In research released last Fall, the Metal Roofing Alliance reported that the housing market slowdown in 2023 caused a decline in the metal roofing market. That slight decline coincided, though, with an increase in the share of the market. Metal roofing now has roughly 18% of the residential market. Going forward, the goal will be to hold market share and ride a rising construction market.

Renee Ramey, executive director, Metal Roofing Alliance, says, “We are optimistic the economy will be strong and that homeowners’ desire to renovate utilizing eco-friendly, durable, sustainable products will continue to grow. Unfortunately, the number of extreme weather events (hurricanes, hail, and wildfires) was not something I think any of us anticipated. The amount of loss and the widespread need to rebuild was a surprise. It is our hope we continue to drive awareness for more sustainable building materials that can help harden homes against such events.”

The wildfires in Los Angeles in early 2025, in particular, have drawn attention to the kind of resilient construction that metal roofing helps bolster.

Characteristics of the Metal Roofing Industry

The largest cohort of respondents (25.7%) to the 2025 CSI annual survey were companies that primarily did general roofing. (See Section 1: Survey Participant Profile.) Companies whose primary building type was metal roofing came in at 7.8%. When asked what other building types respondents participated in, general roofing came in at 36.5% and metal roofing 24.4%. Clearly a significant portion of the respondents in our survey were general roofers who also offered metal roofing as a service.

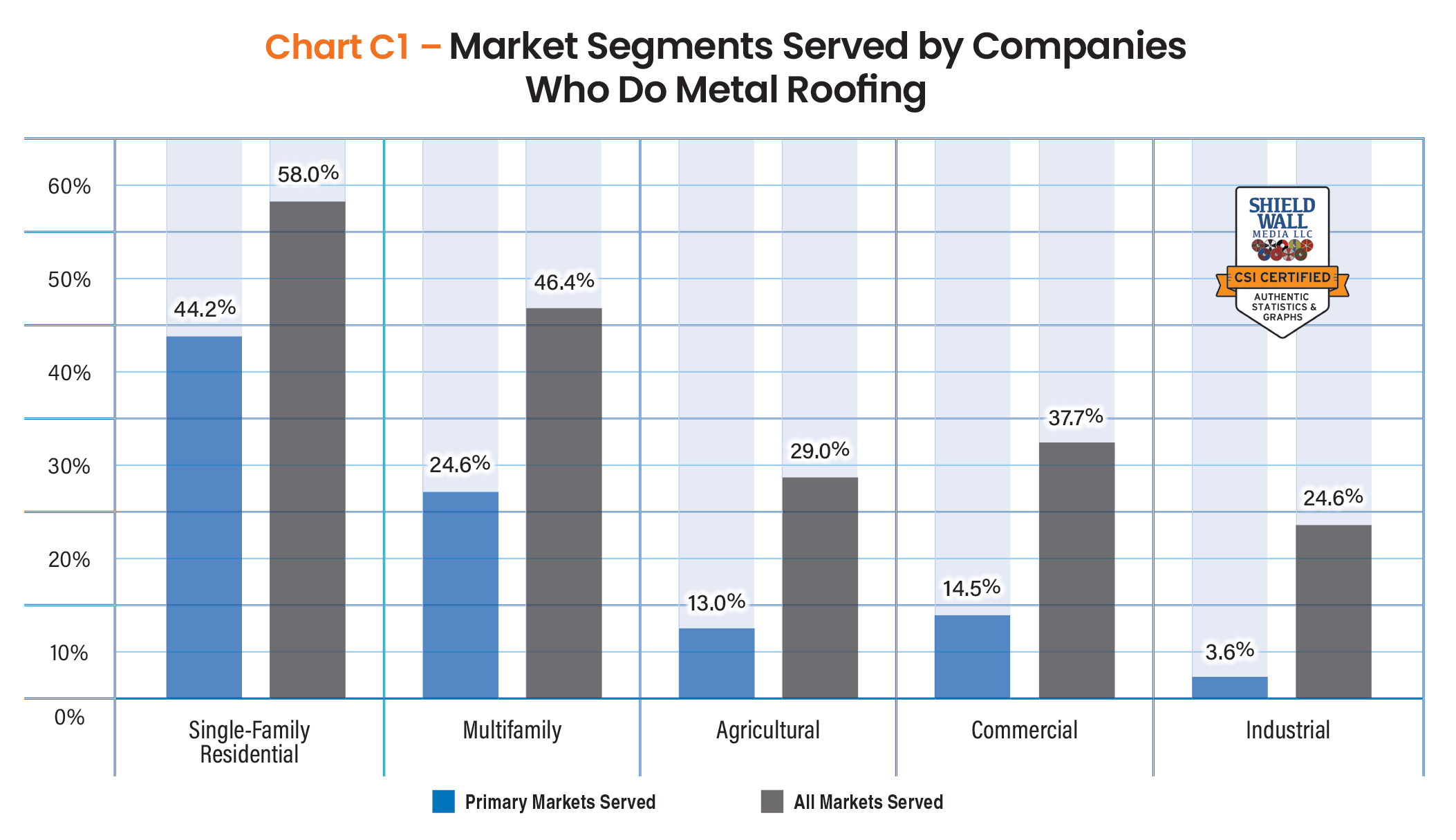

Breaking that participation out by the markets they served, we compared companies doing primarily metal roofing to those engaged in metal roofing. For both types of companies, single-family residential work was the predominant area of concentration, with 44.2% of companies primarily doing metal roofing in the single-family residential market and 58.0% of those only engaged in metal roofing.

Very few of our respondents did metal roofing on industrial projects and almost none of them (3.6%) were companies doing primarily metal roofing.

The large percentage of companies whose primary service was metal roofing that work in residential construction speaks to the type of companies doing that work. In our survey, they tended to be remodeling contractors specializing in that area. Companies in the commercial roofing business often offered a variety of roofing types other than metal.

Narrowing the survey down to only those companies that primarily did metal roofing left out a large number of companies doing metal roofing and at what could be a significant level. A general roofing company that did $20 million in gross sales might be getting $7 million of that from installing metal roofs, which would make them a much larger metal roofer than a $1 million company installing only metal roofs.

When we broke out the companies engaged in metal roofing, we found most of them were based in the South, with 35.5% percent of respondents in that region. There were a few national companies (2.9%), who were probably manufacturers, and both the Midwest and West regions accounted for about a fifth (22.5% for both regions) of respondents.

Of the 238 companies reporting they were engaged in metal roofing, 47.8% were builders or contractors. Given the high percentage of respondents engaged in the residential market, that would be understandable. Designers made up 26.8% of the survey takers engaged in metal roofing, while material dealers, distributors, or suppliers comprised 14.5% and manufacturers 10.9%. Those breakouts are nearly identical to the breakouts for the 2024 CSI annual survey.

As the Metal Roofing Alliance has shown in its reporting, a significant portion of the metal roofing market is residential, and a large part of that is retrofit. It’s a little surprising to see the percentage of companies who do primarily new construction among the companies engaged in metal roofing. Of the companies engaged in metal roofing, more than half (53.7%) did at least 60% of their work on new buildings. Only 5.1% of the companies did more than 90% remodeling work.

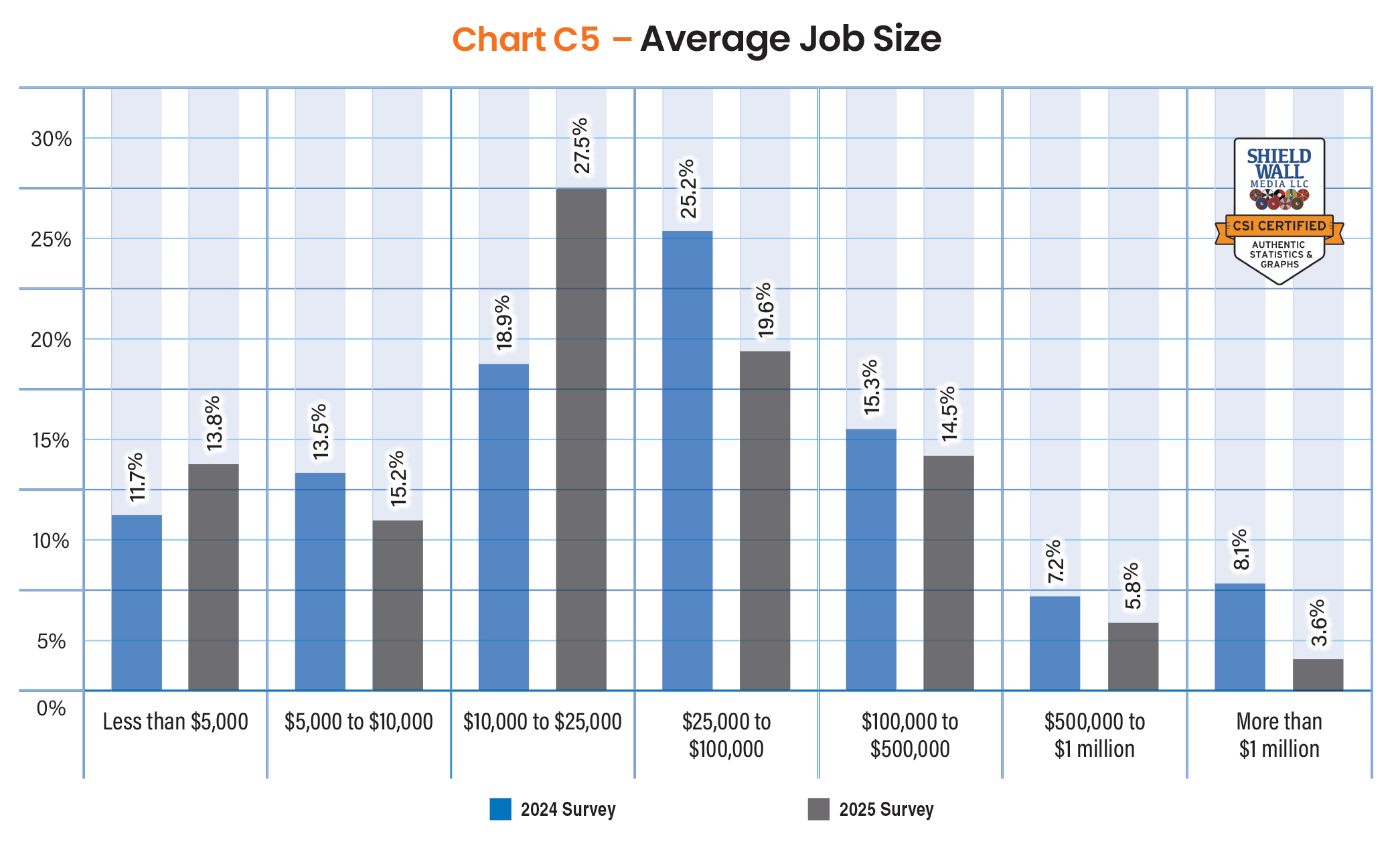

We contrasted the average job size as reported by companies engaged in metal roofing in the 2024 survey to the survey takers in 2025. In general, there was a higher predominance of smaller average job sizes among this year’s respondents. This year, 56.5% of respondents reported they had an average job size of less than $25,000 compared to last year when 44.1% said that. As reported elsewhere, there were a number of respondents who reported they offered handyman services, which may have skewed these numbers to smaller job sizes.

Projected Industry Growth

Our respondents to the 2025 CSI annual survey were generally more optimistic about the upcoming year (2025) than last year’s survey takers were about 2024. The percentage saying the general business climate in the construction industry would improve in 2025 rose to 47.8% from 41.1% last year, which is a 16.3% increase year over year. Just as importantly, the percentage expecting a poorer business climate in 2025 dropped slightly to 15.2% from 16.1% from last year’s survey.

Jim Bush, vice president of sales and marketing, ATAS International, Allentown, Pa., puts this into more specific terms. “While the industry appeared to enter into a softening period during the second half of 2024,” he says, “I believe the first half of 2025 will continue in this manner with an improving market during the second half of 2025.”

Complementing that sentiment is Rob Heselbarth, director of communications, PAC-CLAD, Elk Grove Village, Ill., who spends a lot of time talking to professionals at trades shows and industry meetings. “They indicate confidence in 2025,” he says, “as do the industry reports and as do PAC-CLAD executives.”

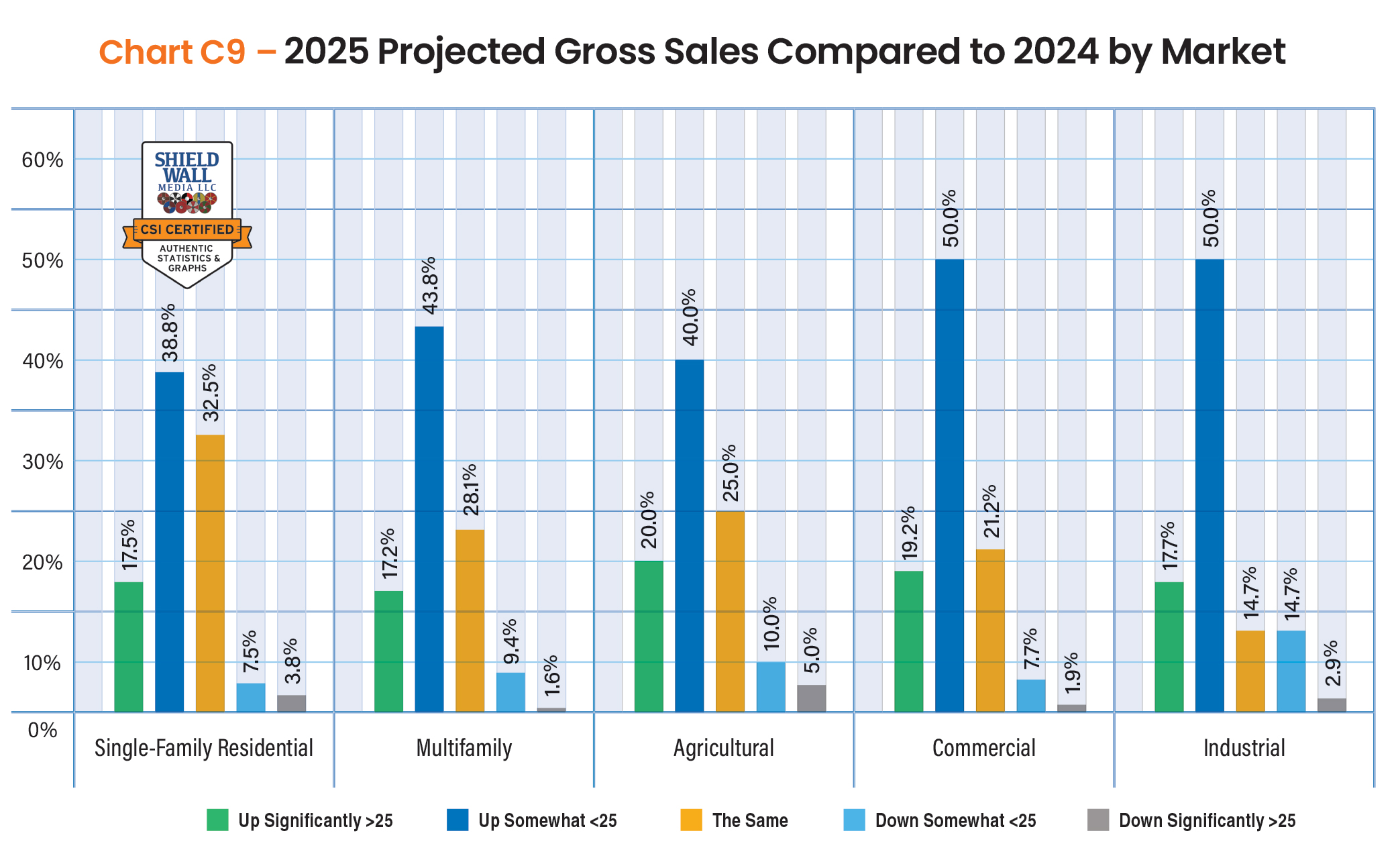

Our survey asked respondents to prognosticate whether the construction activity in individual markets would increase, stay the same, or decrease. Among companies engaged in metal roofing, there was a relatively even sentiment across market segments about construction activity improving with 50% of respondents saying the residential market would improve, 47.1% seeing improvement in the agricultural market, 47.8% expecting commercial construction activity to rise, and 46.4% looking for an increase in industrial construction.

That’s not to say 2025 will come roaring out of the gates. Bush says, “The drawback of construction starts out of ground in 2023 and 2024 affected the industry in late 2024. As we move into the latter half of 2025, we will see the upcoming construction starts begin to improve and the economy settle into the new market dynamics.”

Company Size and Growth Projections

Among companies engaged in metal roofing, the year-over-year growth they experienced in 2024 was remarkably consistent across all the market segments. At the high end, 62.5% of companies serving the single-family residential market showed increased gross sales in 2024. At the low end, 52.9% of companies serving the industrial market reported 2024 gross sales increases.

Within those increases was some differentiation. The single-family companies (26.3%) and agricultural companies (25.0%) were far more likely to have significant (greater than 25%) growth than the other market segments.

When looking at declining revenues, companies serving the commercial construction market (19.2%) were most likely say gross sales declined in 2024, but only 1.9% said the drop was significant.

While companies engaged in metal roofing work in the commercial market segment were most likely to report a decline in 2024, they were the most likely to anticipate an increase in gross sales in 2025 with 69.2% expecting sales to go up this year. Nearly a fifth of them (19.2%) expected the increase to be greater than 25%.

Individual businesses are the engines that drive industry and market economies. For the most part, respondents engaged in metal roofing were bullish on 2025, and the businesses serving this market more often than not expected their gross sales to increase this year. Survey takers responded almost evenly that gross sales would jump significantly. Twenty percent of agricultural companies saw a big increase in gross sales coming, and at the bottom end, 17.2% of multifamily companies anticipated significant growth.

Future Opportunities and Challenges

Anticipating growth is one thing, but planning to expand a business shows a robust belief in both the strength of your company and the prospects for the industry. By that measure, just under 40% of the respondents who were engaged in metal roofing had plans to expand their operations in 2025. Agricultural companies (40%) were most likely to report expansion plans for this year and 32.7% of companies in the commercial market segment anticipated expanding in 2025, which was the least likely of all the market segments.

As far as plans to expand beyond 2025, 23.8% of companies in the single-family residential market said they had no expansion plans, and 21.2% of commercial companies held similar attitudes. Only 10.9% of respondents in multifamily said they had no expansion plans, making that market segment the most optimistic.

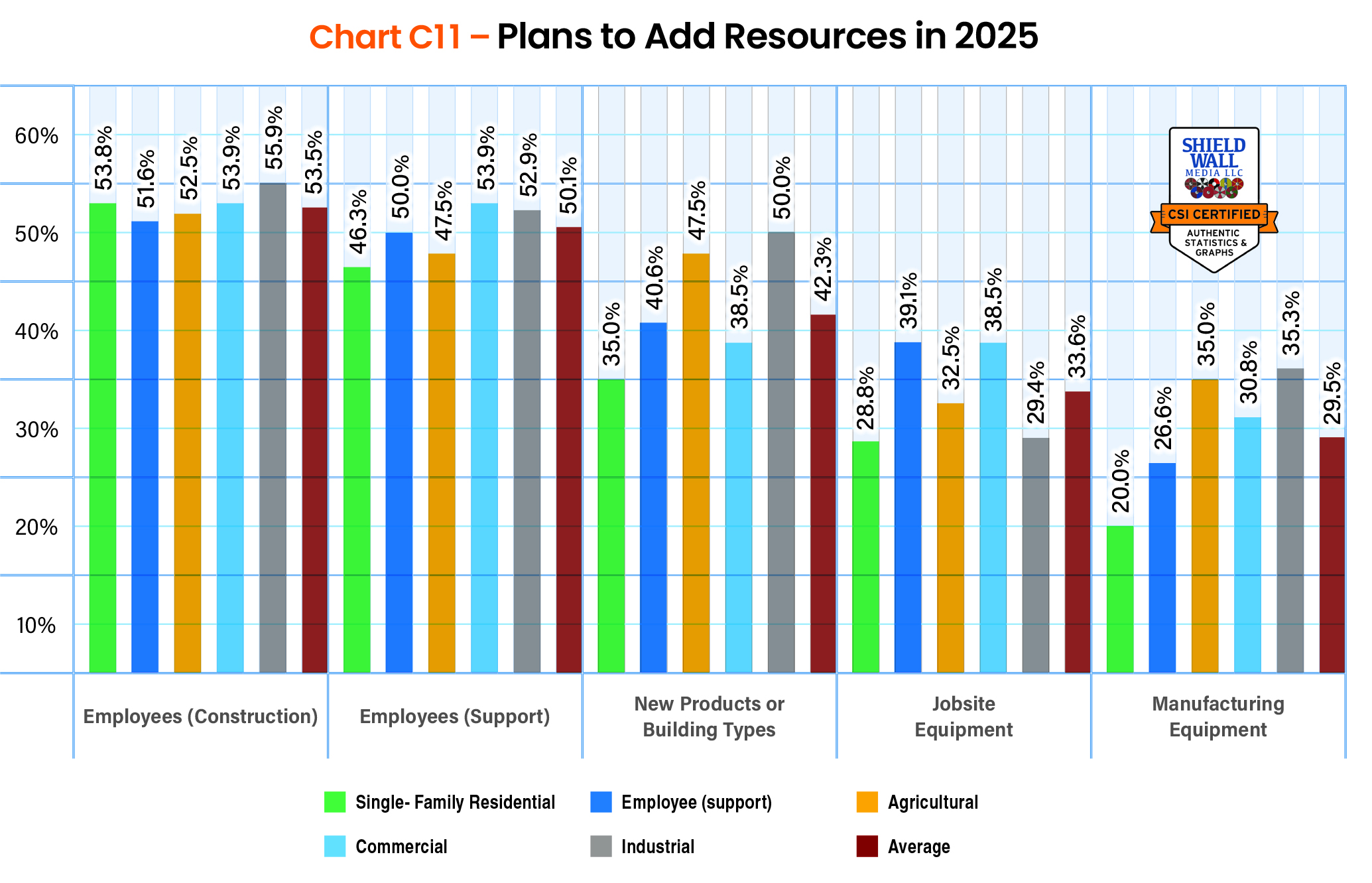

In every section in the 2025 CSI annual survey, companies identified adding employees in 2025 as one of those resources, but among companies engaged in metal roofing, finding employees (construction and support) were the top needs. More than half of the companies said they wanted to add employees: 53.5% looking for construction employees and 50.1% hiring support employees.

Among companies engaged in metal roofing, the likelihood of saying they wanted to add construction employees was almost identical across the market segments. And the spread of response rates across market segments for companies looking to add support employees was not very significant either, with 46.3% of single-family residential companies as the low end, and 53.9% of commercial companies as a high end.

Rounding out the top five resources companies engaged in metal roofing planned to add were new products or building types, jobsite equipment, and manufacturing equipment. The only consistency about adding resources across building types was everyone identified the need for employees as a top three requirement.

Technology is impacting every element of the construction industry. For the companies engaged in metal roofing, the biggest impact they said will be from design and engineering software with 49.4% reporting that is most likely to have the greatest effect on their business. Manufacturing automation (44.6%) and artificial intelligence (44.5%) were close behind. According to our respondents, the impact of artificial intelligence on companies engaged in any of the building types in this report is remarkably consistent.

Among the new technology and products mentioned by respondents, the top five were all related to increased efficiency. Other advances, such as drone imagery and 3D printing, rated much lower.

As with the respondents to the survey overall and for those engaged in each building type, rising material costs was seen as one of the biggest challenge for our industry. Among companies engaged in metal roofing, nearly two-thirds (64.6%) said material costs would be a challenge in 2025. The next closest was finding employees – the perennial difficulty in the construction industry – where 48.7% expected to be facing that difficulty in 2025.

Other employee-related issues, such as increasing employee related expenses and retention all came out near the top of the challenges the respondents expected to see in 2025.

All of the cost issues, of course, are interrelated, so it’s no surprise that inflation and high interest rates are also going to be challenges next year for companies engaged in metal roofing.

Unlike other areas of the construction industry, the metal roofing sector still seems to be facing some lingering supply chain management. About a third of respondents (34.6%) said supply chain issues would be a challenge.

Jim Bush brings a broader perspective to the challenges the industry is facing. “Regulatory issues such as building codes and the over selling of competitive products as having green or sustainable attributes are a challenge,” he says. “As an industry, the metal community must develop a consistent message of the value we bring to this changing landscape of sustainable initiatives.”