GENERAL CONSTRUCTION INDUSTRY DATA

By Paul Deffenbaugh, Contributing Editor

Over the last few years, the construction industry has been a leading economic driver of the overall U.S. economy. Housing construction has been soaring, recuperating from the devastation of the housing recession in 2009 to 2011. Commercial construction, too, has been a force of economic improvement, providing millions of jobs and offering workers a way up to the middle-class.

There have been winners and losers, of course. Online shopping, for example, has hurt the retail industry but has been a shot in the arm to the warehouse market. Federal government infrastructure investments as well as improved state and municipal budgets that were gutted by the COVID-19 pandemic have helped lift the public construction sector.

The following tables provide an overall view of the construction industry as well as some predictions for 2024.

Characteristics of General Construction

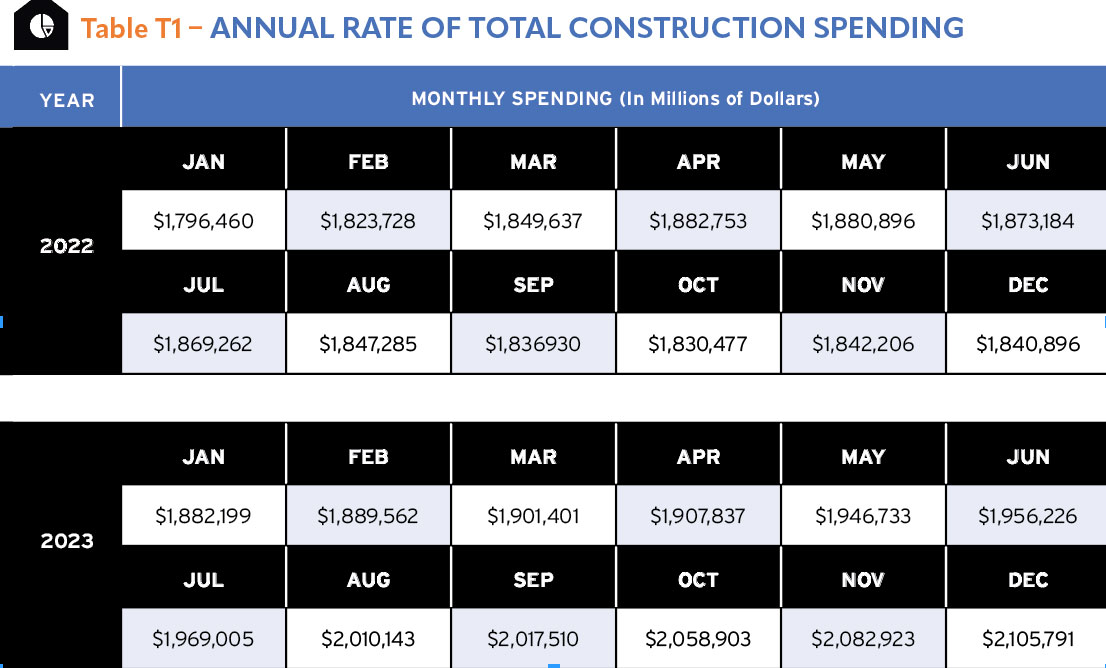

Total construction spending from 2022 through 2023 was buffeted by a variety of economic factors. Initially, as the global economy began to recover from the impacts of the COVID-19 pandemic, there was a surge in construction spending as governments and businesses invested in infrastructure projects and real estate development. This period saw a heightened demand for residential housing, spurred by low interest rates and changing housing preferences due to remote work trends. T1

As the supply chain disruptions intensified and inflationary pressures mounted, construction costs soared, leading to project delays and cancellations. Additionally, labor shortages in the construction industry further constrained output and drove up wages, adding to the cost escalation.

Overall, while the construction sector demonstrated resilience and adaptability during this period, navigating through unprecedented challenges, the volatile economic landscape underscored the importance of agility and strategic planning for construction firms to sustain growth and profitability amidst uncertainty.

When asked what in the last year had surprised him, Jim Bush, vice president of sales and marketing, ATAS International, Allentown, Pa., pointed to this issue specifically. “The resilience of the construction economy continues to be somewhat of a surprise,” he said. “Overall things seemed stable in the past year versus the turmoil that occurred in the preceding few years.”

Looking to 2024, the Dodge Data and Analytics forecast expects total construction to increase 7% to $1.2 trillion after growth slowed to just 1% in 2023, which is actually a decline of 2% when adjusted for inflation. Single-family residential construction will increase 9% and multifamily 14%, according to the forecast. Commercial construction is expected to actually decline 2%, while manufacturing goes up 16%.

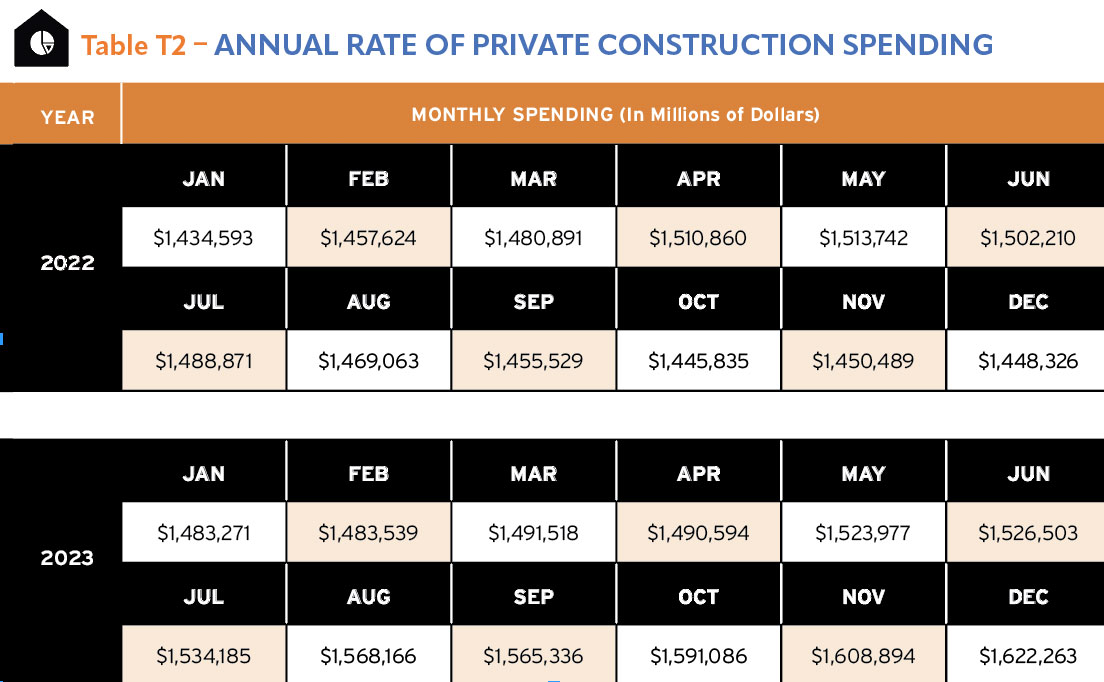

The private construction sector grew during 2022 and 2023. Low interest rates fueled the early growth as well as pent-up demand, and government stimulus measures. The housing market was a significant driver, with robust activity in both residential and non-residential sectors. The supply chain disruptions and labor shortages probably hindered the pace of growth. Overall, the period showcased the adaptability of the construction sector amidst fluctuating market conditions, underlining its essential role in economic recovery and development. T2

Associated General Contractors (AGC) anticipates declines in three sectors of the private construction industry in 2024. Lodging down 3%, retail down 15%, and private office down 24%. None of those are surprising considering the lingering impacts of the COVID-19 pandemic and the continued shift to online retail.

Big increases in the private sector, according to AGC, will come from hospitals (up 23%), other healthcare (up 22%), data centers (up 20%), manufacturing (up 15%), and warehouses (up 10%).

The national assessment is supported by reports from individual markets. Todd Carlson, president of A.J. Manufacturing Inc., Bloomer, Wis., says, “In Western Wis., we see demand for affordable housing booming along with related construction of infrastructure and construction related to general services such as restaurants, hospitality, retail, and medical facilities. We serve industrial and commercial markets as well as all aspects of the post-frame market and expect strength and growth certainly in revenue for our customers, despite some building fewer buildings or units. T2

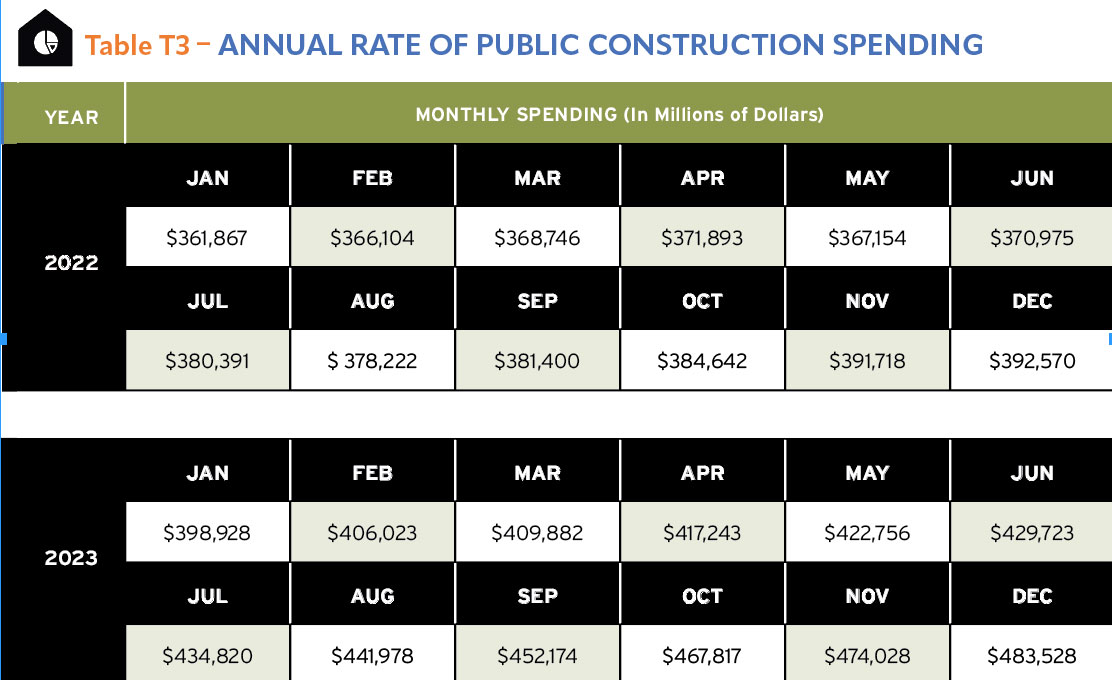

There was a lot of talk about shovel ready projects during the pandemic, but the U.S. had not been investing in infrastructure over the last several years at a rate to replace its deterioration so there was little that was shovel ready. Some of that has been addressed with the Infrastructure Investment Act, signed into law in November 2021. The act authorized $1.2 trillion dollars in infrastructure spending, of which $550 billion was new spending beyond what Congress had already planned to authorize.

AGC reports large increases in public construction, largely as a result of increased investment in infrastructure. Water/sewer, bridge and highway, transportation, and power sectors will see significant increases. For this audience, three sectors stand out: K-12 schools (up 18%), public building (up 15%), and higher education (up 15%), although higher education can include both public and private construction. T3

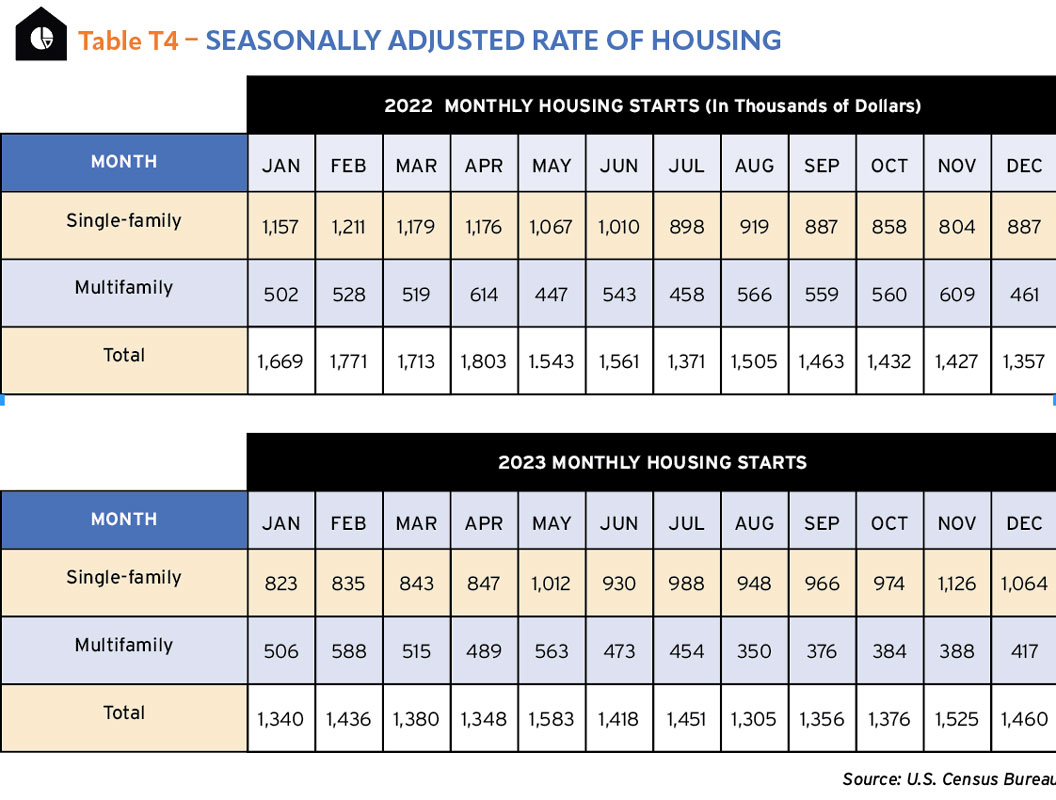

As interest rates have risen, the housing market has cooled after being red hot in 2020—2021. The year 2022 ended with 1.55 million starts, which was 3% lower than 2021. Single-family starts ended 2022 at 1.01 million, down 10.6%, which was not enough to offset the 15.1% increase in multifamily starts to more than 500,000. T4

The following year, 2023, the drop continued as housing starts declined to 1.42 million or 8.6% lower compared to 2022. Single-family starts declined 6% in 2023 compared to 2022, ending at 945,000 units. Multifamily finished 2023 with 469,000 units, well below the 548,000 started in 2022.

The National Association of Home Builders (NAHB) forecasts total housing starts for 2024 to clock at 1.37 million. That includes a 4.7% increase in single-family units to 988,000. The multifamily front is not as robust, though, starts are expected to fall 19.7% in 2024 to 379,000.

Much of that activity is predicated on an NAHB prediction that mortgage rates will decline to below 6.5% by the end of 2025. “We expect rates to be in the high 5% range,” said NAHB Chief Economist Robert Dietz. “This is good news for builders, housing demand, and housing affordability.”

He also points out the country needs more than 1.15 million single-family homes a year to reduce its housing deficit. Demand is greater than supply.

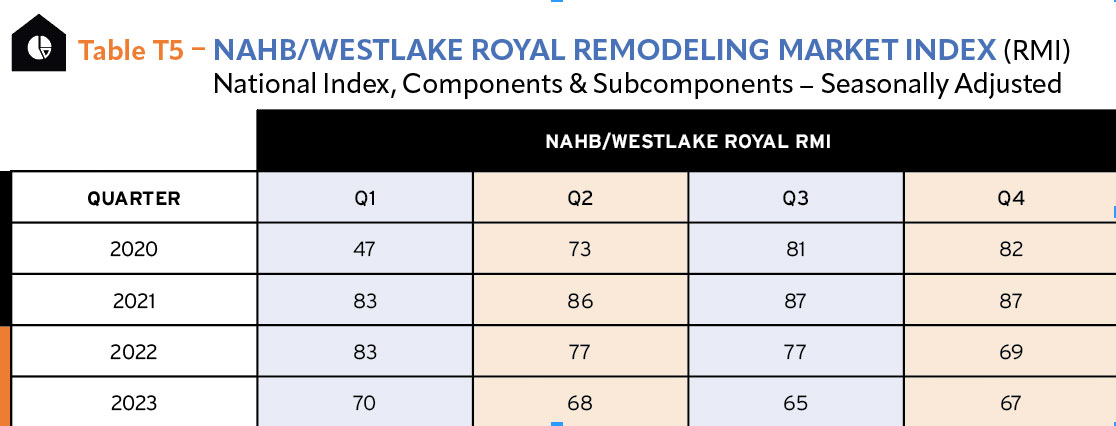

NAHB produces the NAHB/Westlake Royal Remodeling Index, which is based on a quarterly survey of remodelers. They are asked to rate the remodeling market on five aspects. A rating above 50 is good, below is poor. T5

The index through 2020 and 2021 was exceptionally high, which reflected the hot market created by low interest rates and people suddenly having to spend more time in their houses. Rising interest rates have cooled activity since, but the index remains high.

NAHB expects residential remodeling activity to remain relatively flat in 2024 followed by a 2% gain for 2025 as the existing home sales market improves.

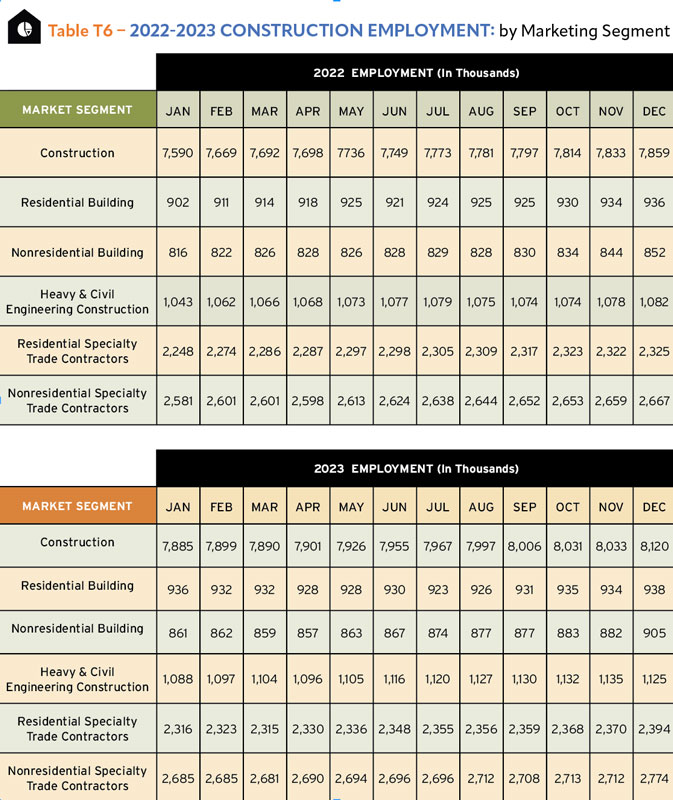

If there has been a story driving the construction industry for the last several years, it is the persistent shortage of skilled labor. When you look at the boom in the growth of construction employment from 2022 to 2023, it’s hard to believe there could have been even more employment if companies had been able to fill open spots. Since the beginning of 2022, the number of jobs in the construction industry has increased from 7.6 million to 8.1 million. T6

Over 5 million of all construction jobs are with specialty trade contractors and just under half of those fall in the residential market. The other three segments, residential building, nonresidential building, and heavy and civil engineering construction account for about 3 million of the total jobs.

Wayne Troyer, Acu-Form, Millersburg, Ohio, speaks to the flexibility of the construction workforce today. “In our area, in a lot of construction,” he says, “crews work in at least three of these: residential, agriculture, commercial, or industrial.”

Among the challenges companies in the industry face is filling these position, and that is borne out in the CSI survey where finding and retaining employees rank as the second and third most difficult challenges in 2024 after managing the rising cost of materials. (See below.)

CSI Survey Attitudes

The markets served by Metal Roofing, Rural Builder, Frame Building News, Rollforming, and Garage, Shed, Carport Builder among the other publications and industry shows from Shield Wall Media serve a unique niche across the construction industry. Getting information about the performance of these markets and their audiences is essential to serving them.

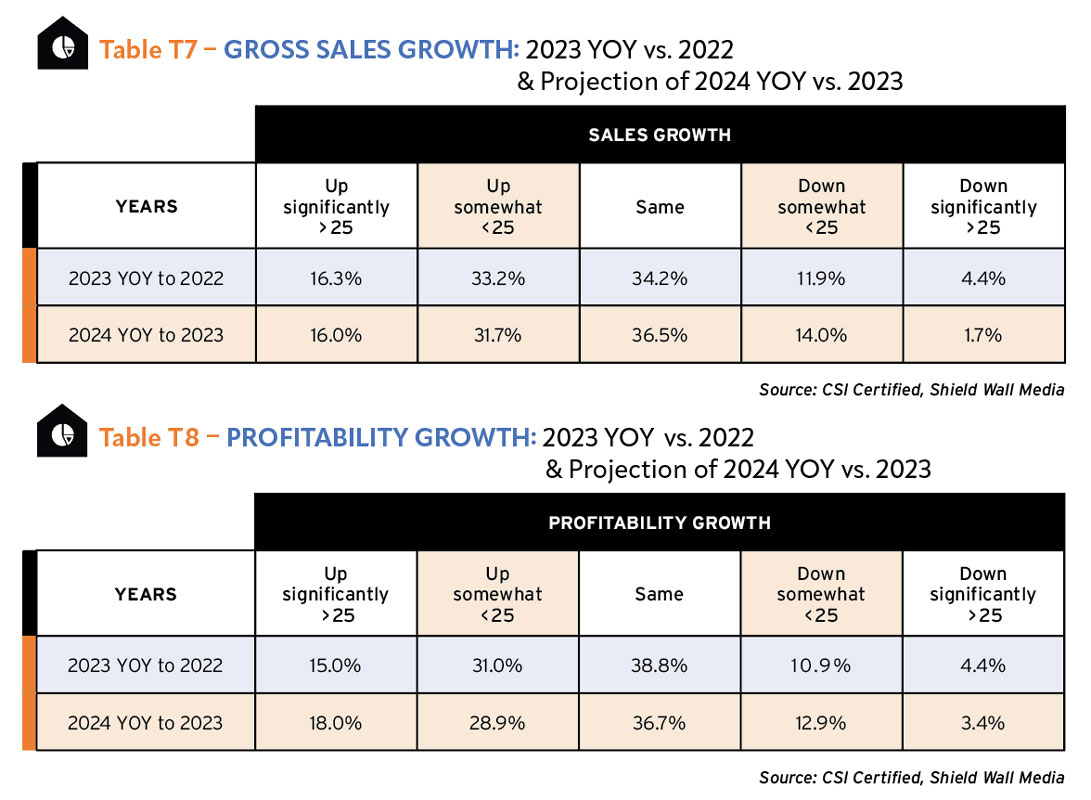

Shield Wall Media surveyed their audience in November and December 2023. About 300 respondents across the industry completed the form. The following tables look at how these unique market segments have performed since 2022 and look forward to the next year. T7

For all intents and purposes, the expected gross sales growth of companies for 2024 is roughly the same as they reported the previous year. The number of companies who saw increases in sales in 2023 (49.5%) is roughly the same as those who say they will see increases in sales in 2024 (48.7%).

There is more difference in those who expect to see a significant decline in gross sales in 2024 compared to what was experienced in 2023. Only 4.4% of companies experienced a greater than 25% reduction in sales 2023, but an even smaller number (1.7%) anticipate a similar decline.

That matches the reports and predictions of the overall construction economy, which did see a slight decline of 1% in 2023 according to Dodge Data and Analytics. But Dodge anticipates a rebound this year with a 7% jump.

Maintaining profitability while experiencing significant increases or declines in sales can be a struggle for any business. Across the industry, according to our survey, companies were substantially able to hold the line in 2023. Just over 16% of companies report declines in sales in 2023, but only about 15% report a decline in profitability. In fact, 38.8% of respondents say their companies maintained profitability in 2023. T8

Looking forward, as with most surveys on the construction industry, respondents are both optimistic and pessimistic. Fewer expect profits to remain the same in 2024 (36.7%), but that is almost identical to the percentage of survey takers who think gross sales will remain the same (36.5%).

Still, when you look at significant increases in profitability, 18% of respondents expect to see more than 25% increase in profits in 2024 compared to the 15% who reported a similar increase in 2023.

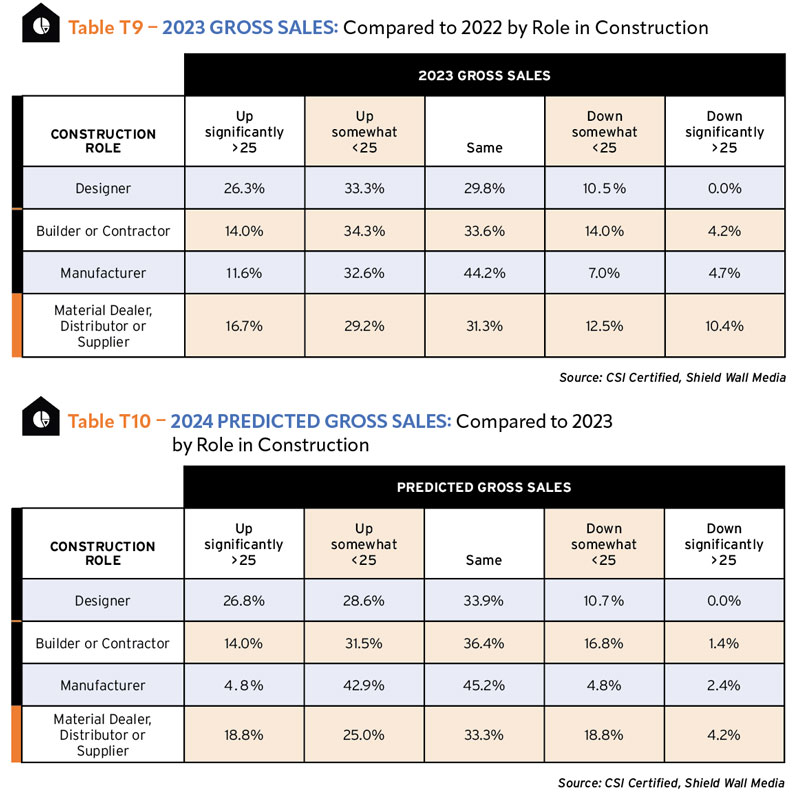

More designers report significant sales growth in 2023 compared to 2022 than any other participant in the construction process. More than 26% of designers said their sales increased more than 25% in 2023. The next closest cohort is distributors where only 16.7% say they saw significant sales growth. T9

When you add the significant sales growth to some sales growth (less than 25%) designers again far outstripped the others with 59.6% reporting an increase. Manufacturers are far more likely to report sales in 2023 (44.2%) that were approximately the same as those in 2022. Interestingly, manufacturers were less likely to report a decline in sales, with only 11.7% doing so. Although no designers report declines greater than 25%.

Distributors and contractors fall mostly in lockstep with roughly the same reporting increases and declines with the exception that contractors (4.2%) are less likely to report a significant decrease in sales than distributors (10.4%) .

It is often said sales growth in the design part of the construction industry is a leading indicator for the industry since those building contracts land on designers’ desks first. Designers again lead the optimism parade in their expectations for 2024 with 26.8% expecting significant sales growth and another 28.5% (for a total of 55.3%) saying sales will grow. While manufacturer respondents don’t think their sales will grow significantly in 2024, they do think sales will grow with about the same percentage reporting growth in 2024 as they had in 2023. T10

Distributors (23%) and contractors (18.2%) are most likely to anticipate gross sales declines in 2024 but no one expected significant declines to be as likely as occurred in 2023.

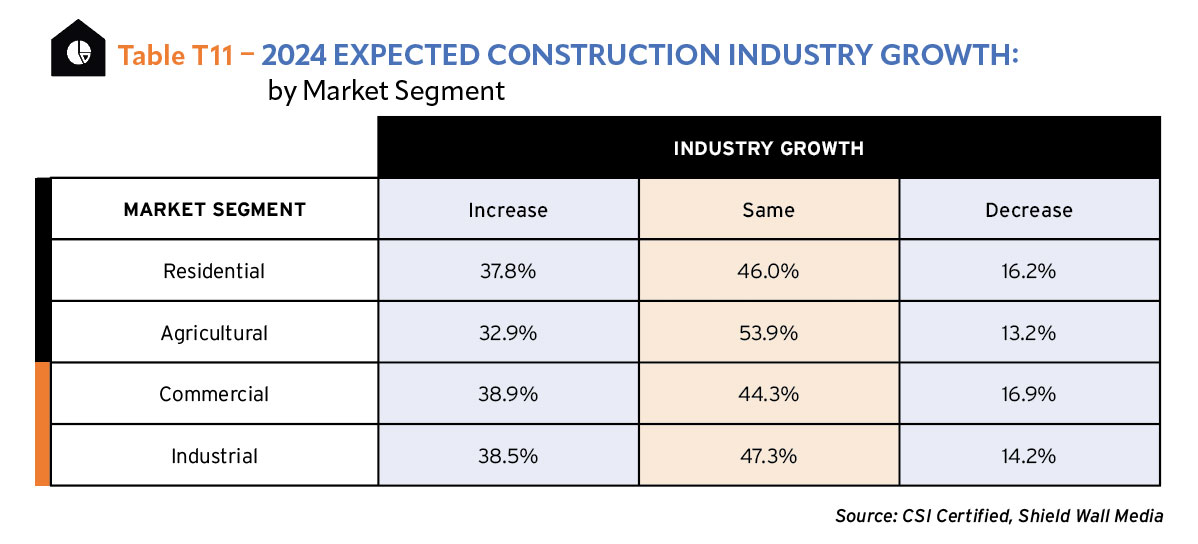

The following charts look at the overall expected growth in different market segments, then dig into the expected growth in specific regions by each market segment. T11

Overall, our respondents generally agree on the growth of the residential, commercial, and industrial market segments. Just around 38% of them see those segments increasing in 2024. However, only 32.9% expect the agricultural market to increase.

While that sounds less than optimistic, when you identify which segments our survey takers expect to decline, the agricultural market is the strongest with only 13.2% anticipating a cooling of the segment. Overwhelmingly, survey takers think the agricultural market will remain the same in 2024 with 53.9% selecting that option.

About the same number of respondents feel the residential and commercial market segments will see a decline this year (16.2% and 16.9% respectively). And slightly fewer are more optimistic about the industrial market, where 14.2% anticipate a slowdown.

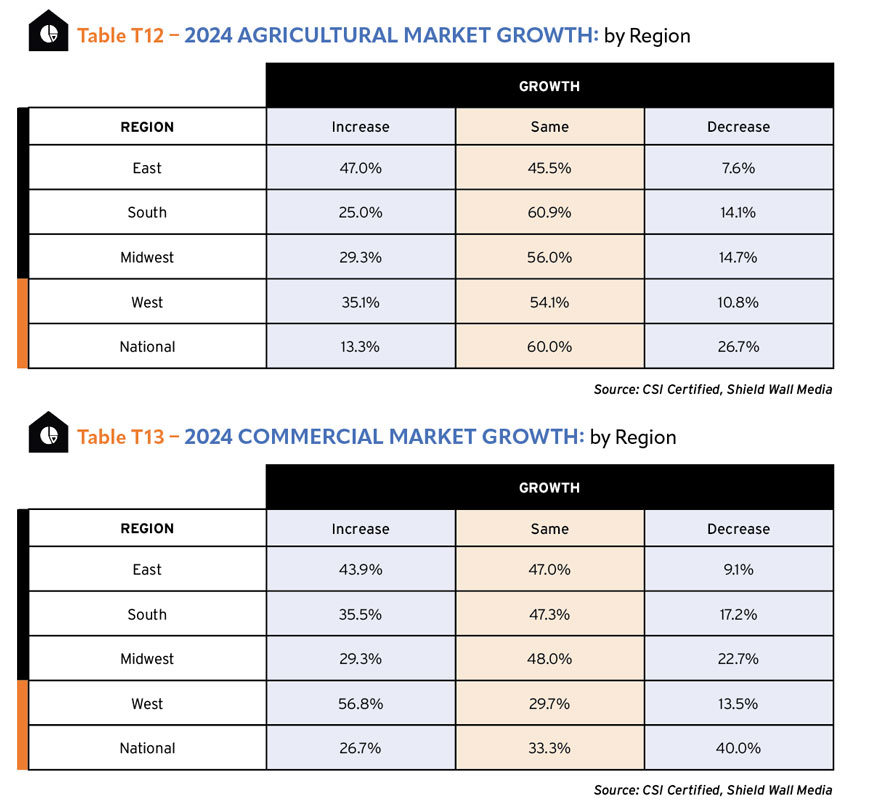

Companies in the East are much more optimistic about the growth of the agricultural market segment than other regions or the national companies. 47% of our respondents from the East anticipate an increase in the agricultural construction segment. Only 13.3% of national companies or companies with locations in more than one region think this segment will grow. T12

The majority of respondents think it will stay the same. On average about 55.3% of surveyed companies expect it to remain the same with only 45.5% of those in the East suggesting this market segment will remain constant.

More than a quarter (26.7%) of national companies see a decline coming in 2024 while the East once again shows its optimism with a mere 7.6% of respondents thinking the agricultural segment will slow this year. Looking at the commercial market segment, the responses from the different regions again vary widely. The only region where more than half of the survey takers think this segment will increase are from the West (56.8%). Approximately the same number of respondents in the East, Midwest, and South think the segment will remain the same. T13

Survey takers representing national companies (40%) are again pessimistic about the prospects for growth in the commercial segment in 2024, while those in the East are the least pessimistic with only 9.1% anticipating a decline.

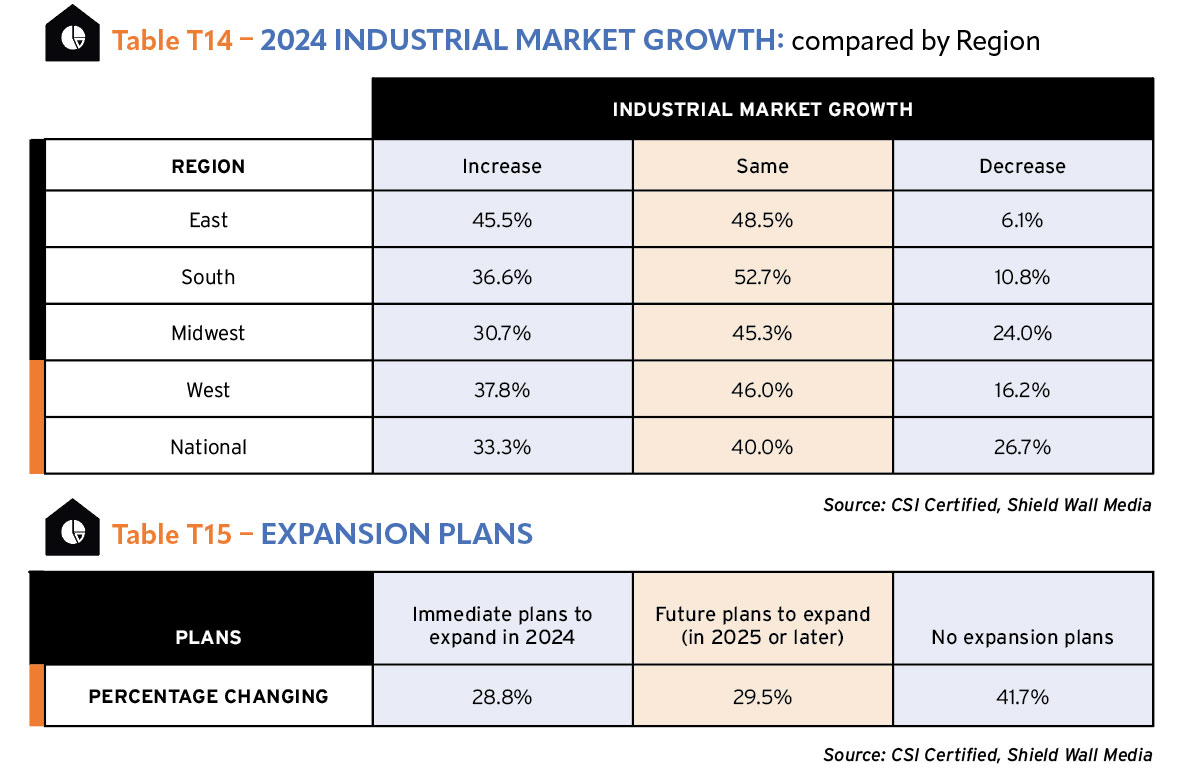

The survey takers from the East again show their optimism with only 6.1% anticipating a slowdown in the industrial market segment. On average, 36.8% of respondents think this market will grow in 2024, but 45.5% of those from East see the possibility of growth. Of those in the Midwest though, only 30.7% believe industrial construction will grow. T14

Midwestern respondents (24%) along with those representing national companies (26.7%) are most likely to see a decline in this market segment.

One of the great ways to determine how optimistic people really are about the future is to ask if they have expansion plans. Nearly 30% of respondents expect to expand in 2024. Considering that only 47.7% of all respondents are anticipating sales growth in 2024, that is a remarkable number and shows a very high confidence in the growth of the industry and their businesses. T15

Looking beyond the immediate future, another 29.5% of respondents have plans to expand and only 41.7% don’t have plans. That doesn’t mean those companies won’t expand; they just don’t have immediate plans.

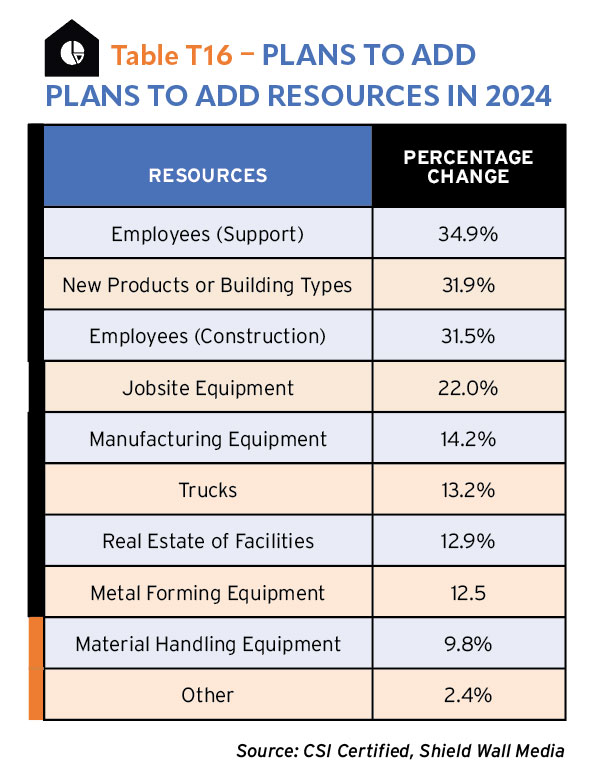

Expansion requires a significant amount of planning as well as investment of capital. But companies can show positivity about the future in other ways, including how they will add resources to their companies. When asked “Which of the following (if any) do you plan to add or increase in 2024,” respondents selected from a variety of options. T16

Adding support employees (34.9%) is the most likely area chosen to increase the size of a company, but when you add construction employees to the list (31.5%) it becomes clear that survey takers are aggressively looking for workers to handle an increase in business.

New business may come through diving into a new building type to offer or new products. The likelihood of adding those products to the mix for our respondents was 31.9%.

On the non-human resources side of the capital equation, respondents also expect to add jobsite equipment (22%), manufacturing equipment (14.2%), trucks (13.2%), real estate or facilities (12.9%), metal forming equipment (12.5%) and material handling equipment (9.8%).

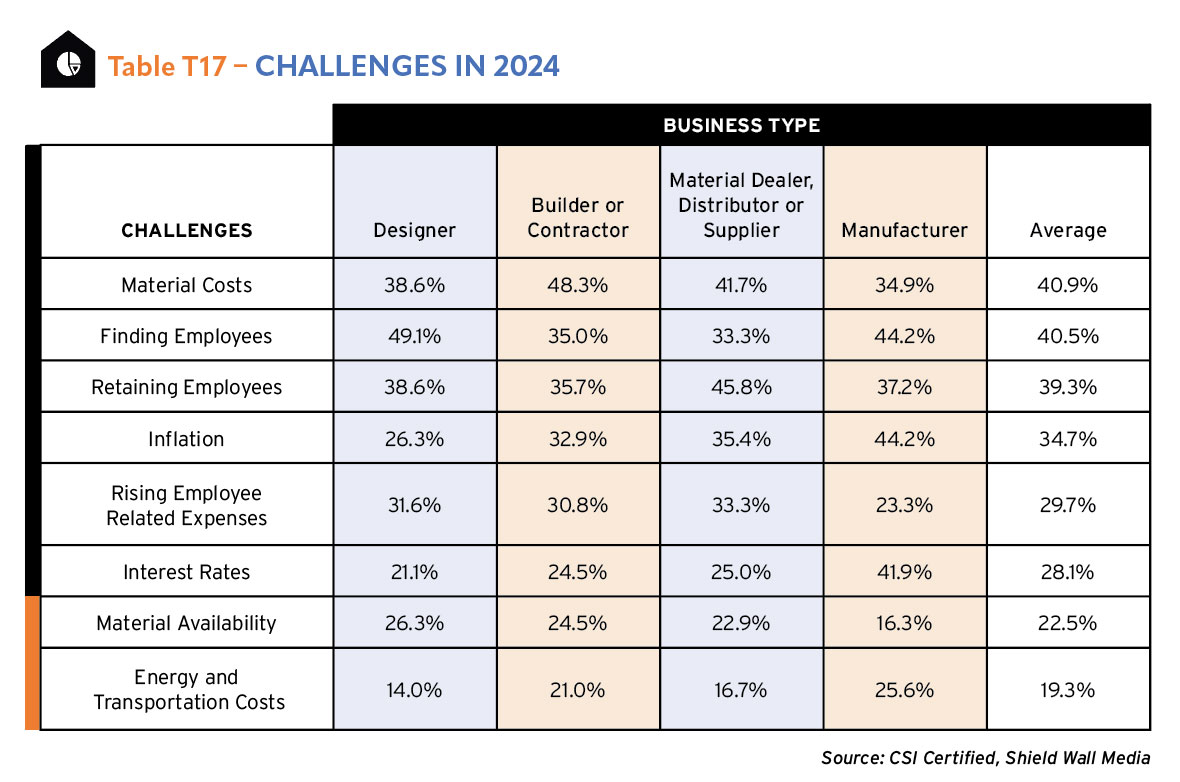

For years, one of the biggest challenges the construction industry faced was securing enough skilled labor, and then came the COVID-19 pandemic. That changed everything. The skilled labor shortage didn’t disappear, but new challenges arose. Supply chain issues caused material shortages and increased lead times. T17

Today, though, according to our survey respondents, the biggest issues facing designers, contractors, distributors, and manufacturers are related to the recovery from the pandemic. On average, 40.9% of our survey takers said controlling cost of materials is the biggest challenge they face. For contractors, that is the leading issue; almost half identified it as the biggest challenge.

Add in inflation (34.7% average), rising employee-related expenses (29.7% average), interest rates (28.1% average), and cost of energy and transportation (19.3% average) and you see that of the eight biggest challenges facing our survey takers, five of them are related to rising costs.

But it’s different for different players in the industry. Designers are much more likely to identify finding employees (49.1%) as their biggest challenge than distributors (33.3%). Distributors see retaining employees (45.8%) as the biggest challenge.

After designers, manufacturers experience the most difficulty finding employees (44.2%) but they don’t rate that much more of a challenge than either inflation (44.2%) or interest rates (41.9%).

While identifying the average is helpful in ranking overall attitudes about challenges, there are significant differences among the companies in the building product supply chain. Understanding those specific challenges will make it easier for companies wanting to engage designers, contractors, distributors, or manufacturers.

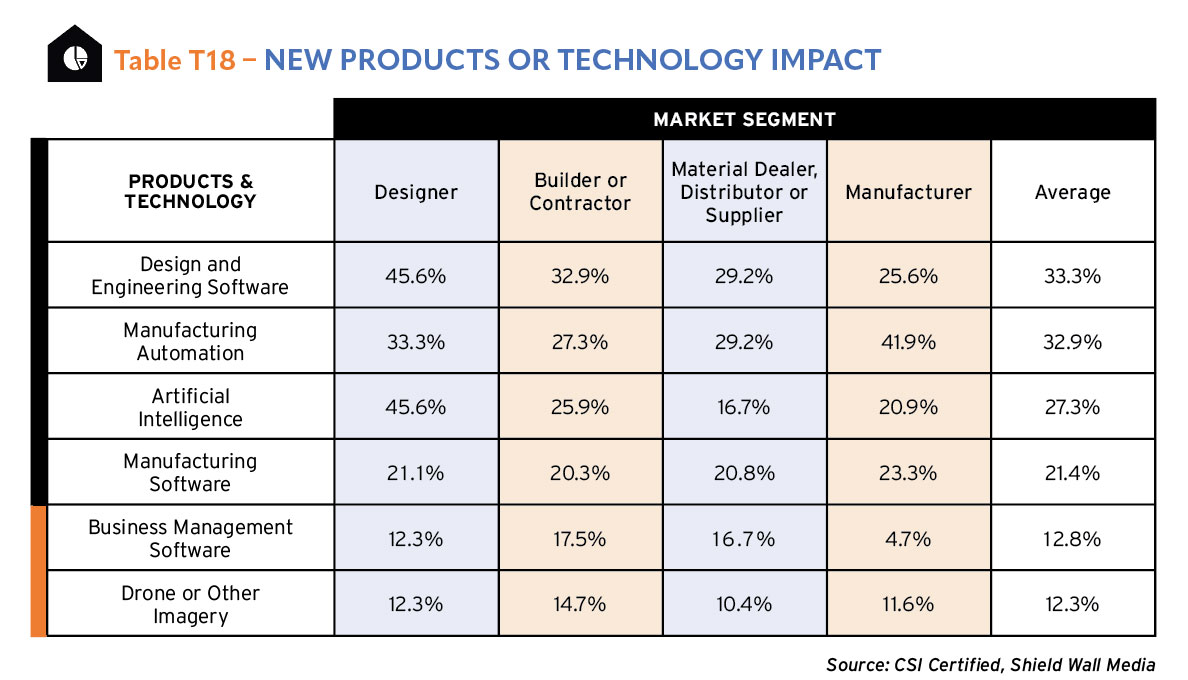

On average, our respondents say design and engineering software will have the greatest impact on their business with a third identifying it as most important. However, the heavy selection of that by designers (45.6%) weights it higher than others. The same is true with artificial intelligence (AI) which 45.6% of designers identify as having a heavy impact on their businesses, but no other cohort – contractor, distributor, or manufacturer – rates it higher than 26%.T18

Understandably, manufacturers (41.9%) think manufacturing automation will have the biggest impact on their businesses, but surprisingly high percentages of the other cohorts in the survey also understand innovation in this area will significantly impact their businesses.

(AI is the topic of the day ever since ChatGPT launched in November 2022. It is already being used in design software, so the high ranking (45.6%) for that new technology is not surprising from designers. Only 16.7% of distributors see AI as having an impact.

Both manufacturing software and drone imagery technology ranked relatively evenly among all the participants in the construction process. The only other significant outlier is the low rating of business management and sales software among manufacturers. A mere 4.7% see that technology as having an impact. That would likely be because those companies have already invested heavily in that technology.

Check out the whole Construction Survey Annual & Market Data 2024!