The post-frame construction market is primarily centered in rural America, which also means that companies engaged in post-frame construction are also likely taking on other building types. Rural builders need to be flexible. That kind of flexibility is matched by the design flexibility of the buildings.

Characteristics of the Post Frame Industry

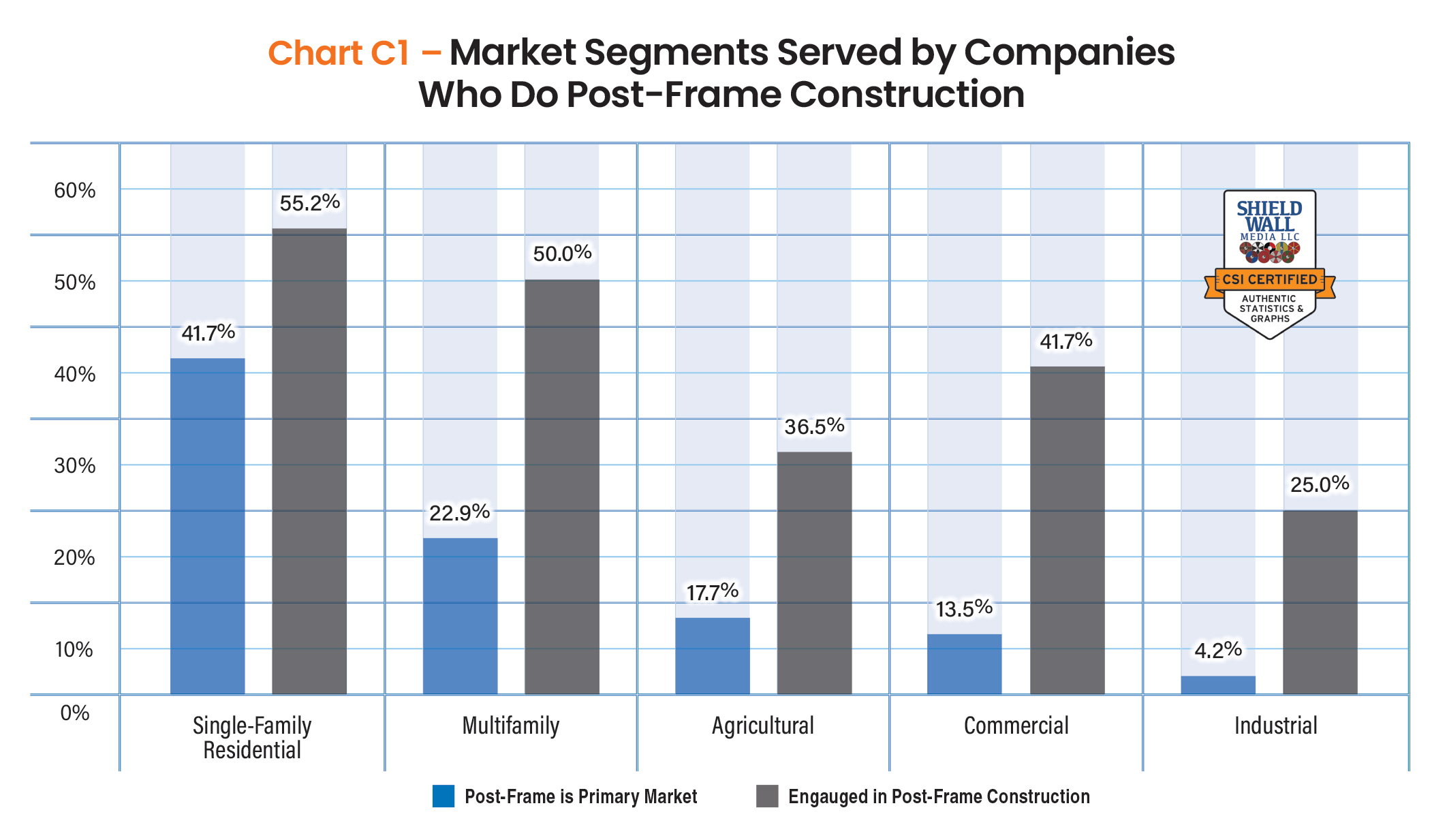

While post-frame buildings are used extensively in the agricultural market, the companies in our survey who report their primary building type was post-frame are more likely to be involved in single-family residential work (41.7%). The rise of the popularity of barndomiums is likely driving that move, but 17.7% of the respondents also said they were involved in agricultural construction.

When we broaden the scope and look at companies who report they are engaged in post-frame construction, which would include those who have it as their primary building type, the survey-takers still report they are most likely to be involved in single-family residential (55.2%). Surprising, 50% of those respondents also report that they are involved in multifamily work, which probably speaks again to the flexibility companies doing rural construction need to exhibit.

Respondents to the CSI annual survey who were engaged in building post-frame buildings were more likely to be based in the Midwest (32.3%) or South (27.1%) than the other U.S. regions. We did have a few companies that worked nationally, though, they were probably manufacturers, not contractors or designers. And we did have one respondent of the 96 who said they were engaged in post-frame buildings in Canada.

Most of the companies who responded to the survey and were engaged in post-frame construction were contractors (54.2%), which is a 20% increase of the percentage of contractors who participated in this survey last year (45.1%).

Just over a fifth of survey takers were designers (21.9%) and that was still less than half the total of survey takers. Distributors represented 26.8% of respondents while designers clocked in at 19.7% of all respondents. The smallest faction represented were manufacturers with only 8.5% of respondents.

More than half (54.2%) of the companies engaged in post-frame construction say at least 60% of their work is in new construction, with only 11.5% reporting less than 40% of the work is new. Of the survey takers, 22.9% said almost all their work was new construction. Approximately, a third (34.4%) reported they did between 40% and 60% new work.

We compared the average job size of companies engaged in post-frame buildings reported in last year’s survey to this year’s. An almost identical percentage said their average job size was less than $25,000. In 2024, 49.3% reported that, and this year 51.0% reported it. But there was within that average size a very large shift to larger jobs. Companies that reported their average job size was between $10,000 and $25,000 in 2023 were 19.2% of responders, but the companies in this year’s survey reporting their job size for 2024 in the same grouping totaled 31.3% of the respondents.

A job less than $5,000 is a small handyman or remodeling project, but a project less than $25,000 is a mid-sized remodeling project, such as a reroofing. About a quarter of the survey takers in both years report average job sizes greater than $100,000.

Because of the lower participation in the survey last year, we saw considerable volatility when we analyzed participation by region or market segment. Of particular note, the East region was particularly unstable. This year, we had 93 companies reporting they were engaged in post-frame construction, which is nearly double the participation from last year.

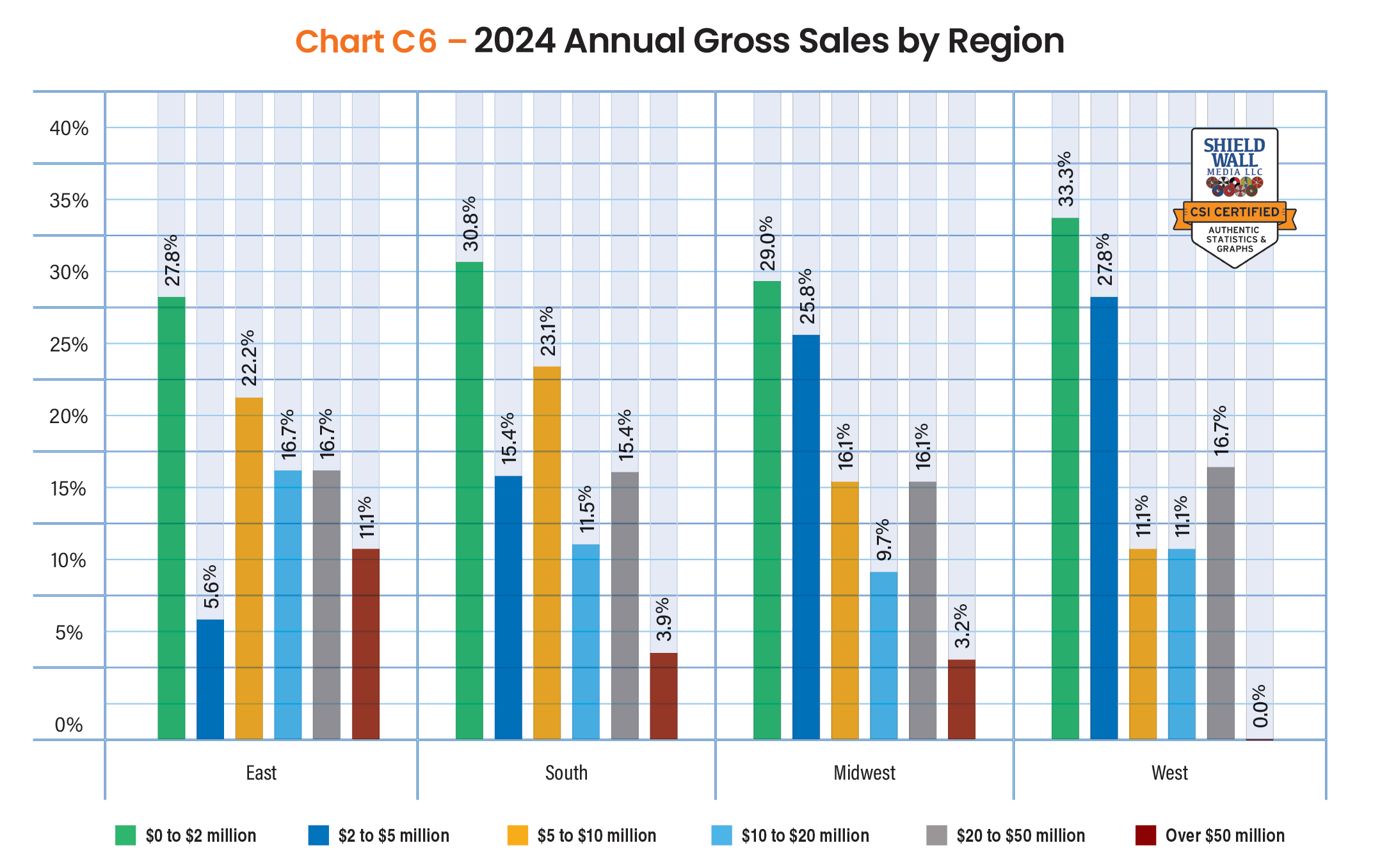

Respondents in the East (27.8%) were as likely to report revenues below $2 million as companies in the other regions. But only (55.6%) of companies in the East doing post-frame construction reporting gross sales in 2024 below $10 million, which was much lower than the other regions, where about 70% reported revenues less than $10 million.

Ben Nystrom, CEO of MWI Components, Spencer, Iowa, says “Last year was a strange year. The typically busy months were slower than expected. I’m usually fairly optimistic about our industry. We are still experiencing a COVID correction from the first half of the 2020s. I hope we find balance in 2025.”

Mark Stover, president, Perma-Column, Ossian, Ind., supports Nystrom’s analysis of 2024. “The pace of business activity started to slow,” he says, “and has become more normalized seasonality since post-COVID.”

The Eastern region’s propensity to have lower gross sales in 2024 can likely be attributed to the participation of very large companies. 11.1% of companies in that region said 2024 gross sales were greater than $50 million. No other region came close to that percent, and companies in the West had no respondents reporting revenues that large.

Projected Industry Growth

In our survey last year, 31.5% of companies engaged in post-frame construction expected the construction industry as a whole to improve in 2024, and 37% thought it would stay the same. Almost 30% (28.8%) anticipated a decline in 2024.

This year, the attitudes are more optimistic even though there seems to be cause of concern. Compared to last year’s 31.5% expectation of improvement, 46.8% of respondents in this year’s survey anticipated 2025 to be a better year. Only 14.9% thought the general business climate in the construction industry would decline.

The positivism is leavened by the comments of people on the front lines. Mark Rhine, a regional sales manager for Leland Industries and based in Oklahoma says, “I’m neutral about the 2025 construction economy. I’m not sure how potential tariffs may affect the business climate.”

We also asked survey takers to express their sentiment about 2025 for the different market segments, and there were some interesting differences. Among companies engaged in post-frame construction, there was a consistency in whether they thought any given market segment would decline. Only 9.5% though the residential market would drop in 2025, 7.4% felt the same about agricultural market, 11.6% about commercial and 9.5% about industrial.

However there were significant differences on whether they expected those market segments to improve or stay the same. Far and away, the largest percentage of survey takers (52.6%) thought the residential market would improve. They were less optimistic about the other three segments with agricultural sentiment about improving being the lowest (37.9%).

In 2024, there were noticeable differences in gross sales growth compared to 2023 by region. More than 60% (61.1%) of companies in the East that were engaged in post-frame construction reported their gross sales increased in 2024 year over year, while only a third of the countries in the West saw growth.

The nature of the growth changed significantly from region to region as well. Companies in the South were far more likely (30.8%) to report growth greater than close up while only 6.5% of companies in the Midwest experienced similar growth.

Less than a fifth of any region reported a decline in gross sales in 2024. Extrapolating from that you can see that respondents were more likely to report growth or flat gross sales than a decline in gross sales.

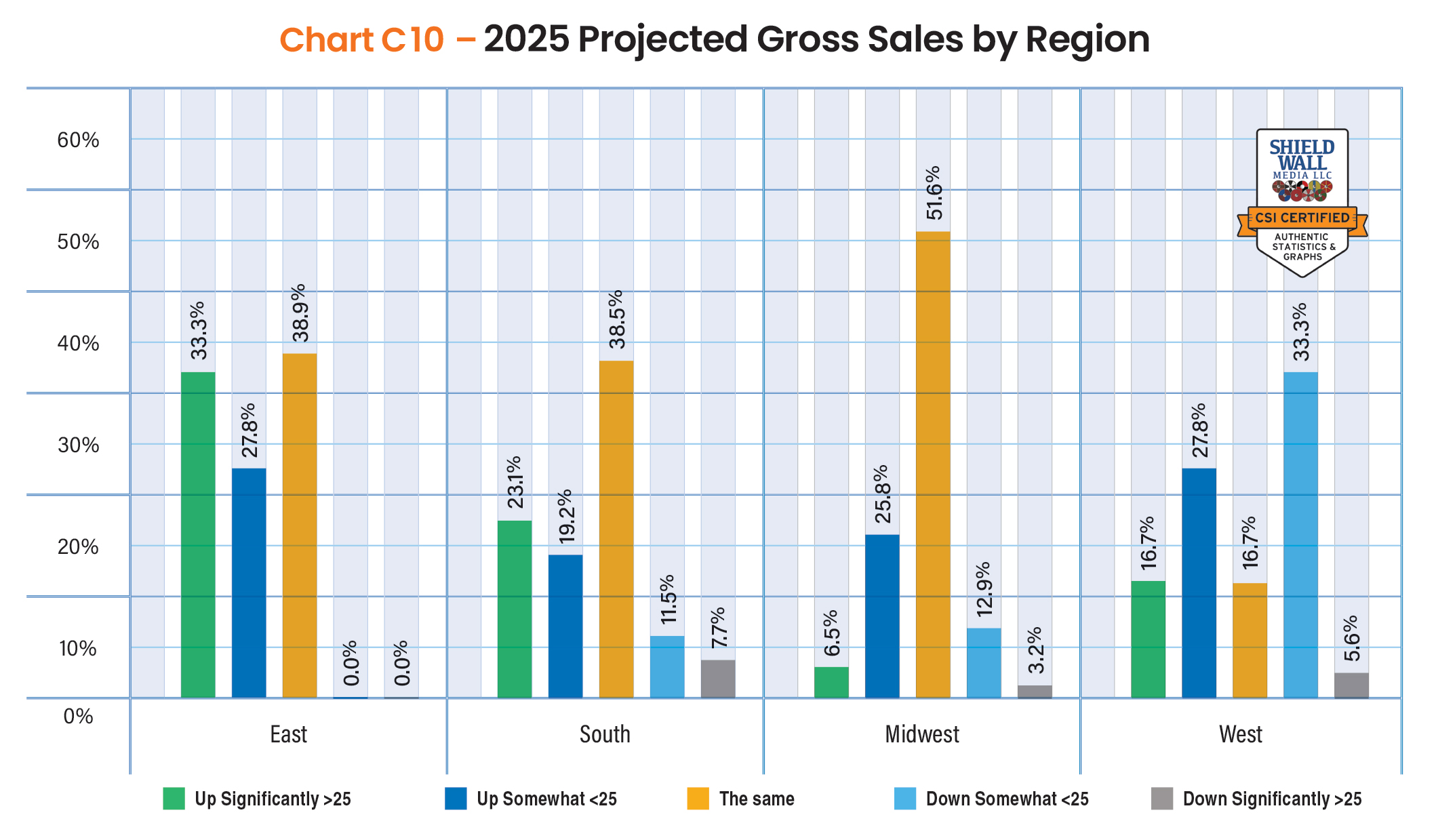

A third of companies engaged in post-frame construction in the East anticipated significant growth (greater than 25%) in 2025. Combined with the 27.8% who thought gross sales would increase somewhat, it’s clear that companies in the East are far more robust about sales than the other regions.

Survey takers in the Midwest were not as likely to expect to see growth in 2025, with only 32.3% of them feeling optimistic. However, they were not necessarily pessimistic, since more than half (51.6%) felt gross sales year over year would be flat.

Companies based in the West were the most pessimistic, with 38.9% expecting a decline in gross sales, which is about double the next closest region (the South at 19.2%) to that sentiment.

Company Size and Growth Projections

In 2024, the likelihood of companies engaged in post-frame construction saying gross sales increased in 2024 was about the same regardless of market segment. Those doing single-family residential work were slightly more likely to report an increase (66.0%) compared to the other segments, which all hovered around 50%. But the reporting on the single-family residential market was primarily driven by survey takers who said gross sales increased only somewhat.

Respondents working in the agricultural (31.4%) and commercial (30.0%) markets were more likely to report significant, or greater than 25%, growth in 2024 compared to 2023. About a fifth of the commercial and industrial companies also reported a decline in gross sales.

Among companies working in the post-frame building industry, the prospects for 2025 were remarkably similar no matter what market segment they worked in. About half of all the respondents, regardless of the market segment, anticipated some kind of growth in gross sales in 2025 with the likelihood ranging from 45 to 55%.

The only differences between segments depended on whether the survey taker thought the increase would be significant (greater than 25%) or just somewhat. Among companies in the single-family residential market, only a fifth (20.8%) thought growth would be significant. Only multifamily (18.8%) respondents reported less likelihood of significant growth.

When looking at the potential for decline in gross sales across market segments, the story is slightly different. Only 7.6% of single-family residential respondents expected a decline in 2025, but a third of industrial survey takers anticipated a drop.

Future Opportunities and Challenges

On average, 31.8% of companies have expansion plans in 2025 and 22.7% have no future expansion plans, leaving 45.5% planning to expand some time beyond 2025. Across market segments, about a quarter of the respondents engaged in post-frame construction report they have no expansion plans, but the multifamily (17.0%) and agricultural (17.7%) are less likely than the other market segments.

Companies in the agricultural market (38.2%) were most likely to report they planned to expand in 2025. Only 25% of industrial market companies looked to expand next year.

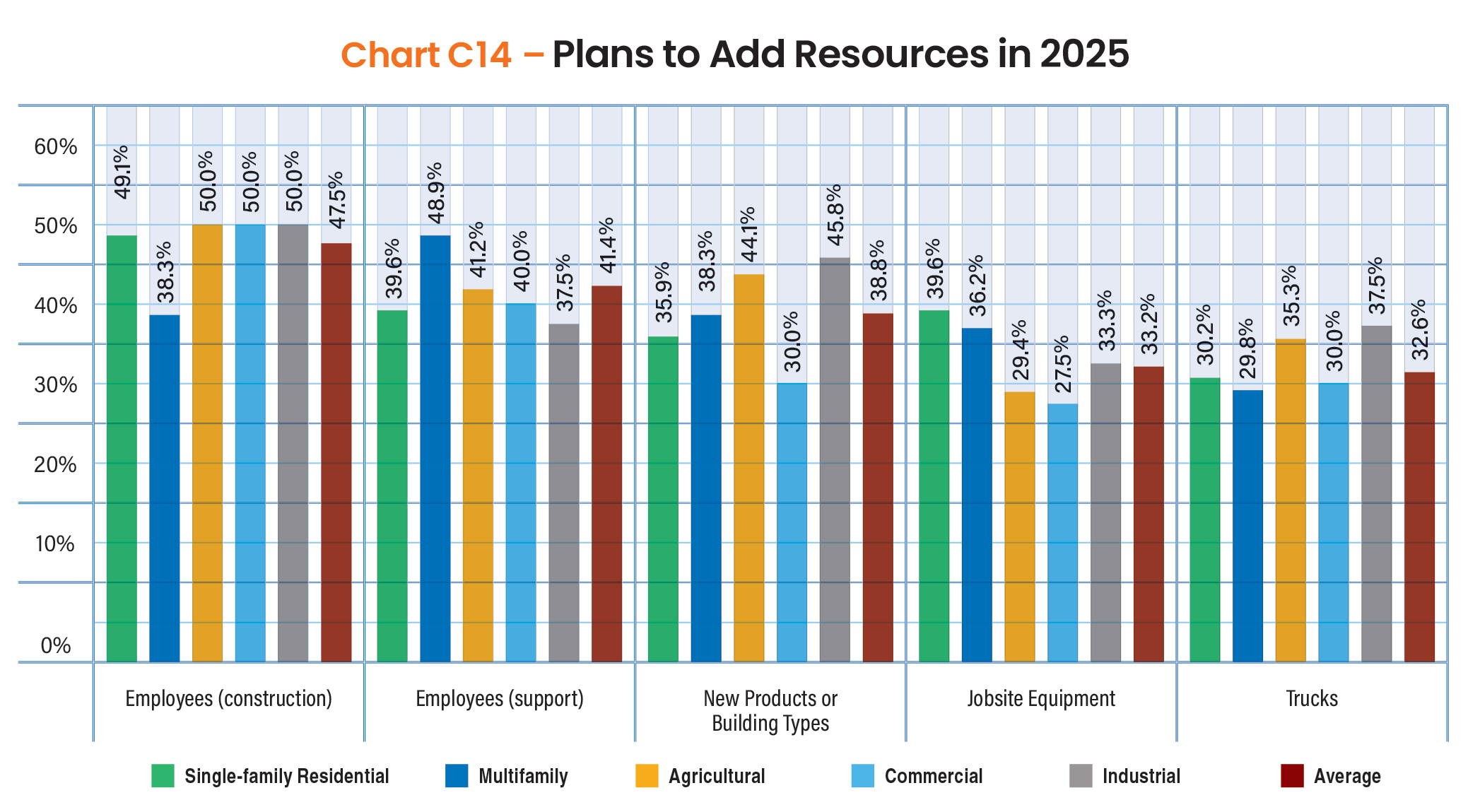

Expansion plans require the addition of resources. For many companies, maintaining business size means adding resources as well, especially as employees depart or equipment goes out of service.

Among a list of twelve potential resources, respondents from companies engaged in post-frame construction identified the most pressing needs as adding employees, both construction and support. Of all the market segments, those doing multifamily (38.3%) work were least likely to say they were going to add construction employees. About half of each of respondents in the other market segments said they would add construction employees. But multifamily companies (48.9%) were more likely to look at add support employees than any other market segment.

Companies in the construction industry face all kinds of challenges, some day-to-day and others potentially upsetting the entire industry. For years, the industry has battled a shortage of skilled labor, and companies engaged in post-frame construction have felt that bind as well.

But in our survey this year, one particular challenge kept rising to the top of the concerns: material costs. On average, 62.5% of survey takers said rising material costs were going to be the big challenge in 2025. Respondents in all market segments agreed with that sentiment. The likelihood of them choosing that was 58.3% at the low end among industrial companies and 67.9% at the high end among single-family residential companies.

Inflation, rising employee costs, interest rates, and material availability (shortages) all combined to make the material cost issue the most challenging respondents face in the coming year. And the specter of tariffs certainly had business owners in the post-frame construction market concerned.

Ben Nystrom, CEO of MWI Components, Spencer, Iowa, sums it up. “Weather, finding quality candidates, and uncertainty regarding a new administration discussing tariff,” he says, “ are all going to be challenges.”