GARAGE, SHED AND CARPORT CONSTRUCTION DATA

By Paul Deffenbaugh, Contributing Editor

There is at the end of every supply chain in the construction industry a consumer, but in the garage, shed, and carport sector of the industry, the distance between the top of the chain and the bottom is condensed. Because of that, the issues facing companies engaged in this sector are different than those in other sectors. Although financing is obviously part of almost every construction project, in this sector financing greases the wheels and helps sell the product. A lot has changed in the industry and much of that is in the details.

The garage, shed, and carport construction industry is primarily a straight to consumer business that relies heavily on a direct sales business model supported by consumer financing. In many ways, it’s similar to the specialty remodeler industry that provides retrofit roofing, siding, and windows, but with a more heavily involved manufacturer component.

Characteristics of the Shed and Carport Industry

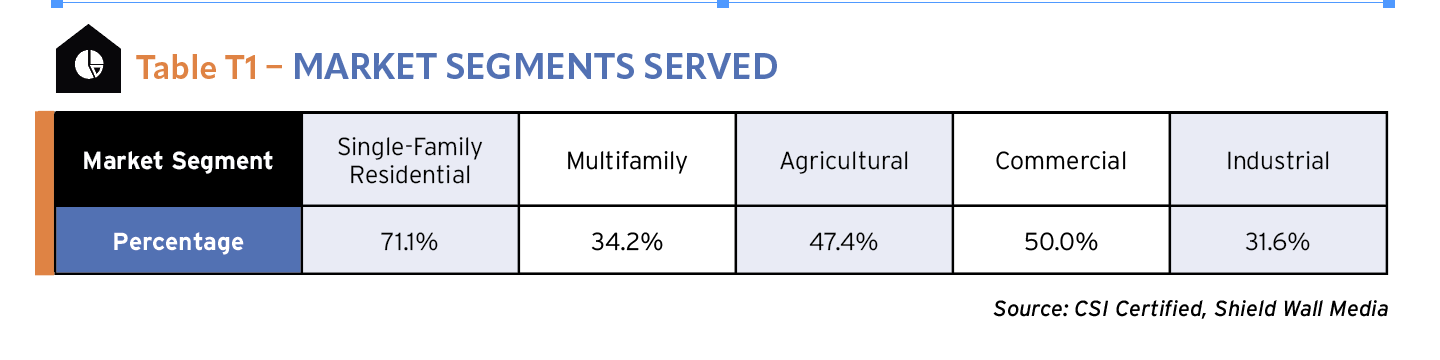

The respondents to the Construction Survey Insights (CSI) survey who are engaged in garage, shed, and carport construction work primarily in the single-family residential market segment with 71.1% of them indicating that. The next closest market segment was commercial (50%) and that was about equal to the 47.4% who identified the agricultural market segment as an area they serve. A surprising number work in multifamily (34.2%), although when we looked at companies whose identified business was garage, shed, and carport as their primary business, two thirds of them served single-family residential. T1

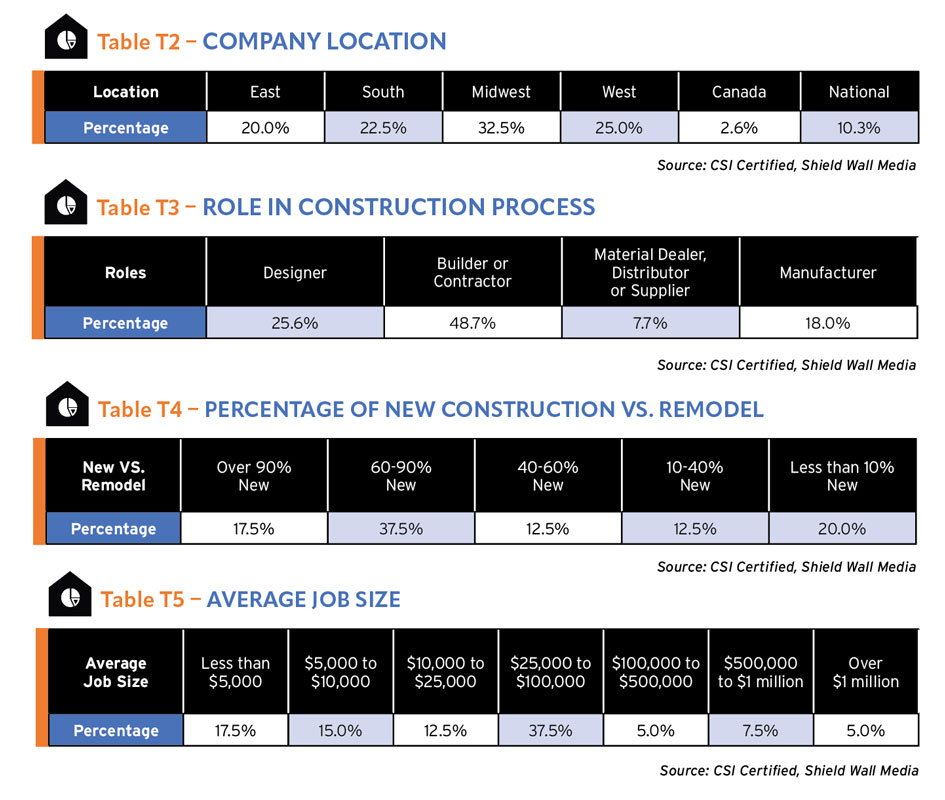

Our general sense of companies engaged in garage, shed, and carport construction is they tend to be more rural and more often based in the South or the Midwest. That is partially shown in the results from our survey takers, of whom about a third (32.5%) say they are in the Midwest, a quarter from the West, and 22.5% from the South. The East is not a strong market for companies engaged in garage, shed, and carport construction, and only 20% of our respondents report their companies were from that region. T2

Most of the survey respondents in the CSI data who are engaged in garage, shed, and carport construction are contractors (48.7%). There is a blending of roles in this construction sector, though, and designers could work for a contractor, distributor, or manufacturer. And, since there has been considerable consolidation of the supply chain, a company could fill all of these roles. Design the structure, make, it, distribute it, then sell and install it. All under one roof. T3

About a quarter of our respondents (25.6%) were designers, and 18% were manufacturers. Only 7.7% of our respondents engaged in garage, shed, and carport construction identified as distributors, which is the step in the supply chain that is most likely to have been consolidated in this market sector.

More than half (55%) of survey takers engaged in garage, shed, and carport construction say at least 60% of their business is new construction and 17.5% report at least 90% is new. These kinds of buildings get little remodel work done on them to speak of other than maintenance and repair, so the high percentage of respondents reporting their business is primarily new construction is not a surprise. T4

But these businesses may be involved in other aspects of construction to some extent, and it’s there that they are more likely to do remodeling. Or a garage, shed, or carport was, perhaps, part of a remodeling project. To that end, only 20% say less than 10% of their work is new, and a quarter report that between 10% and 60% is new.

The average job size for companies engaged in garage, shed, and carport construction is overwhelmingly on the small side. 45% of them report an average job size of less than $25,000 and 37.5% indicate their average job size was between $25,000 and $100,000. The range between 25,000 and 100,000 is quite large, and it would be possible for a significant percentage of respondents to have an average job size at the lower end of that range. The percentages above $100,000 would seem to indicate that the percentages at the top of the $25,000 to $100,000 may be thinning considerably. The 12.5% who say they have an average job size of greater than $500,000 may be doing additional work, or their sale of a garage, shed, or carport may be part of a larger project. T5

Projected Industry Growth

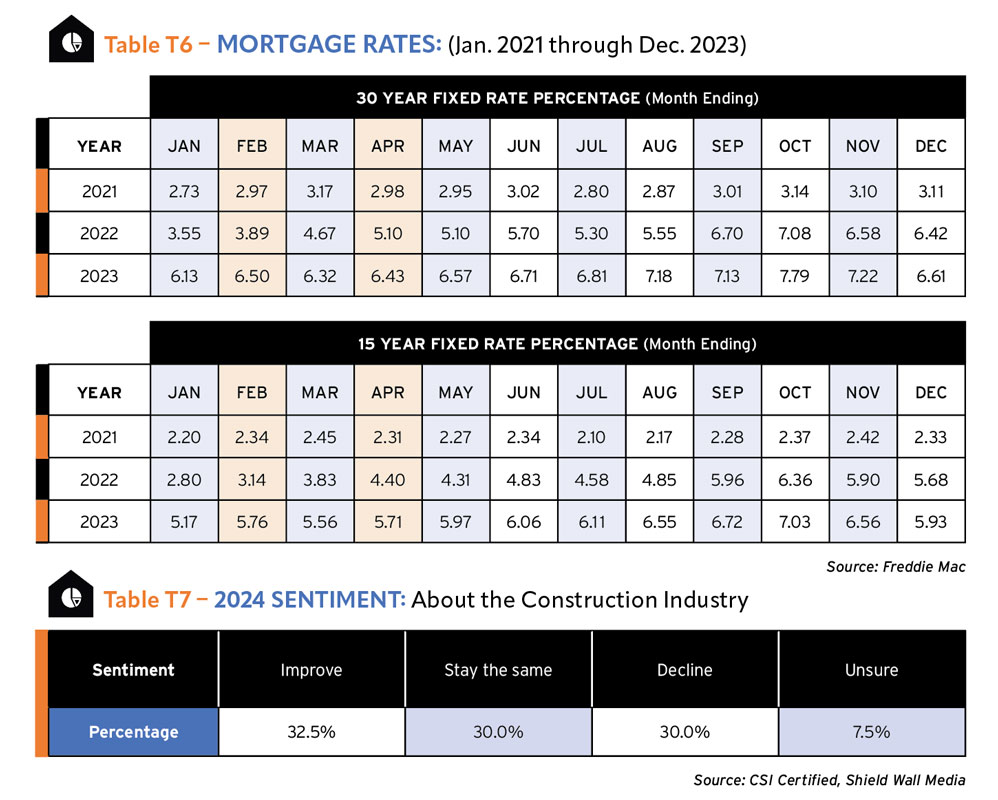

Financing is tightly intertwined with selling garages, sheds, and carports. Homeowners often finance through the company making the sale, borrow against the equity in their house, or take out a line of equity loan (HELOC). As 30-year and 15-year fixed mortgage rates have risen since their low in Jan. 2021, the cost of financing has increased. A 30-year fixed mortgage rate has gone from 2.65% in Jan. 2021 to a peak of 7.79% in Oct. 2023, which is more than doubling the cost of borrowing related to home improvement. T6

While hopes for 2024 were initially promising, the latest meeting of the Federal Reserve in March 2024, put a bit of a damper on that. Policymakers had hoped to see a decline in the target interest rate but the Fed is waiting to see inflation get closer to its goal of 2%.

Following the meeting, Fannie Mae announced its earlier prediction of the 30-year fixed rate dropping to 5.9% by the end of 2024 was being revised. The organization now believes 2024 will end with a rate of 6.4%. The Fed continues to signal rate cuts are coming, but until that actually happens the cost of borrowing money will remain higher than it has been in 23 years. And the garage, shed, and carport market will need to overcome those price objections.

The concern about the cost of money could also explain why the general sentiment toward the construction industry among companies engaged in garage, shed, and carport construction is not very positive. About a third believe the industry will improve in 2024, while 30% think it will stay the same and 30% also think it will decline. The percentage who are unsure about what will happen probably speaks to the uncertainty about the economy. In spite of relatively high consumer sentiment, strong employment, and overall growth, the worries about inflation and rising costs are seeping into all of the conversations in the construction industry. This can be seen clearly in the “Challenges” part of this section below. T7

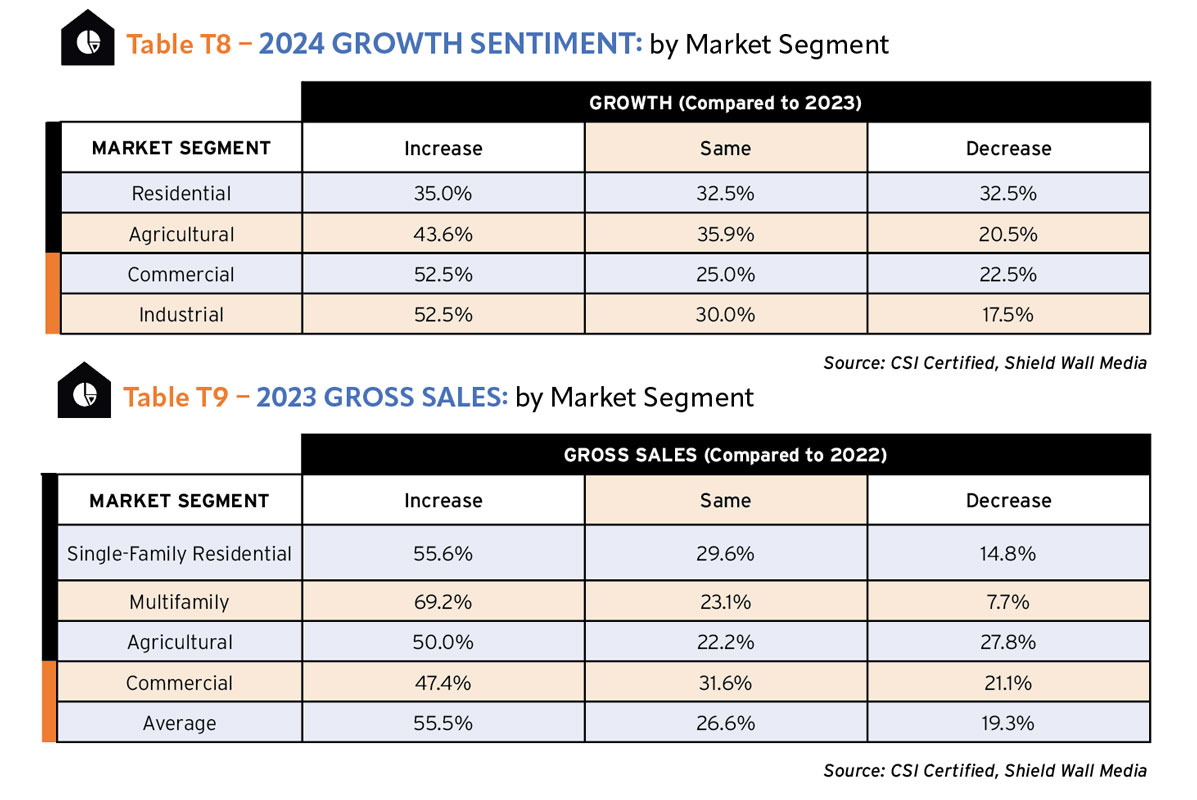

When looking at what companies engaged in garage, shed, and carport construction think will happen to individual market segments in 2024, there are clear winners. 52.5% of our respondents in this sector think the industrial market segment will see an increase in activity in 2024. There are not a lot of companies in this part of the survey who are working in the industrial segment, so this may be a case of the grass looks greener on the other side of the fence effect. T8

The same could be said about the commercial market segment, where 52.5% of survey takers believe it will increase in activity in 2024. Again this sector of the industry is less focused on commercial construction so those sentiments may be taken with a grain of sand.

Garage, shed, and carport companies are, though, heavily involved in the single-family residential market, and it is there that they see less activity. The National Association of Home Builder (NAHB) has forecast that single-family starts will increase 4.6% in 2024, which is after a decline of 8.6% in 2023. That was the prevailing view when this survey was taken, and our respondents in the garage, shed, and carport industry were far less optimistic than that forecast suggest they should be. Only 35% of survey takers expected an increase in this market segment, while a third expected a decline.

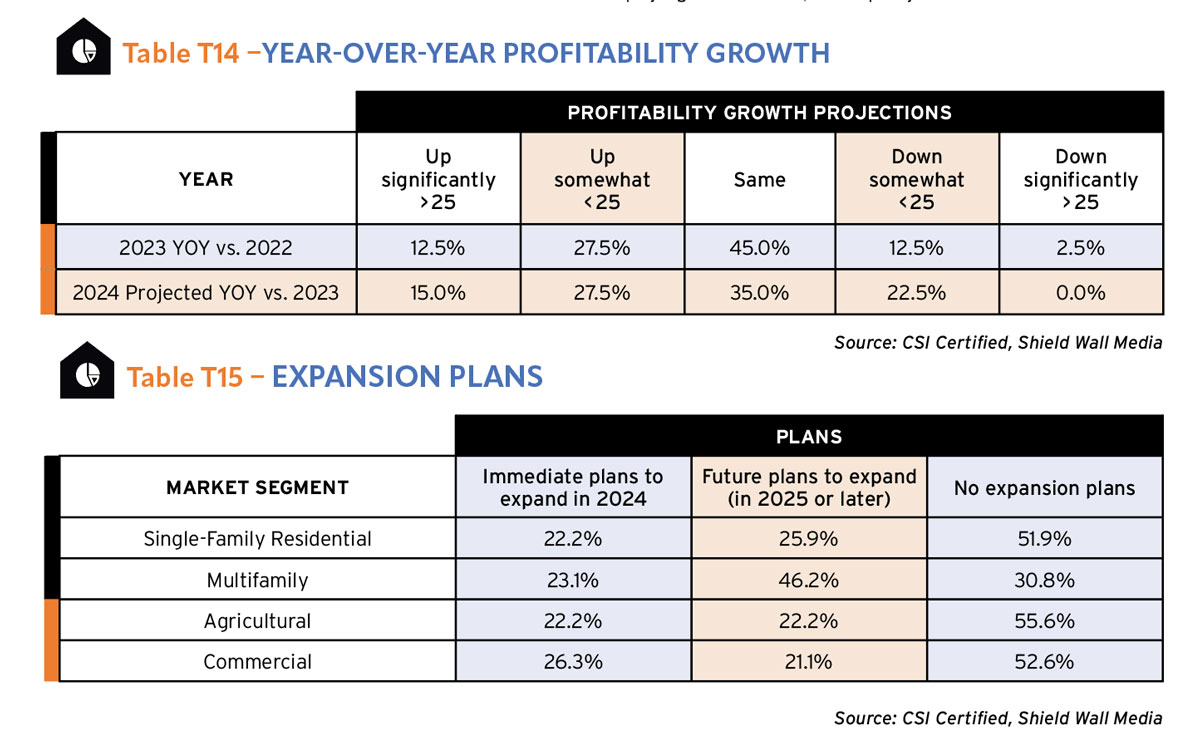

Among companies engaged in garage, shed, and carport construction, there are some market segments that performed better in 2023 than they did in 2022. In other sections of this report, we have divided the growth into five categories (up significantly, up somewhat, stayed the same, etc.) but responses to this sector only allowed us to characterize these movements as up, same, or down. T9

In keeping with other sections, the multifamily market is the area where companies engaged in garage, shed, and carport construction were the most likely to see an increase in activity in 2023 compared to 2022 with 69.2% reporting a jump in work in that market segment. Averaging across all segments, the percentage of companies reporting an increase was 55.5%, so the 55.6% percent of companies reporting an increase in the single-family market segment was right about the average.

Again, keeping with the sentiment across this CSI data, the companies serving the agricultural segment were most likely to see a decline in gross sales in 2023, with 27.8% reporting as such, but half of the companies serving this market segment also saw an increase.

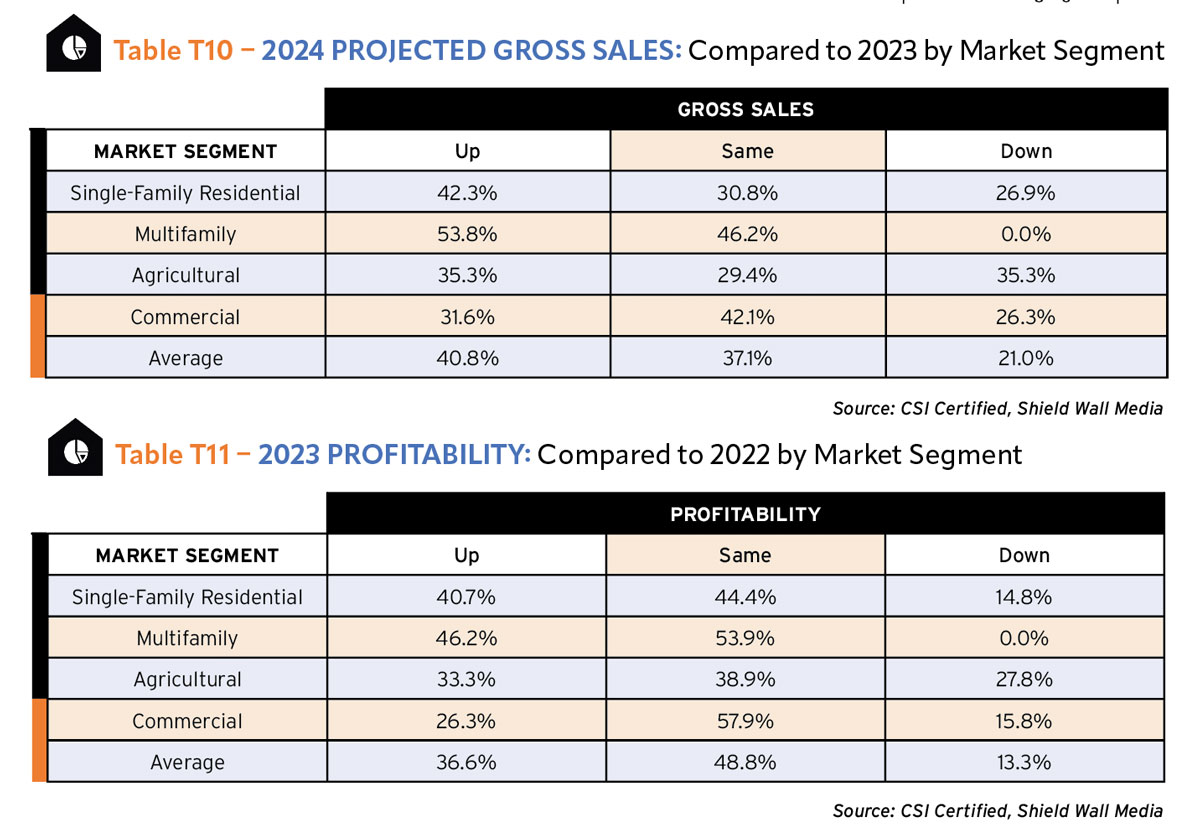

Projecting gross sales in 2024 compared to 2023, companies serving the multifamily market again were the most optimistic with 53.8% expecting an increase in gross sales and none anticipating a decline. The companies engaged in garage, shed, and carport construction in the agricultural market were the most pessimistic, with 35.3% anticipating a decline, which was equal to the percentage who expect an increase in gross sales in 2024. T10

Looking at the average likelihood of decline across the market segments, it’s apparent that the companies serving multifamily and agricultural are tugging the average in opposite directions, while single-family (26.9%) and commercial (26.3%) hold almost the same likelihood of decline in those segments.

Companies engaged in this sector are less likely to see gross sales increases in the single-family market segment (42.3%) but much more likely to anticipate growth than those in agricultural (35.3%) or commercial (316%).

When addressing profitability among companies engaged in garage, shed, and carport construction, those serving the multifamily market were not nearly as likely to report increases as they did gross sales increases. Again, it sounds like a story often repeated, but across the board, we are seeing companies getting more sales but struggling to hold the line on profitability in light of rising costs. The good news here is that companies in this segment were largely able to hold their profitability the same in 2023 as 2022 with about half (48.8%) on average saying profits had remained steady. T11

The respondents serving the agricultural market segment were least likely to say profitability held steady (38.9%) and most likely to say profits declined in 2023 year over year (27.8%). The residential market was the segment where companies were most likely to report increases in profitability with 40.7% of companies serving the single-family market saying profits increased last year, and 46.2% of companies serving the multifamily market saying they will increase year over year.

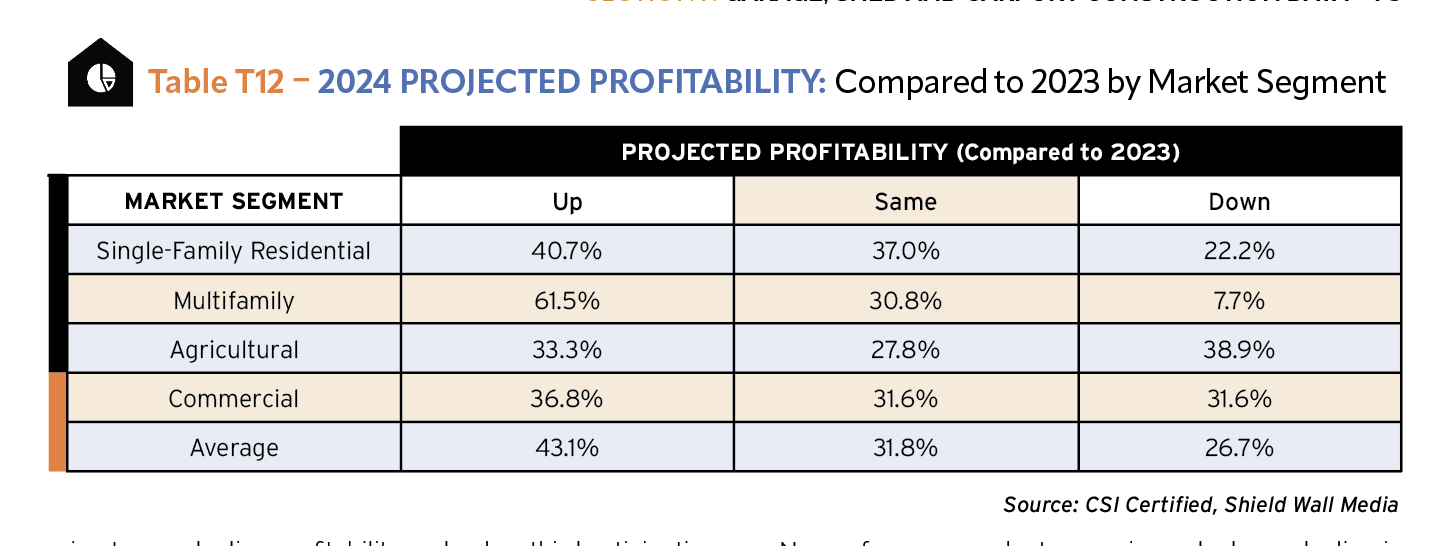

You have to give it to those companies serving the multifamily market and their wild optimism. 61.5% of companies engaged in garage, shed, and carport construction who serve this market segment anticipate profits will increase in 2024 compared to 2023. And only 7.7% expect profitability to decline. T12

The companies serving the other market segments don’t come anywhere near as close to being that optimistic. In fact, compared to other sectors of this report, these respondents were far less likely to believe they could hold the line on profitability in 2024. Those serving the agricultural market were the least optimistic with 38.9% expecting to see decline profitability and only a third anticipating an increase.

The single-family residential market companies, in spite of seeing the 4.8% rise in housing starts NAHB has predicted, are only likely to anticipate a rise in profitability (40.7%) in 2024 that’s equal to what they experienced in 2023. More than half the companies serving the commercial market kept profitability the same in 2023 as 2022 (57.9%) but only 31.6% of them project keeping profits the same in 2024 as 2023. 15.8% of these suffered a decline in profits in 2023, but 31.6% expect to see profits decline in 2024. T11 & T12

Company Size and Growth Projections

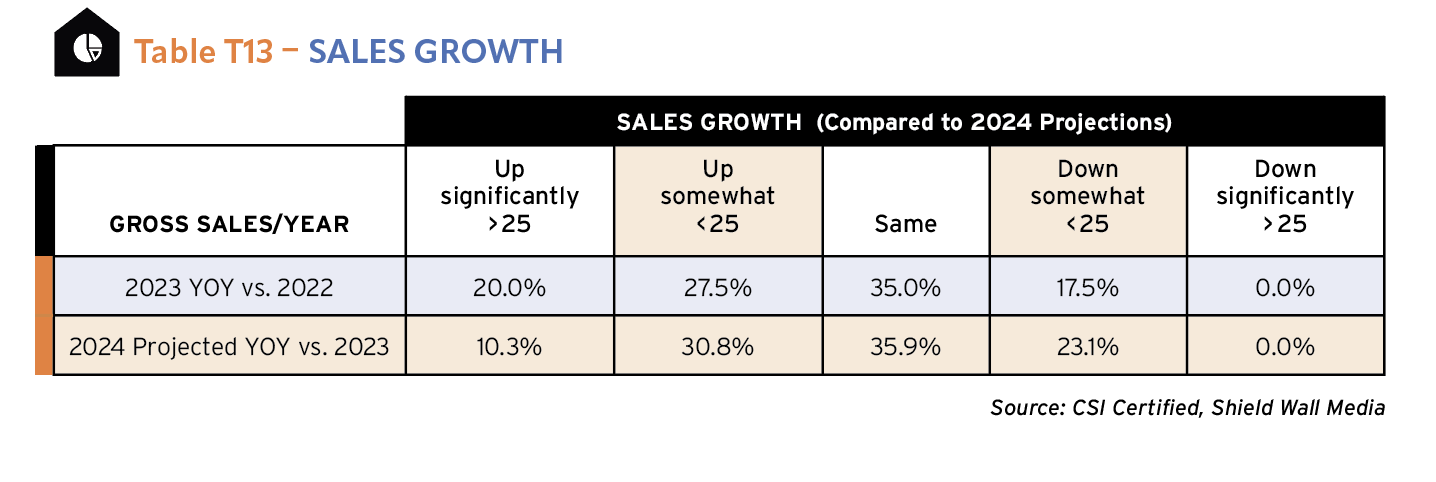

Companies engaged in garage, shed, and carport construction generally experienced a good sales year in 2023 in spite of the increasing cost of money. Those reporting increases in gross sales last year were about half (47.5%) of the respondents, with 20% of them saying sales were up more than 25%. About a third (35%) say sales will be even year over year, and 17.5% experienced a decline, although none of the survey takers say sales dropped more than 25%. T13

As has been shown earlier, this group – companies engaged in garage, shed, and carport construction – are not as positive about 2024 prospects as others. A still decent percentage (41.1%) say sales will increase this year, but only 10.3% anticipate a significant increase. About the same percentage expect sales to remain constant in 2024 as those who experience steady sales in 2023. But a much larger percentage (23.1%) see a decline in sales coming down the road this year.

None of our respondents experienced a large decline in 2023, and none expect a greater than 25% decline in sales in 2024.

The profit story for this side of the industry is a different matter than sales. Of companies engaged in garage, shed, and carport construction, 40% report an increase in profits in 2023 compared to 47.5% who said sales were up. When you compare significant increases, only 12.5% report profits jumped more than 25% in 2023, but 20% say sales jumped more than 25%. Clearly, issues with controlling costs in light of inflation and other pressures hurt profitability in 2023. This is especially evident among the 2.5% of respondents who say they had profits decline more than 25% in 2023. None, as was said earlier, had a similar sales decline. T13 & T14

Looking to 2024, the connection between sales and profits seems to have aligned. 35% of our respondents working in the garage, shed, and carport construction sector expect 2024 profits to hold the same, which closely matches the number who expect sales to hold the same. Where 41.1% expect sales to increase in 2024, a nearly identical percentage of 42.5% expect profits to increase. But a far greater percentage (15%) expect profits to increase significantly compared to the 10.3% who anticipate a greater than 25% jump in sales.

On the other end of the spectrum, 22.5% of our survey takers think profits will decline in 2024, which is a larger percentage than those who experienced a decline in 2023 (15%). It does, though, roughly match the percentage who expect a decline in sales (23.1%). None expect a significant decline in profits.

Future Opportunities and Challenges

Companies doing garage, shed, and carport construction are, on the whole, less likely to have expansion plans than companies in other sectors of the industry, such as metal roofing or post-frame construction. This is regardless of the market segment they serve with the exception of the growth-oriented respondents in the multifamily market where only 30.8% of companies have no plans to expand. For the other segments – single-family, agricultural, and commercial – more than half of survey-takers say they have no plans to expand. T15

There is a consistent response among all four segments when looking at plans to expand in 2024. Between 22% and 26% of companies by segment have immediate plans for expansion. The biggest difference among the market segments is that companies in multifamily are more likely to want to expand in the future (46.2%) and less likely (30.8%) to have no plans to expand.

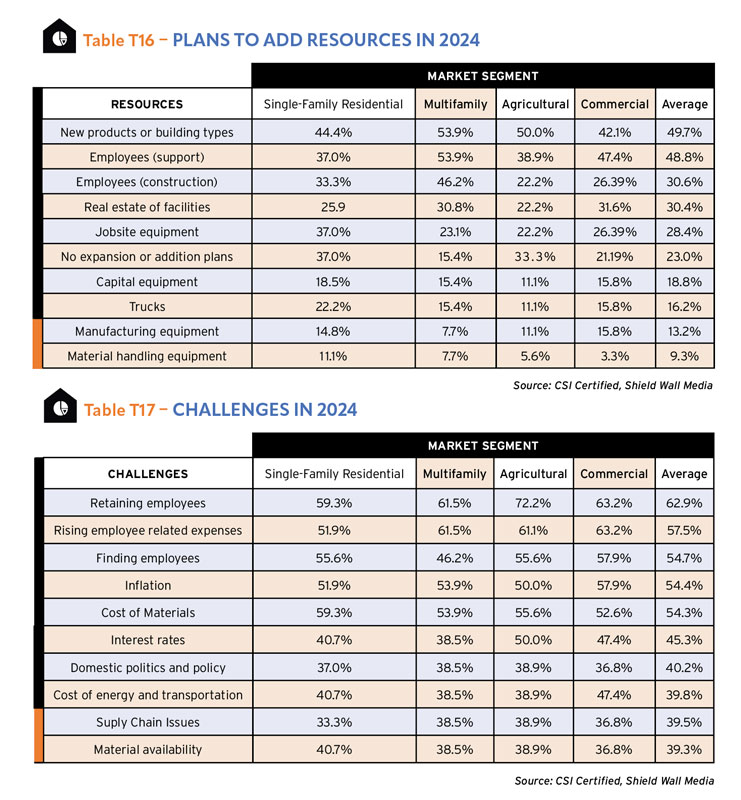

On average, about half of the companies engaged in garage, shed, and carport construction mentioned a need to add new products or building types (49.7%) and support employees (48.8%) when asked about future resource needs. Adding new products is more likely among companies serving the multifamily market (53.5%) than it is among companies in the commercial market (42.1%). Multifamily companies are also more likely to address shortages in field employees (46.2%) than the other market segments. T16

There has been consistency from sector to sector in the responses by market segment. New products has been the resource companies are most likely to add, and adding support employees is often the second most likely resource to be identified.

In keeping with the trend, the demand for skilled labor is not the top needed resource among companies engaged in garage, shed, and carport construction. Carlson of A.J. Manufacturing digs into this issue a little deeper. “The current situation as it relates to work ethic, aspiration to improve, or achieve personal goals, in general, is of concern,” he says. “Many individuals simply do not have the skills, fundamental understanding, or examples to learn from to be employees that contribute regularly while consistently improving. Many employees are good but are fewer and more difficult to find than ever.”

Making an appearance on this list at a higher level than in other sectors is the option not to add any resources. About a quarter (23%) on average said they didn’t plan to add resources, and among companies serving the single-family market that was 37%.

While companies engaged in garage, shed, and carport construction don’t have plans to add employees at the rate of companies in other sectors, they do see employee-related issues as the three largest challenges they face. On average, 62.9% of companies in this sector say retaining employees is the biggest challenge, while 57.5% say controlling rising employee costs is a challenge, and 54.7% say finding employees is a challenge. Those three challenges are interrelated. Rising employee costs have to do with increasing wage demands as wages in the economy rise and other industries can now compete with construction. If a barista can make $20 per hour with benefits, paying a laborer $40,000 per year with limited benefits is tough competition. So, keeping employees is the most important element of human resources. Finding employees when unemployment is at record lows is also a daunting challenge. T17

Not only are those three challenges connected, they are all influenced by the other challenges companies engaged in garage, shed, and carport construction face. Inflation well above the Fed-targeted 2%, rising costs of materials, and interest rates going up impact a company’s ability to plan and manage. Interest rates affect both a company’s ability to borrow money for capital expansion or establish a line of credit, while making it more difficult for consumers to finance the products the company sells. Supply chain issues and material availability continue to be challenges that haunt the construction industry with roughly 39% of companies in this sector citing those as challenges.

Check out the whole Construction Survey Annual & Market Data 2024!