AGRICULTURAL, RESIDENTIAL, AND LIGHT COMMERCIAL

CONSTRUCTION DATA

Companies that work in rural areas need to learn how to be flexible. Large metropolitan areas give companies the opportunity, especially contractors, to focus on very narrow niches. But there just isn’t enough of a specific kind of work in rural areas to grow a company, provide career paths for employees, and generate the revenue and profit that small businesses can contribute to the well-being of a community.

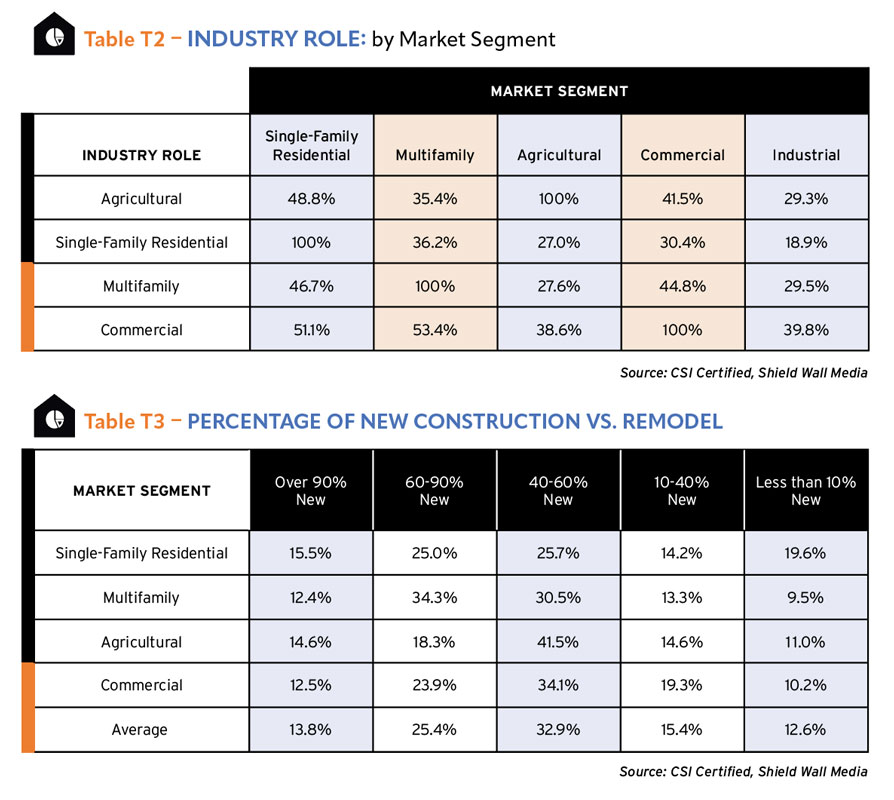

The Shield Wall Media CSI survey looked at companies serving the rural builder market by focusing on companies engaged in single-family, multifamily, commercial, and agricultural construction. As is shown later, there is considerable crossover among these market segments within one company.

In many markets, it’s not unusual to find a commercial contracting company also doing multifamily work, but it is unusual to find a company that fits in all four of these segments. Unless it’s a rural builder.

Characteristics of Rural Builders

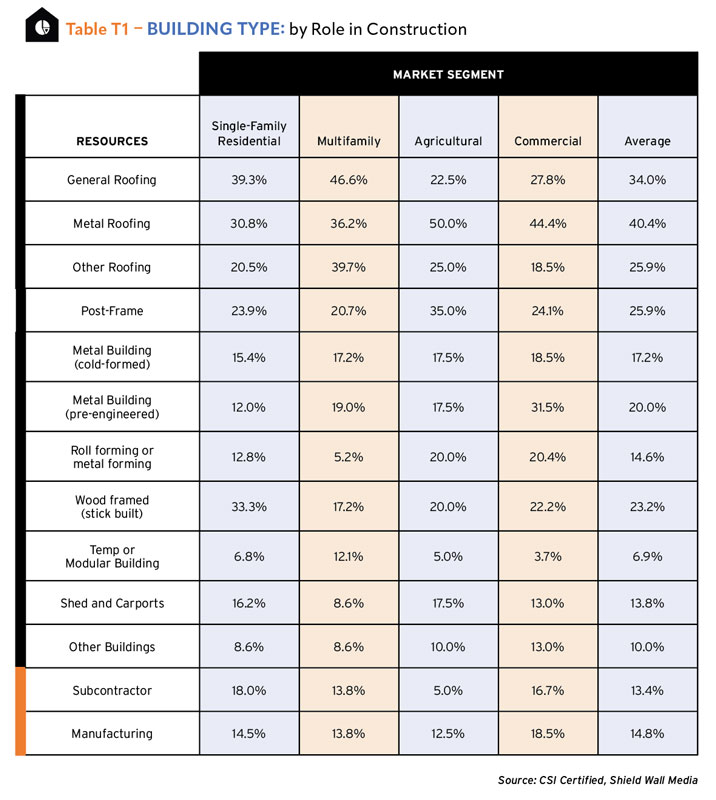

Companies engaged in agricultural construction are far more likely than other construction companies to build post-frame buildings or use metal roofing. That’s according to the survey of nearly 300 designers, contractors, distributors, and manufacturers. In agricultural construction, the table shows half of them use metal roofing compared to only 30.8% who are engaged in single-family residential work. The table also shows that a high proportion of companies engaged in commercial construction usemetal roofing (44.4%). T1 & T2

Interestingly, agricultural companies are less likely to do general roofing work (22.5%) than other companies serving these construction markets. Multifamily companies are most likely; 46.6% of them say they do general roofing work.

When looking at cold-formed metal buildings, the rate of involvement by role in the construction is remarkably consistent. Across all cohorts, between 15% and 19% do this building type. For pre-engineered metal buildings, commercial contractors are most likely to specify and construct this building type (31.5%) than any other, while single-family contractors (12%) are least likely.

Two other building types show significant variations depending on the type of company doing them. Companies in the single-family residential arena are most likely to construct wood-framed buildings (33.3%) while no other cohort raised to the 25% likelihood of usage rate. This isn’t surprising given that the residential construction market has never made a transition from wood framing to light-gauge steel framing at a significant degree.

The final building type with variation is sheds and carports. (See Section 7 for more information on this building type.) Multifamily companies are least likely to sell and install sheds and carports (8.6%), and both agricultural (17.5%) and single-family (16.2%) companies are most likely.

The flexibility rural builders need to develop is shown in how companies who are engaged in specific market segments also cross over to execute in other market segments. About a third of single-family residential builders also do multifamily projects, 27% do agricultural work, 30.4% do commercial construction, and 18.9% work in the industrial market segment.T2

Companies engaged in commercial construction are the most likely to work in the other market segments. In every segment, the commercial companies participate at the highest level of all types of companies.

The most common type of additional segment agricultural builder contractors move to is single-family residential. About half of the companies engaged in agricultural (48.8%), multifamily (46.7%), and commercial (51.1%) also work in single-family residential. This may include new home construction and residential remodeling. The only similar level of crossover is 53.4% of commercial contractors also do multifamily, but those two market segments are very tightly entwined and demand similar design and construction expertise.

Companies doing single-family construction are least likely to do industrial construction. Again, there are such wide disparities in requirements – from codes, product familiarity, to construction techniques – that it takes a remarkably large or flexible company to handle both kinds of work.

Agricultural work is often viewed as a kind of specialty niche, making it more difficult for companies to cross over to that market segment. Only 27% of single-family companies. 27.6% of multifamily, and 38.6% of commercial companies pick up agricultural work. The building types, the customer base, and the product knowledge are nearly as specific as the industrial sector. However, for rural builders, agricultural work is a mainstay of their business.

In May 2022, the American Architectural Institute’s (AIA) Billing Index reported reconstruction projects exceeded new construction. Typically, 30% of billings are reconstruction, but the trend is changing, and AIA Chief Economist Kermit Baker, Hon. AIA, Ph.D., said at the time, “We are going to move toward an increased share in reconstruction and a decreased share in new construction.” T3

On average, companies engaged in single-family and multifamily residential, commercial, and agricultural construction do about half of their work in new and half in reconstruction. 32.9% of these companies do between 40 and 60% of their business in new construction, the rest in remodeling.

About 34% of multifamily companies do between 60 and 90% new construction and when you combine that with those that do more than 90% new construction (12.4%) for a total of 46.7%, it is the segment most likely to do new construction. The least likely to do new construction are companies engaged in the agricultural segment, with only 32.9% saying more than 60% of their work is new construction.

The most likely to do remodeling work are companies engaged in single-family construction, where 33.8% do less than 40% of their work in new construction. The likelihood of a company to do almost all new construction, more than 90%, is roughly equal across all cohorts with companies engaged in multifamily and commercial construction being the least likely.

Projected Industry Growth

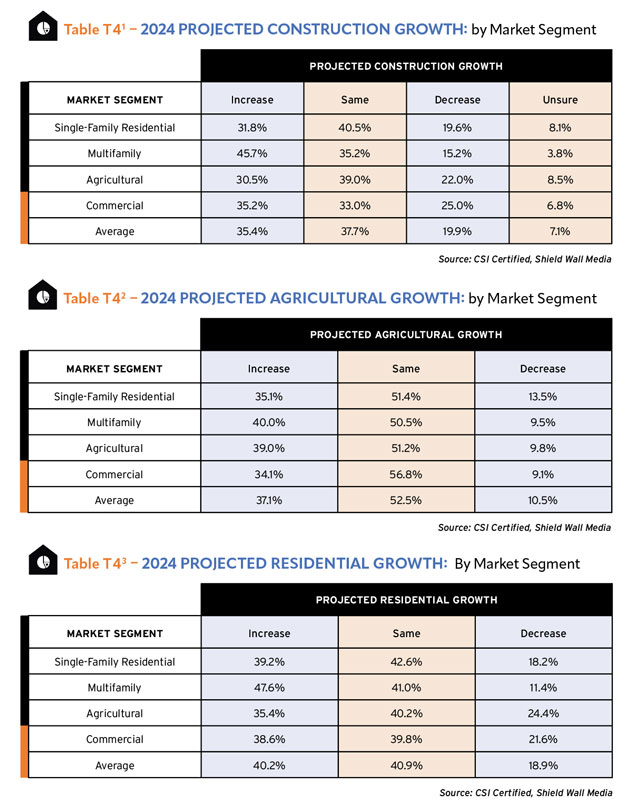

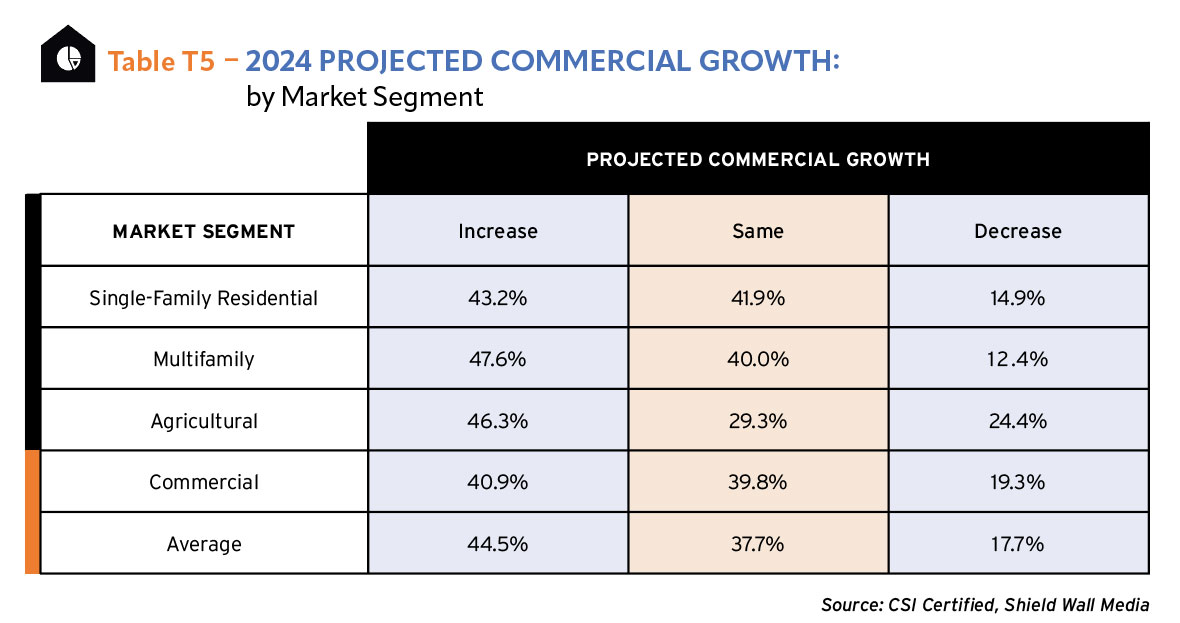

Attitudes toward the prospects for the construction industry can vary by what a person sees from their vantage point. For example, companies engaged in multifamily construction are far more likely to see improvement coming for the construction industry than other cohorts. 45.7% of multiple-family companies think the industry will improve in 2024, but on average, only 35.4% of all cohorts see an improvement coming. Every other group – single-family, agricultural, and commercial – are less positive. T4-1,2,3 & T5

Generally, these companies feel the status quo will continue, but 25% of commercial companies and 22% of agricultural companies project a decline.

When you look at this group of tables for specific market segments, a different story begins to emerge, and you can see where companies engaged in residential, agricultural, and commercial work believe the growth will occur.

Almost without exception, these types of companies expect agricultural construction to remain the same in 2024 with more than half saying it will. Just more than a third think it will increase, and none of the cohorts is significantly different from that.

But the residential and commercial construction market garner a much more positive attitude with 40.2% saying residential activity will increase in 2024 and 44.5% projecting commercial activity increases. For residential projections, part of that is driven by the very strong belief among companies engaged in multifamily work (47.6%) that it will go up. This positive attitude toward the prospects for the industry among multifamily companies will arise in other areas of this report as well.

While companies serving these markets are generally bullish about the commercial and residential markets either staying the same or improving, they are not nearly as confident that they won’t decline. On average, 18.9% of these companies think the residential market will shrink, and 17.7% project a decline in commercial activity.

Those stand in stark contrast to projections for the agricultural market where only 9.8% of companies doing this kind of work expect the market to decrease.

Company Size and Growth Projections

The rule of thumb in construction is that 80% or more of the firms are small companies. They often have one owner and that person may also work on the jobsite. This is especially true on the residential construction side where small home improvement contractors dominate the number of total contractors.

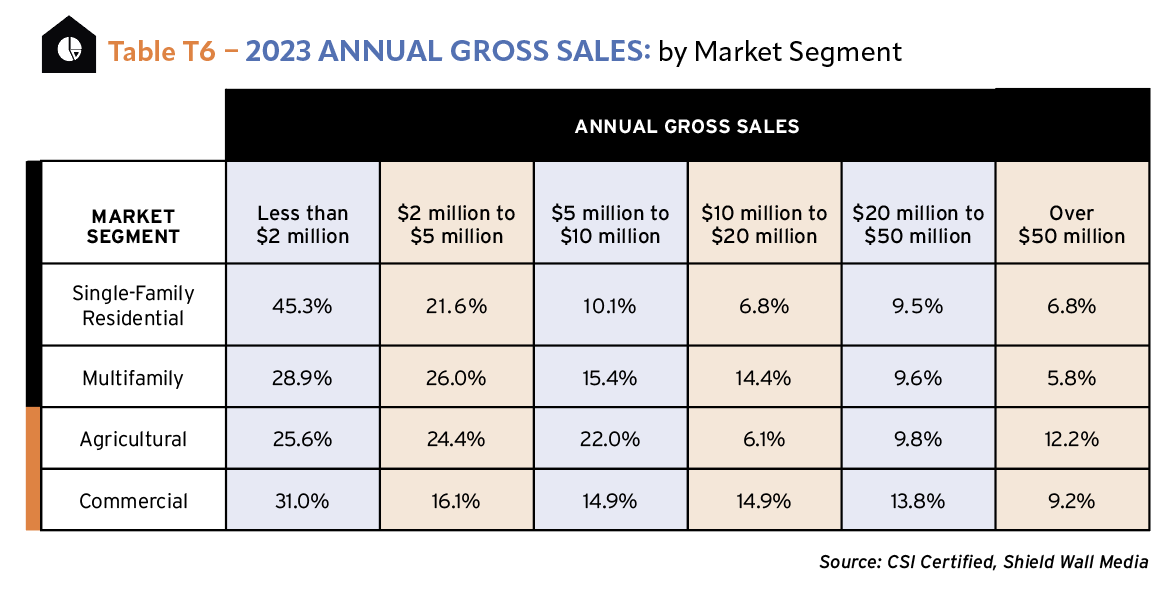

Looking at the CSI survey of companies doing single-family, multifamily, commercial, or agricultural work, you can plainly see the smallest firms – those with gross sales less than $2 million – are dominated by the single-family residential companies. More than 45% of single-family companies have revenues at the low end of the scale. The other segments are grouped relatively closely. T6

But differences do begin to appear among commercial, agricultural, and multifamily participants. Companies doing agricultural work are far more likely to have revenues in 2023 greater than $50 million. And there seems to be a high complement of agricultural companies with between $5 and $10 million in gross sales with 22% reporting sales from last year in that range. That far exceeds the other cohorts.

For the most part, the companies decrease in size in lockstep with a couple of exceptions. There is noticeable drop in the revenue range $10 to $20 million for single-family and agricultural companies.

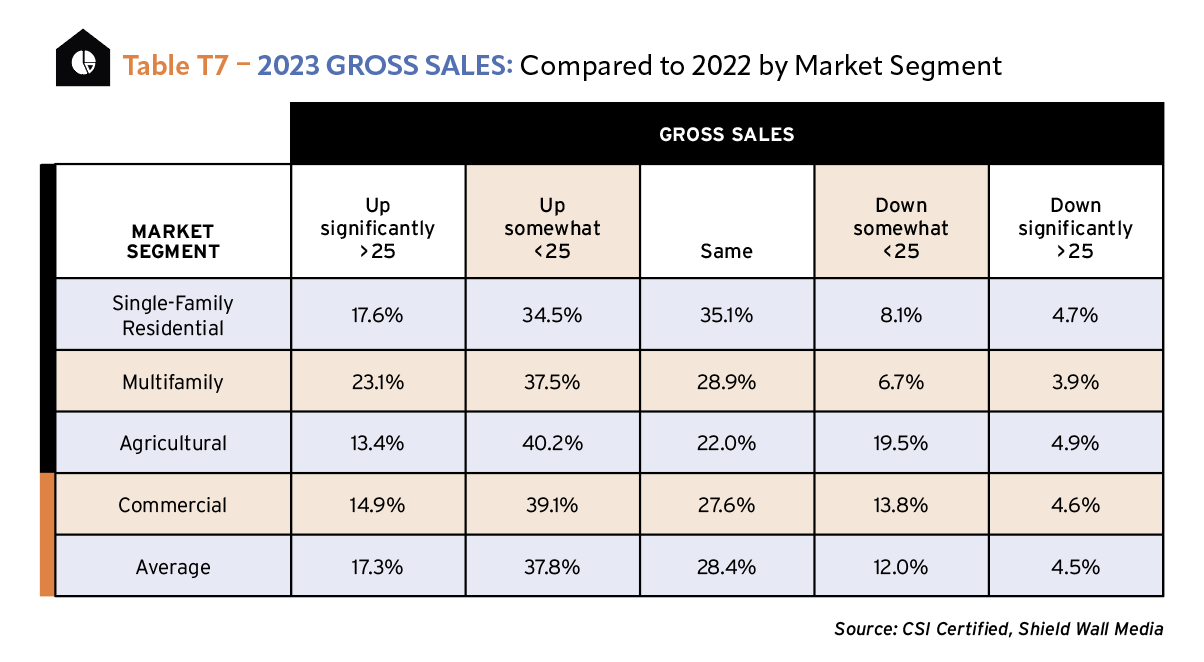

In 2023, the vast majority of companies engaged in single-family, multifamily, commercial, and agricultural construction report sales that were the same or higher than in 2022. On average, only 16.5% report a decline, and of those, only 4.5% report a decline greater than 25%. T7

The multifamily cohort reports that 23.1% of them experienced significant sales growth of greater than 25%. That might also help explain why this cohort was the most bullish about the growth of the construction industry over all in 2024. More than 45% of them said 2024 would be a good year for construction.

Companies serving the agricultural market tended to be somewhat pessimistic on the prospects for the construction industry in 2024, but not in excess of the other cohorts. However, they do report a decline in gross sales for 2023, with 19.5% of them saying they were down less than 25% and another 4.9% reporting a drop of greater than 25%.

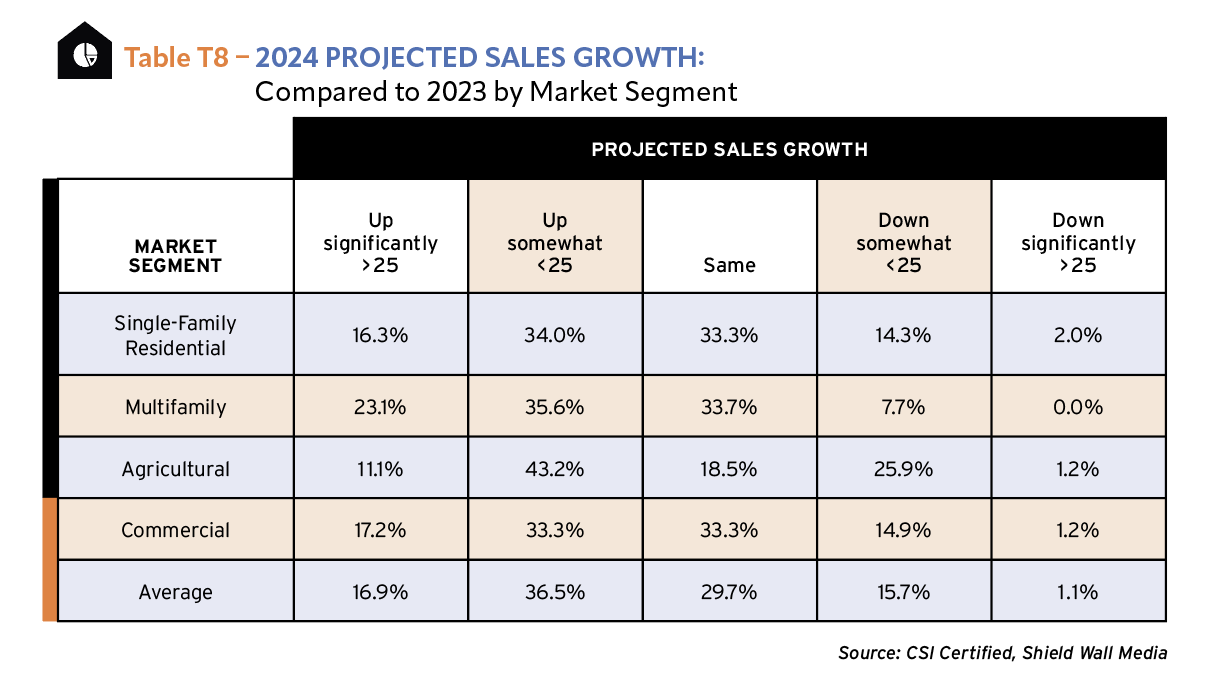

When asked to project sales for 2024, companies serving the agricultural market again were less optimistic than the other cohorts. More than a quarter of them expected declines of less than 25%. However, that is somewhat offset by the expectation that gross sales will increase among this cohort with 43.2% saying they will rise less than 25% and 11.1% projecting a significant increase of greater than 25%. T8

Of all the cohorts, multifamily companies are, again, the most optimistic about 2024. More than 58% say gross sales will increase this year, with 23.1% predicting a significant increase of greater than 25%. Only 7.7% of companies engaged in multifamily work expect to see declines.

To put this in another context, Dodge Data and Analytics projects a 7% increase in the construction industry for 2024 after only a 1% increase in 2023. That includes the entire industry – infrastructure, sewer and water, transportation, etc. – and this smaller sampling of the industry may have a very different response to market conditions than the entire industry. This group does not get a lot of Federal infrastructure money flowing into its projects.

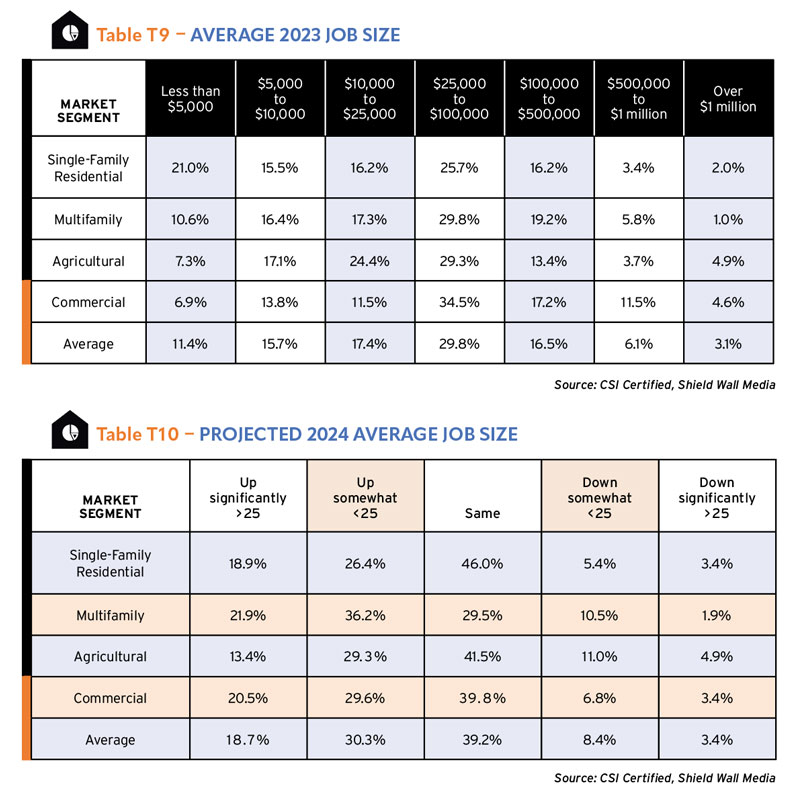

In 2023, 21% of companies engaged in single-family residential construction reported having a job size of less than $5,000. There isn’t much that can be done these days for that low price other than things like a new water heater installation, front door remodel, or a repair project. But those are exactly the kinds of jobs that companies working in this segment might have. (And they can be quite profitable if managed correctly.) T9

The highest percentage of jobs done by companies engaged in single-family, multifamily, commercial and agricultural construction fall in the $25,000 to $100,000 range, but even that doesn’t represent a plurality of the work. On average, only 29.8% of companies do that work, with 34.5% of commercial companies reporting job sizes in this range.

With a couple of exceptions, the average job size for these companies fits a traditional bell curve. Most of the jobs fall in the middle with declining participation as the jobs get either larger or smaller. The first exception is that companies doing commercial work (34.5%) are more likely to have average job sizes between $25,000 and $100,000 than the other cohorts. But that difference isn’t notably significant. That’s only about 15% higher than the next highest.

Commercial companies are far less likely to have projects between $10,000 and $25,000 with only 11.5% of them working in this range, while 24.4% of agricultural companies have an average job size in that range.

Companies doing agricultural work did report a greater instance of doing reconstruction work than other cohorts, and that could explain the smaller job size.

The other big outlier is the 11.5% of commercial companies with average job sizes between $500,000 and $1 million, and for the most part that does sound like the sweet spot for a lot of light commercial work.

It would be unusual for companies to suddenly see a change in average job size unless one or two things happen. The company may have moved into new services, such as adding large warehouses to it’s mix of traditional retail work. It could have added a maintenance and repair division to the company, reducing the average job size. Or it might be a small company that had an exceptionally large job that threw off the average job size. T10

For the most part, that is borne out in the projects companies engaged in single-family, multifamily, commercial, and agricultural report about their expected average job sizes in 2024. Very few report declines in job size with 8.4% on average saying they will be down somewhat and 3.4% on average saying they would be down significantly.

Companies reporting increases in average job size could be in large part due to increases in material costs and overall inflation, which are driving up prices.

The unique points to be made in projection of job size for 2024 is that multifamily companies are far less likely to predict the status quo will remain; fewer than 30% report that, and they are slightly more likely to expect an increase with a total of 58.1% projecting an increase in average job size.

Future Opportunities and Challenges

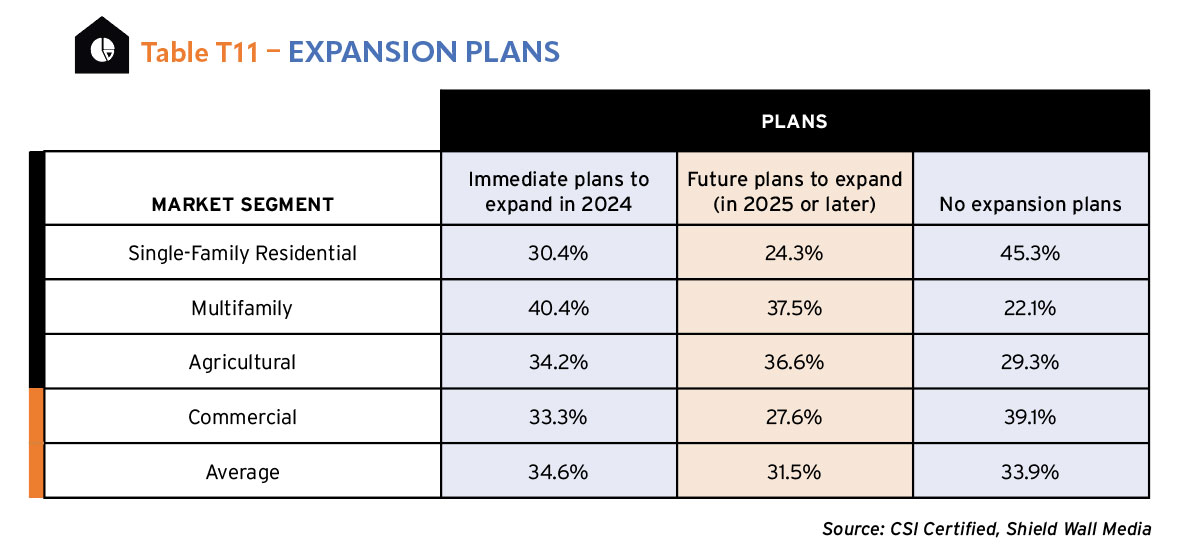

The true test of a company’s feelings about the future are its plans to expand or add resources. About a third of the companies doing single-family, multifamily, commercial, or agricultural construction report they have no plans to expand. The firms engaged in single-family work are more adamant about that with 45.3% saying no to expanding, but only 22.1% of multifamily companies don’t have expansion plans. The multifamily companies have been the most optimistic in every aspect of the survey, so this isn’t surprising. T11

About a third of companies have plans to expand in 2024, which is also pretty optimistic, and again multifamily companies are leading the way with 40.4% of them expecting to expand in 2024.

We asked CSI survey respondents to tell us what resources they planned to add in 2024. When you look at the companies who serve the single-family, multifamily, commercial, and agricultural markets you see a clear need for more employees. As much as the industry talks about the shortage of skilled labor, it is support employees (skilled in their own way) that are most in demand among these companies. T12

Adding new products and building types (average 40.2%) ranked second with construction employees (35.9%) coming in third. It should be noted, though, that the very low reaction from single-family companies to adding these resources are pulling the averages down. Only 31.1% of single-family companies plan to hire support employees, and only 31.1% plan to add new products or building types. The other cohorts are roughly grouped at the same percentages.

More than 37% of single-family companies do report a plan to add construction employees, and 43.3% of multifamily companies expect to put more people on the jobsite, which jibes with residential construction industry’s claimed need of skilled workers.

When it comes to investments in capital equipment, companies working in these market segments still have plans to add resources, but not at as high a rate as they would human resources. About a quarter of the companies plan to get more jobsite equipment, 18.2% are looking at manufacturing equipment, and around 14% expect to add metal forming equipment and trucks.

Across the board, single-family companies are less likely to indicate they plan to add resources with 20.3% on average reporting they will add resources compared to 26% on average for multifamily and commercial companies.

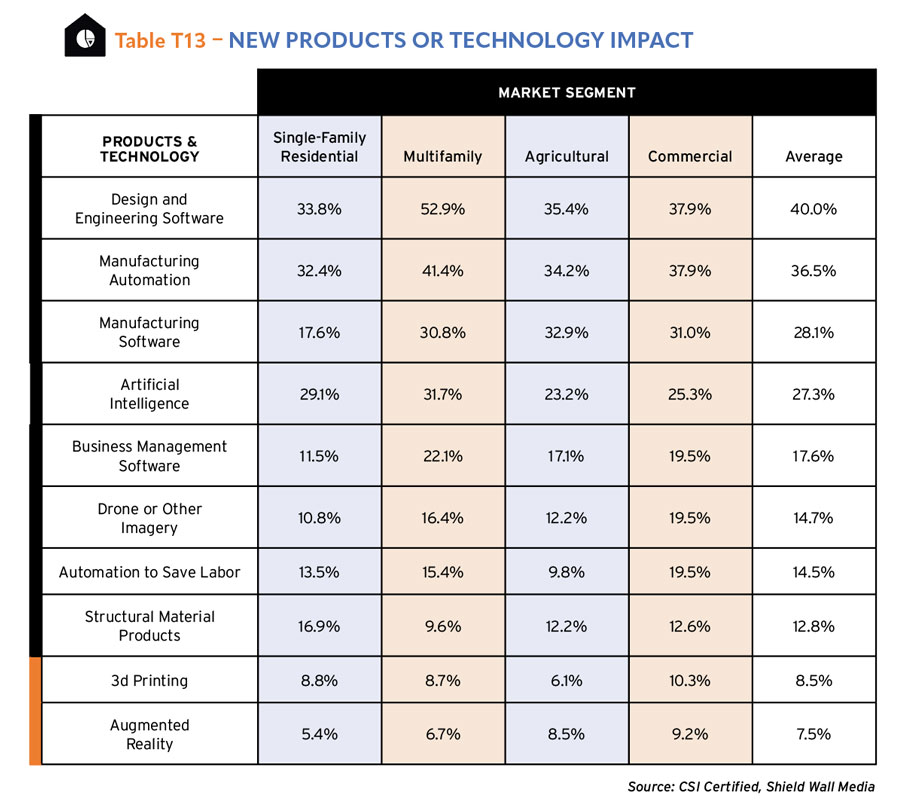

According to our survey, companies working in the multifamily construction market are far more likely to think design and engineering software will impact their businesses than the those working in commercial, single-family, or agricultural. Fully 52.9% of those companies expect to see an impact from that software, but only 33.8% of single-family companies expect to see it. It is a little surprising, given how close commercial and multifamily companies have tracked in this survey that they are not in lockstep here. T13

Manufacturing automation and manufacturing software are reported to be the next most impactful innovations for these businesses. That is, of course, excepting single-family companies; 17.6% think manufacturing software will have an influence, compared to the average of 31.1%.

The fourth technology to be recognized as impacting their businesses would not even have been on this list a year ago. Artificial intelligence (AI) is sweeping across marketing and design firms as ChatGPT provides a tool for generating marketing and sales copy quickly and easily. AI also has been paired with design software to make renderings even more lifelike.

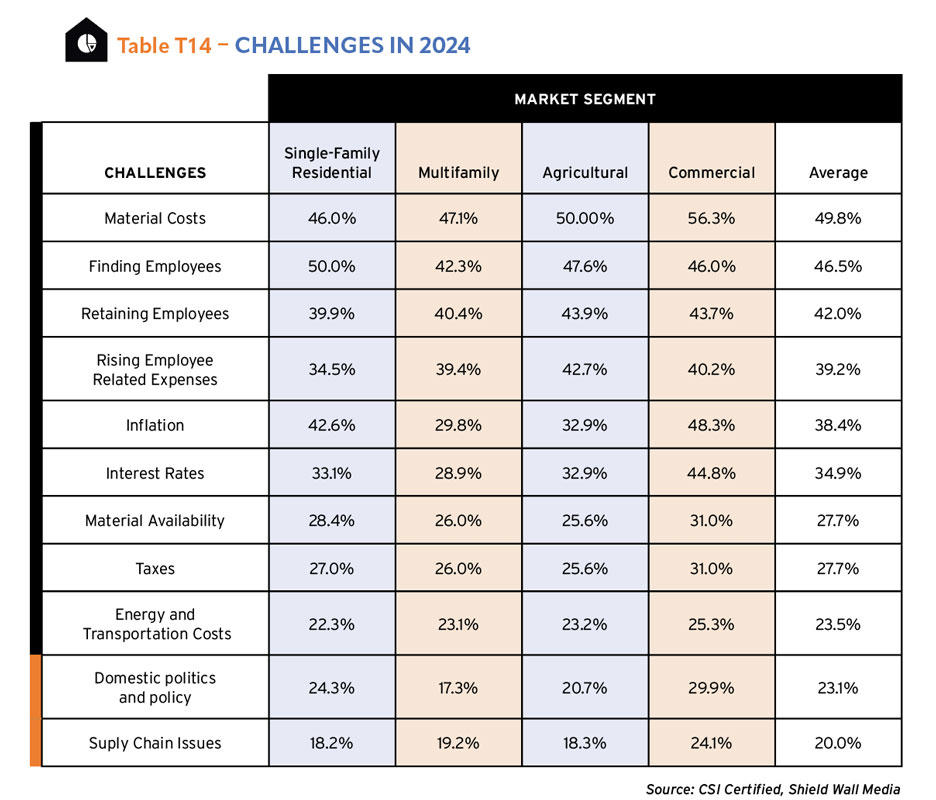

What keeps owners of companies serving single-family, multifamily, commercial, and agricultural markets awake at night? The challenges on this chart. T14

And it’s clear the people in commercial companies are far more worried about these challenges than others. For four of the challenges – material costs, inflation, interest rates, and domestic politics – companies engaged in commercial construction are far more likely to be concerned about these issues than companies in other market segments. Three of those challenges are directly related. Material costs, inflation, and interest rates have strings that attach them. You can’t change one without affecting the others. And, it could be argued, domestic politics is tangentially related.

For these companies, finding and retaining employees is the big issue after managing material costs. It’s the well-worn mantra of the industry that there is a labor shortage. However, even in best of times, managers worry about human resources because managing employees is never easy.

Other than commercial companies serving as an outlier, there is very little difference among these cohorts. Single-family companies are concerned about inflation and domestic politics at a higher rate than average, but not as high as commercial companies.

Check out the whole Construction Survey Annual & Market Data 2024!