ROLLFORMING AND METAL FORMING CONSTRUCTION DATA

By Paul Deffenbaugh, Contributing Editor

Rollforming or metal forming are essential parts of any construction project that involves the use of metal components. Whether it’s done at the manufacturer plant, distributor facility, or on the job by the contractor, today’s machinery is much more sophisticated than those used just a few years ago. Computer technology and improved designs have made them easier to use and capable of delivering metal materials that are a far cry from the simple crimp of old. There are difficulties the industry faces, though, and Jim Bush, vice president of sales and marketing for ATAS International, Allentown, Pa., cites the competition from other building products in talking about the sustainability of their products. “Competitive building materials are pushing sustainable attributes of their products in a much better way than those of us in the metal arena,” he says. “As an industry we must do a better job communicating a universal message on the green and beneficial environmental aspects of metal building products.”

A lot has changed in the industry and much of that is in the details.

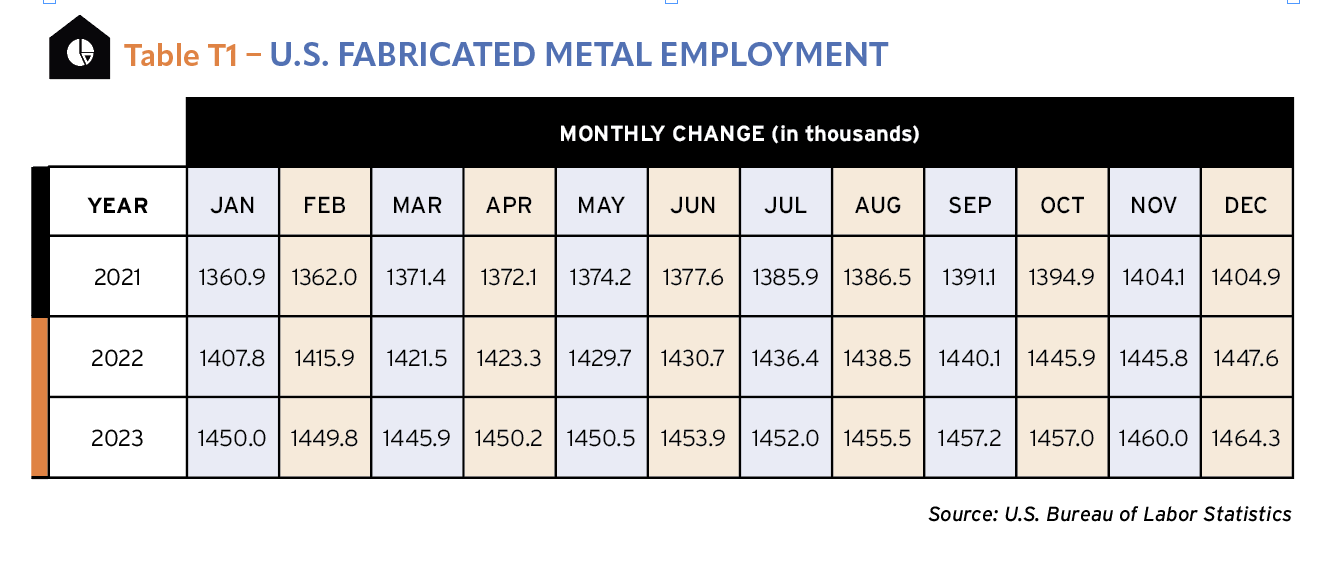

We should begin, though, with a reminder of the larger picture. Metal fabrication is a growing market. According to the U.S. Bureau of Labor Statistics, employment in the metal fabricating sector has increased from 1.36 million jobs in Jan. 2021 to 1.46 million in Dec. 2023, which is almost a 7% increase. Much of that growth will be in the automobile industry but the construction industry is growing as metal building materials begin to increase in market share. In residential roofing, for example, metal roofing now has 18% of the retrofit market as of 2022, according to the Metal Roofing Alliance. T1

Characteristics of the Rollforming and Metal Forming Industry

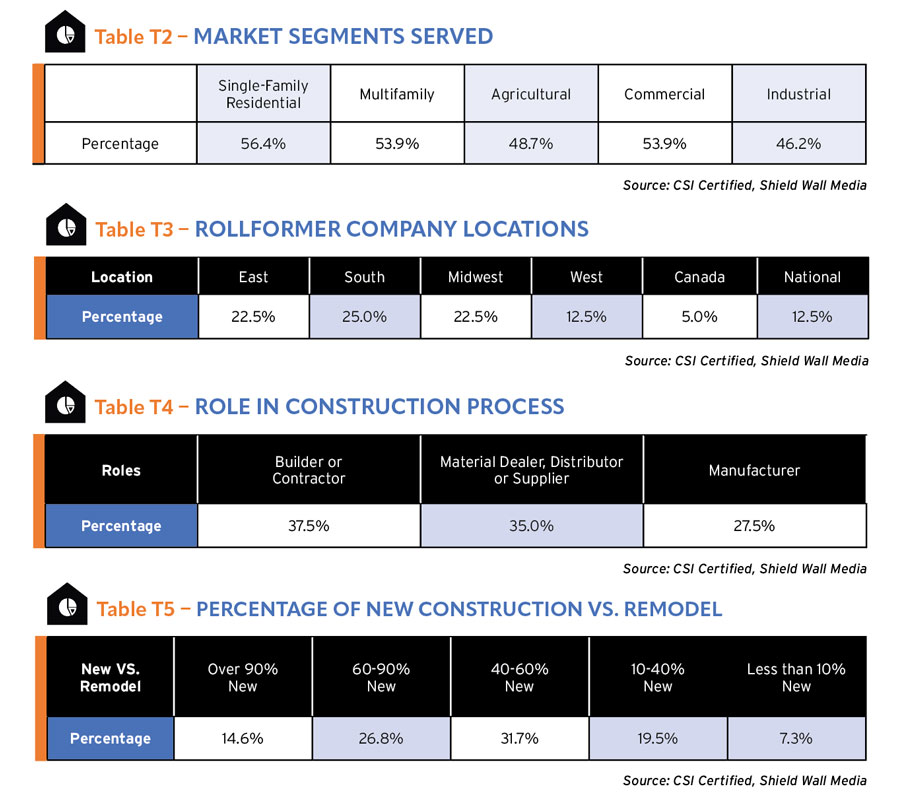

Filed under the category of not much of a surprise, companies engaged in rollforming serve all the construction segments about equally. They are slightly more likely to be involved in single-family residential (56.4%) and slightly less likely to be involved in industrial (46.2%). The total spread among the five market segments is less than 10 percentage points. T2

In the CSI data, we found most of our respondents came from the East (22.5%), South (25%), and Midwest (22.5%). There were a few Canadian survey takers, and 12.5% of respondents identified as national or in multiple regions. Those latter companies could be manufacturers or distributors with locations in more than one region. T3

The percentage of companies identifying as being in multiple regions may be explained by the large percentage of respondents who reported they were manufacturers (27.5%). Among companies engaged in rollforming, 37.5% of them are builders or contractors and 35% were material dealers, distributors or suppliers. That data generally matches our assumptions about who is using rollforming or metal forming equipment in the construction industry. T4

Given the larger market share metal roofing now has in the residential retrofit market, you would expect a large percentage of companies to be doing remodeling work. But a significant amount of the retrofit market is metal shingles, so only manufacturers would be involved in that portion. Still, only about 26.8% of survey takers say a majority of their work is in remodeling. 41.4% percent say more than 60% of their work is new construction, and the remainder (31.7%) report they are about half and half new construction and remodeling. T5

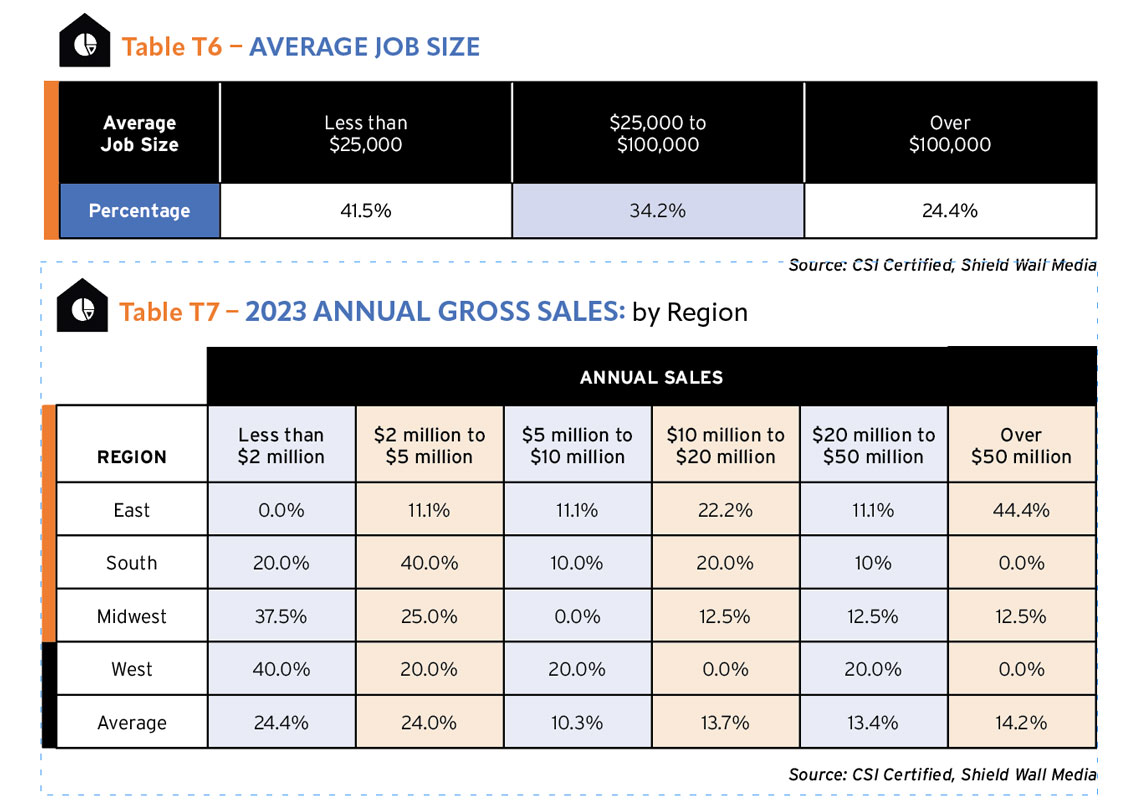

The average job size for companies engaged in the rollforming and metal forming market tends to run less than $100,000. Only 24.4% say they have an average job size greater than $100,000 and 41.5% report their job size is less than $25,000. T6

As has been mentioned elsewhere in this report, building materials represent on average about 30% to 35% of a job cost, so companies that use rollforming and metal forming machinery to make materials and do not install them, will have a lower job cost than contractors or distributors who install them.

On average, about half of the respondents who are engaged with rollforming say their annual gross sales in 2023 were less than $5 million. And half of those, or 24.4% of the total, had sales less than $2 million. T7

A surprising number of companies reported sales greater than $50 million, and the majority (44.4%) were based in the East. As has been reported in other sections, this region’s data has been volatile, and that high number may be swayed by a few respondents.

In the Midwest (37.5%) and the West (40%), the largest cohort of respondents reported annual sales of less $2 million. In the South, survey takers say they had the greatest likelihood of having annual gross sales between $2 and $5 million (40%).

Projected Industry Growth

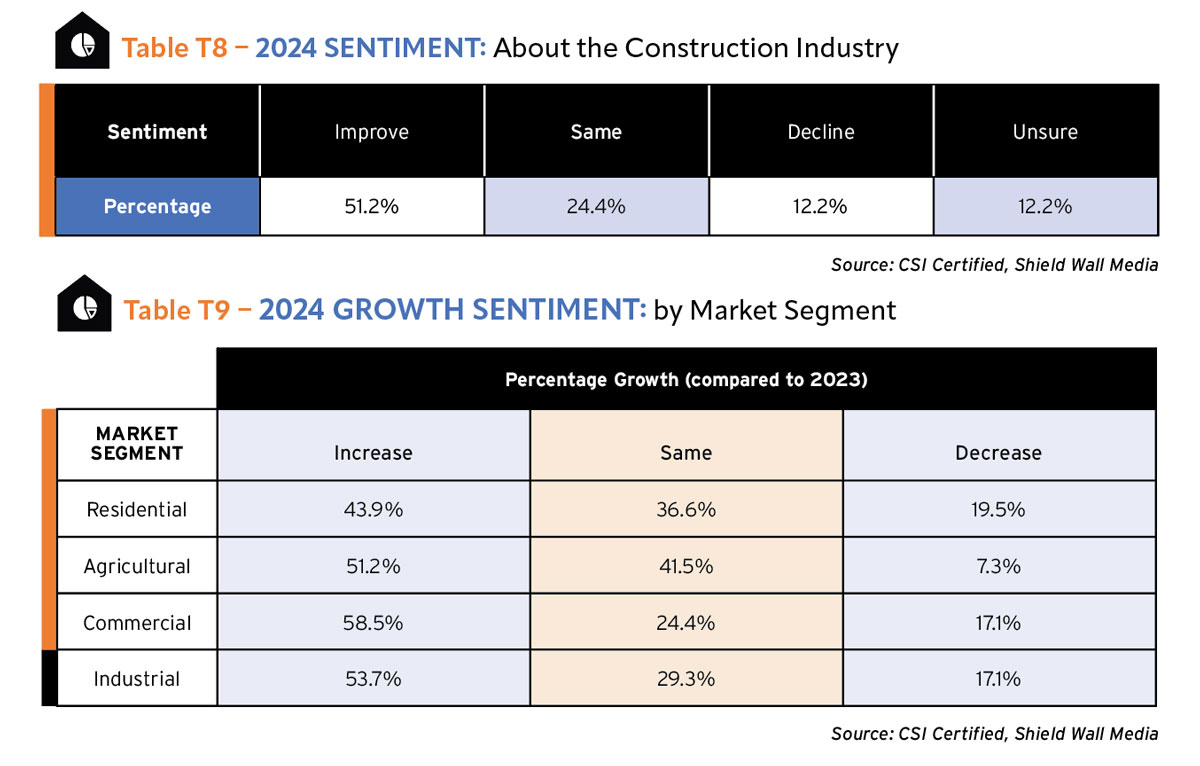

More than half (51.2%) of companies engaged in rollforming expect the construction economy to improve in 2024 compared to 2023. There were 12.2% of survey takers who expected it to decline with another 24.4% predicting it would stay the same, and another 12.2% who aren’t sure what to think.T8

Since rollforming is substantially spread across both residential and commercial construction, new and existing buildings, this data isn’t surprising. While the single-family market is expected to be up 4.7% in 2024 according to the National Association of Home Builders (NAHB), starts in the multifamily sector are expected to drop nearly 20%. And according to Carlos Martin, project director of the Remodeling Futures Program at the Joint Center for Housing Activities, “Home remodeling will continue to suffer this year from a perfect storm of high prices, elevated interest rates, and weak home sales. These headwinds create considerable uncertainty in the economy, and remodeling spending is projected to fall from $481 billion last year to $450 billion in 2024.” That’s a 6.5% decrease in activity.

Even the 7% increase on the commercial side, as forecast by Dodge Data and Analytics, may not be enough to calm nerves among companies engaged in rollforming activity.

When we break out by market segment the projected growth among our survey takers, the uncertainty market by market becomes even more evident. The rise in single-family and decline of multifamily explain the predictions about the residential market with 43.9% of respondents saying the residential segment will grow in 2024 and 19.5% predicting a decline. T9

The commercial segment has a more positive feeling among companies engaged in rollforming activity. Better than half (58.5%) project an increase in this market segment, but a still significant percentage (17.1%) anticipate a decline.

In other sections of this report, we have often talked about the relative pessimism among respondents about the agricultural segment. Among companies engaged in rollforming activity, that is flipped on its head. The rollforming respondents are least likely (7.3%) to project a decline in this market compared to the other segments.

Company Size and Growth Projections

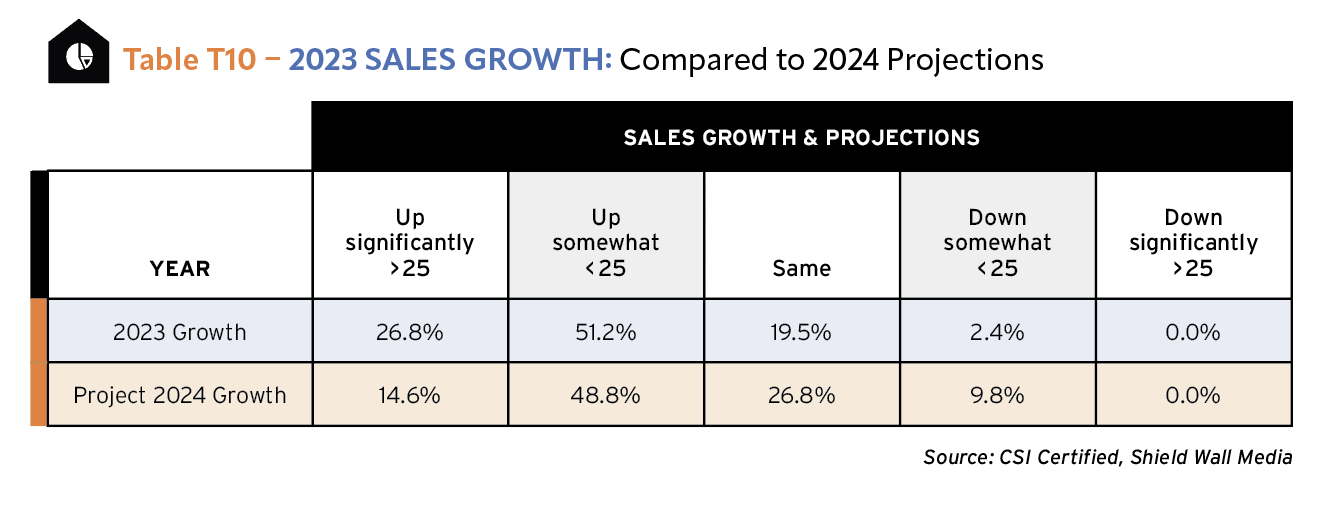

We wanted to use the information gained in the CSI data about companies engaged in rollforming activity to compare sales and profitability by market segments served as well as by the roles played in the construction process. However, the response rate fell below a level we felt comfortable about drawing those kinds of comparative conclusions. T10

We can look at a broader view of companies engaged in rollforming activity, though, and how their growth in 2023 compared to their projections for 2024. On the sales growth side of the ledger, 2023 for these companies was generally a strong year. Nearly 80% of the respondents reported their 2023 gross sales were up over 2022, with a strong 26.8% saying they were up significantly. Only 2.4% reported a decline and none of those said sales were down greater than 25%.

The optimism borne of 2023’s success isn’t carrying through to projections about 2024. Only 63.4% of respondents expected their gross sales to increase and about a quarter as many (14.6%) expected them to increase more than 25%. In 2023, 26.8% of survey takers say gross sales increased more than 25%. Larger percentages of respondents project a flat sales picture (26.8%) and 9.8% anticipate a decline in gross sales.

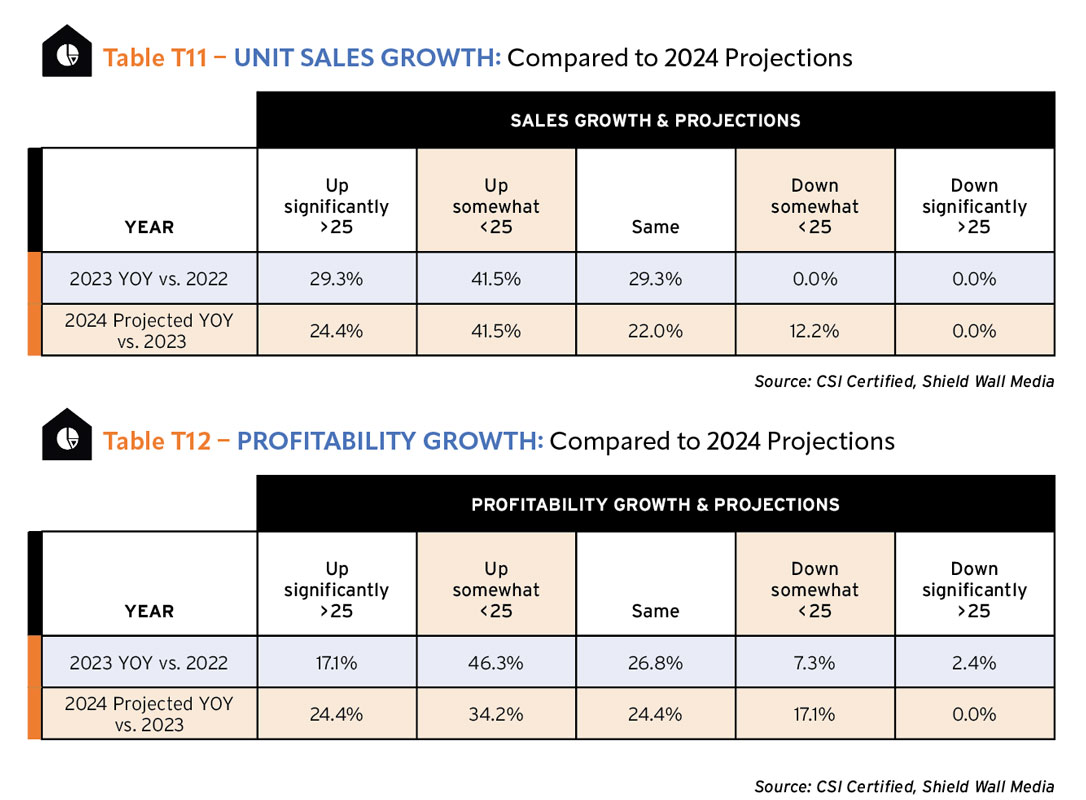

When looking at unit sales, though, the picture is different. Companies engaged in rollforming activity on the whole expect to increase their unit sales in 2024 at about the same rate as they experienced in 2023. More than 70% reported increases in 2023, and 65.9% project an increase in unit sales in 2024, with the decline coming entirely from companies who experienced significant increases in 2023. T11

Companies engaged in rollforming activity are also less optimistic about 2024 than they reported in 2023. The percentage saying activity will stay the same is down to 22% compared to the 29.3% who reported flat activity in 2023 compared to 2022. 12.2% anticipate a decline this year, where none had reported a decline in 2023.

If gross sales don’t increase at the same rate as unit sales, then profitability will suffer because costs of production increase. Sell 10% more units but only see sales go up 5%, it’s clear that profits are leaking somewhere on the cost side. Among companies engaged in rollforming activity, respondents reported increases in both gross sales and unit sales in 2023 compared to 2022, and only a small fraction (2.4%) experienced a decline in gross sales, while none had a decline in unit sales. However, nearly 10% of survey takers reported a decline in profitability. For some companies, cost increases were outstripping sales growth, and it shows in these numbers. It also shows later when they answer questions about challenges faced, and the biggest issues are related to controlling costs. T12

A.J. Manufacturing Inc., Bloomer, Wis., makes windows and doors for the post-frame building industry, but president Todd Carlson addresses the difficulties of unit sales. “Top line growth is unavoidable these days with inflation of all costs of doing business and the increased prices required to maintain strong performance,” he says. “Growing in the context of unit volumes and bottom-line performance is the key.”

Projecting to 2024, an even larger number of companies anticipate a decline in profitability with 17.1% saying it will be less than 25% year over year. None report a significant decline. Interestingly, 24.4% expect to see a significant increase in profitability, indicating that some companies are adjusting pricing to meet the new cost challenges.

Future Opportunities and Challenges

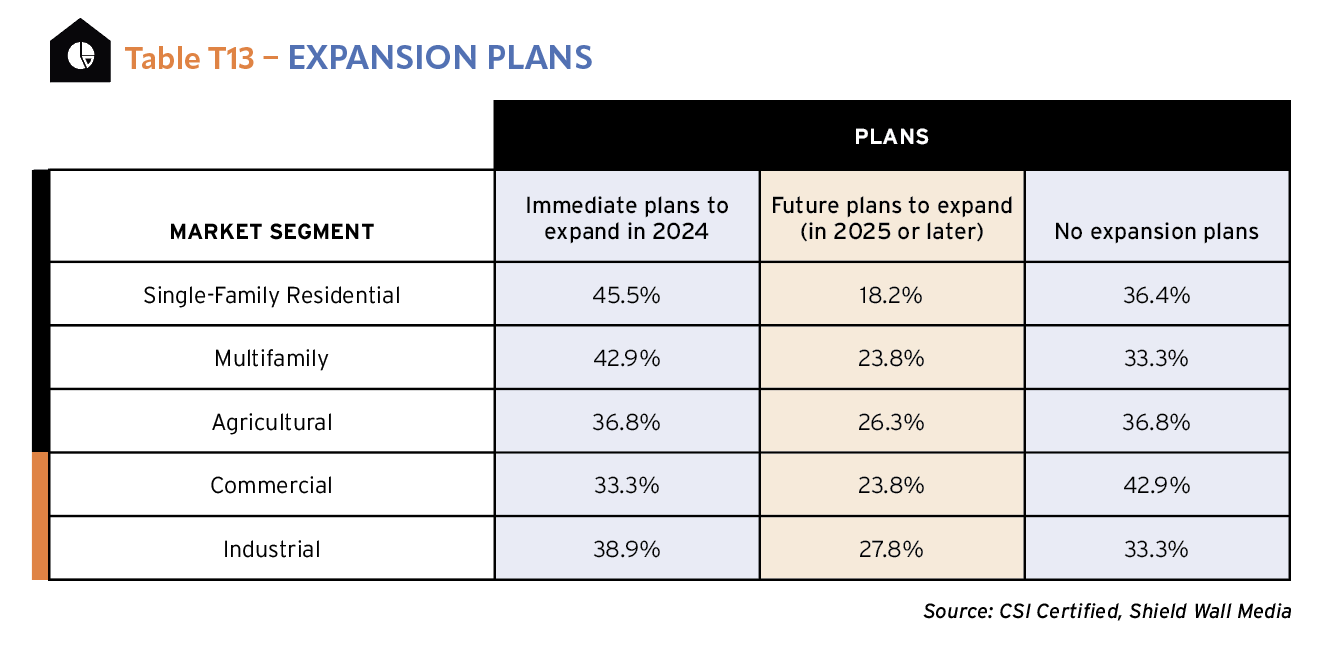

When asked about their plans to expand, respondents engaged in rollforming activity were relatively consistent across market segments, although they varied by sense of urgency. Roughly, about 65% of respondents say they plan to expand, although only 57.1% of survey takers in the commercial market segment admitted to that. T13

Single-family (45.5%) and multifamily (42.9%) companies were more likely to have plans to expand in 2024 than the other segments. In fact, rollforming companies serving the single-family market were far less likely to have plans to expand in the future than the other segments – even commercial – with 18.2% of them reporting they will likely put off expansion. Firms in this market segment who have no plans to expand in 2024 are less likely than other segments to expand later.

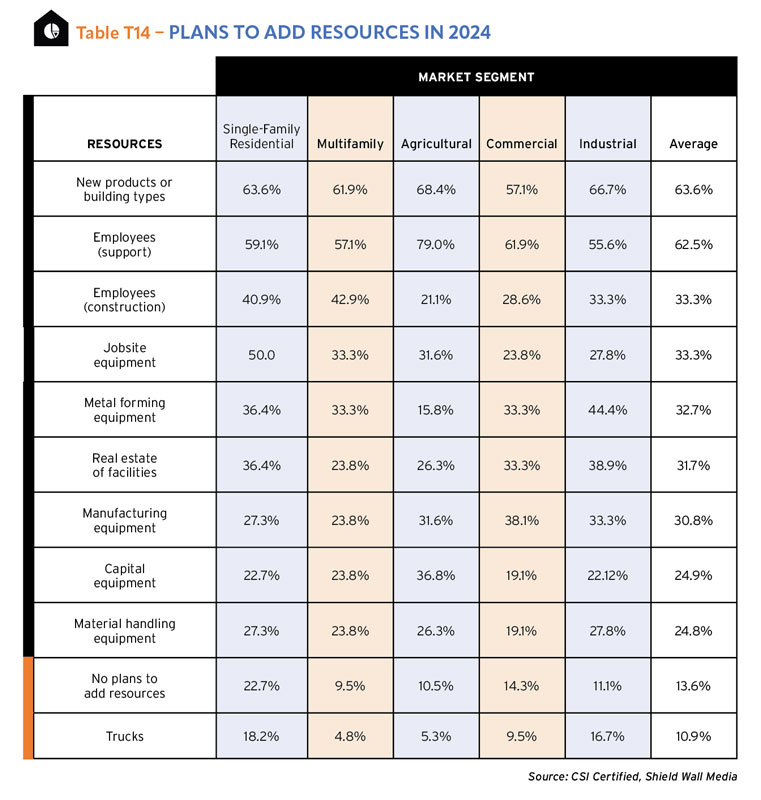

There is considerable agreement about what resources are needed in the market. Far and away, rollforming companies are looking to expand into new products or building types (63.6%) and add support employees (62.5%). This matches reporting in other sections where those two plans are at the top, but what is very different is the drop off among percentages saying they plan to add other resources. T14

With incredible consistency, the different groups of respondents in the CSI data have plans to add support employees at a much greater rate than they plan to add field workers. For this category, though, which would have a large number of manufacturing and distribution respondents rather than contractors, that makes even more sense. Unless a company is doing product installation, field employees aren’t a requirement.

About a third of respondents from companies engaged in rollforming activity say they plan to add field employees, jobsite equipment, metal forming equipment, real estate or facilities, and manufacturing equipment. Roughly a quarter anticipate adding capital equipment and material handling equipment.

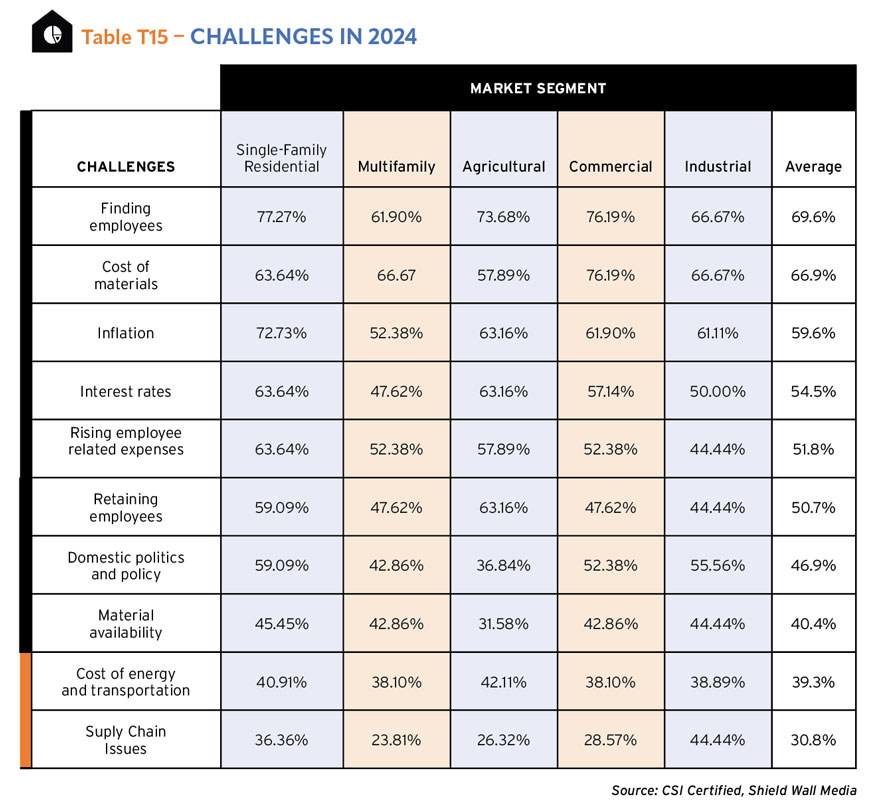

It’s all about controlling costs. That’s the challenge for the respondents to the survey who are engaged in rollforming activity. They may rate finding employees (69.6%) as the biggest challenge but the next four challenges are all cost control issues with rising cost of materials (66.9%) leading the way followed by dealing with inflation (59.6%), adjusting to higher interest rates (54.5%), and managing rising employee-related expenses (51.8%). T15

The shortage of skilled labor comes back into the equation where 50.7% of our survey takers say retaining employees is a challenge. As employee wages increase, staff can get a wandering eye, looking for the better opportunity down the road. Keeping them happy in the workplace is becoming increasingly important. As everyone has learned, the cost of hiring a new employee far outstrips the cost of retaining an already trained one.

The other issue that seems to be on the front of respondent’s minds is material availability (40.4%) and its related cousin, supply chain issues (30.8%). The days of long lead times seem to be mostly in the past, and contractors who were stockpiling supplies have begun to rely on their suppliers for their warehousing again. But the concerns don’t seem to have disappeared completely.

Check out the whole Construction Survey Annual & Market Data 2024!