an investigation into how partisan differences post-COVID have led to huge gaps in attitudes toward the economy that outpaces the gaps in income, age, and education.

“This suggests that the way consumers interpret ongoing economic trends continues to be colored by partisan perspectives,” said Hsu. “The size of the partisan divide in expectations has completely dominated rational assessments of ongoing economic trends. This situation is likely to encourage poor decisions by consumers and policymakers alike. While there have always been partisan differences in preferred policies, the overwhelming size and persistence of the partisan gap has generated substantial economic uncertainty.”

That nearly three-quarters of the respondents to the CSI survey expected the general economy to improve or at least stay the same is indicative of the strong feelings within the construction industry about the health of the business environment. Only 18.9% of respondents thought the general economy would decline in 2024, but the 7.8% who indicated they were unsure about what might happen shows the uncertainty underlying attitudes toward the economy.

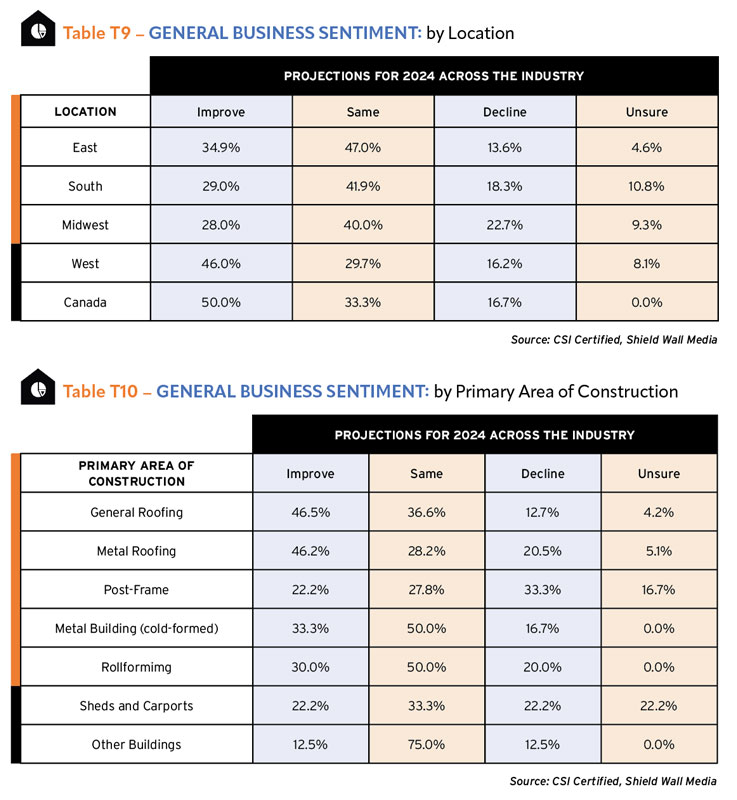

When that sentiment gets broken out by the location of the company, clear differences arise about sentiment. Companies in the West and Canada are much more positive about the general business environment with 46% of western companies and 50% of Canadian companies saying the economy will improve. T9

Respondents from the Midwest and South are the most pessimistic about the general business economy. Nearly a quarter of the Midwest (22.7%) expect the general economy to decline while 18.3% of survey-takers from the South hold that sentiment.

When you combine “Improve” with “Stay the Same,” companies based in the East are actually nearly as optimistic as those in any other region with a total of 81.9% of respondents agreeing with either of those sentiments. T10

Companies in the post frame business are far more pessimistic about the general business economy than those whose primary business is in other market segments. A third of them expect the economy to decline. Since most of those companies are based in the Midwest, that would partially explain why Midwestern sentiment is lower than other regions.

The most optimistic segments are companies whose primary business is general roofing or metal roofing. 46.5% of general roofers expect the economy to improve while 46.2% of metal roofers anticipate improvement. Only 12.7% of general roofers expect the general economy to decline.

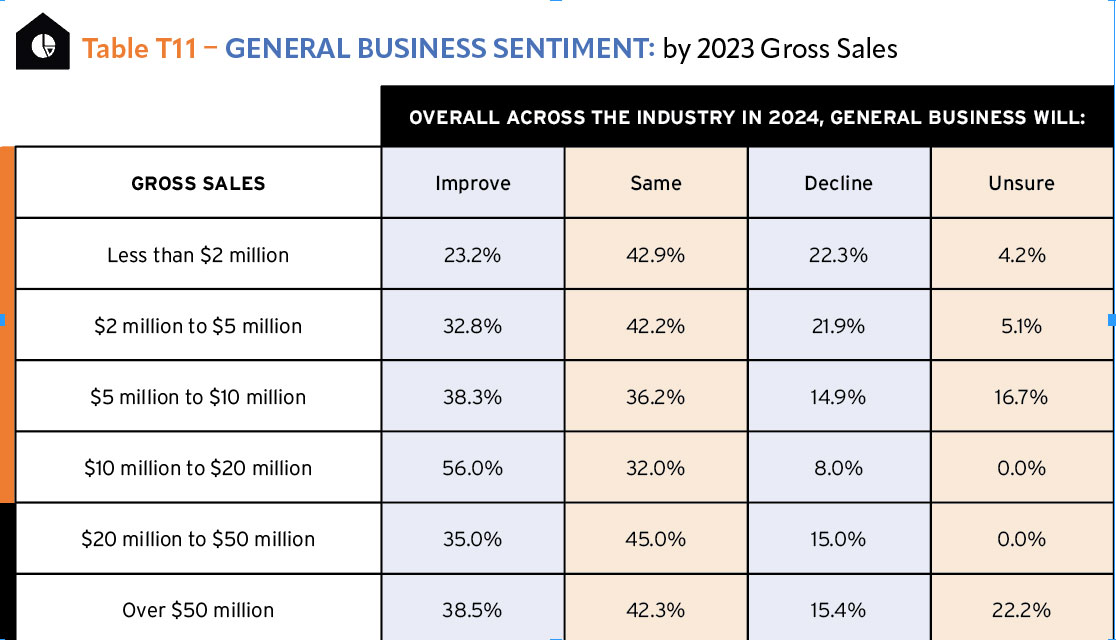

Company size also has an influence on attitudes toward the general economy. The smallest companies are much more inclined to be pessimistic. Of companies with annual revenues in 2023 of less than $2 million, 22.3% expect to see a decline in the economy in 2024. Of those between $2 and $5 million, 21.9% hold a pessimistic view about economic growth in this presidential year. T11

The $10 to $20 million per year companies are the most optimistic. 56% of them expect the economy to improve and another 32% (for a total of 88%) see it holding steady.

Survey Participant Profile

More than 300 industry professionals shared their vision and knowledge on the annual construction insights survey. Here are the demographics for the survey participants.

Location

The largest segment of respondents comes from the South (31.9%) followed by the Midwest (25.7%) and East (22.6%). The West makes up only 12.7% of survey takers. Strength in the South and Midwest is not surprising given the significant involvement of post-frame contractors, metal roofers, and agricultural-based construction in the survey.

Primary Area Construction

Companies that engaged in roofing, either metal or general, as their primary business represented more than 40% of the respondents. Metal roofers accounted for 13.1% and general roofers for 23.9%. The other roofers (4%) provided services such as gutter installation. Manufacturing companies represented 14.5% of survey takers. It is possible that some companies identifying metal roofing or metal building as their primary business are manufacturers, so there may be more manufacturers in the survey than that percentage suggests.” Respondents who selected “Other” primarily defined themselves as general contractors.

Participation in Other Areas of Construction

Companies in the construction industry seldom specialize in just one building type. General roofers also do metal roofing, for example. So we asked respondents to list other building types they did beside their primary building type. Again, the roofing categories had the highest response rate but this time, metal roofing (37.8%) surpassed general roofing (37.8%). And other categories that had low responses in the primary building type had much larger responses in this area. For this reason, when we looked into the performance of these companies, checking such things as gross sales or profitability, we identified companies who participated in these categories, not just those who listed them as their primary building type.

Primary Market Segment

Few of our respondents work in the industrial sector (7.2%) and most work in single-family residential (40.3%). When combined with multifamily (20%), the residential sector provided the largest complement of survey takers.

Other Market Segments

As with the primary building type and other building types, we wanted to identify companies who worked within market segments, not just those who specialized in them. It’s common for multifamily companies also to do commercial work or single-family residential work. The residential market produced the largest number of survey takers. More than 50% of respondents say they work in single-family residential. When combined with the 36% who do multifamily, the residential market segment has a participation rate of more than 86%.

2023 Gross Sales

Nearly 40% of respondents had gross annual sales of less than $2 million in 2023. A few (8.8%) report sales over $50 million. There are manufacturers who participated in the survey and it’s likely they represent a significant number of those along with material suppliers. Contractors and designers seldom have firms that large.

Percentage of New Construction vs. Remodel

There is a tendency in the construction industry to think companies engage in either new construction or remodeling. The two segments present significantly different challenges and have different motivators and economics. However, in our survey of this niche, we found the largest segment of respondents (31.5%) did work between 40% and 60% new construction. At either end of the spectrum, those doing almost all or all new construction represented just 11.9% of the respondents, while those doing almost all or all remodeling work ticked in at 19%.

Roles in Construction

About half of the respondents to the survey identified as builders or contractors. Nearly 20% were designers and the remaining 30% were split roughly evenly between manufacturers (15.1%) and material dealers, distributors or suppliers (16.4%).

Purchasing Design Involvement

The final profile we asked of survey respondents was their involvement in the purchasing decisions. For smaller firms of less than $2 million this is almost always the owner, but for larger firms there is often a purchasing manager. About two-thirds of the respondents were either the sole decision maker (36.3%) or were involved in purchasing decisions (32.5%). Only about 15.3% of respondents report no involvement in product purchasing. Given the low involvement of designers in purchasing decisions (they specify but don’t purchase) this number is not surprising.

Check out the whole Construction Survey Annual & Market Data 2024!