Driven in no small part by the investments as a result of the Infrastructure Investment and Jobs Act (IIJA), the construction industry has been on a steady rise over the last two years with increased spending and greater employee demand. In spite of rising interest rates and their effect on the housing market, the industry overall has been a very positive point in the U.S. economy.

Census Data and Association Forecasts

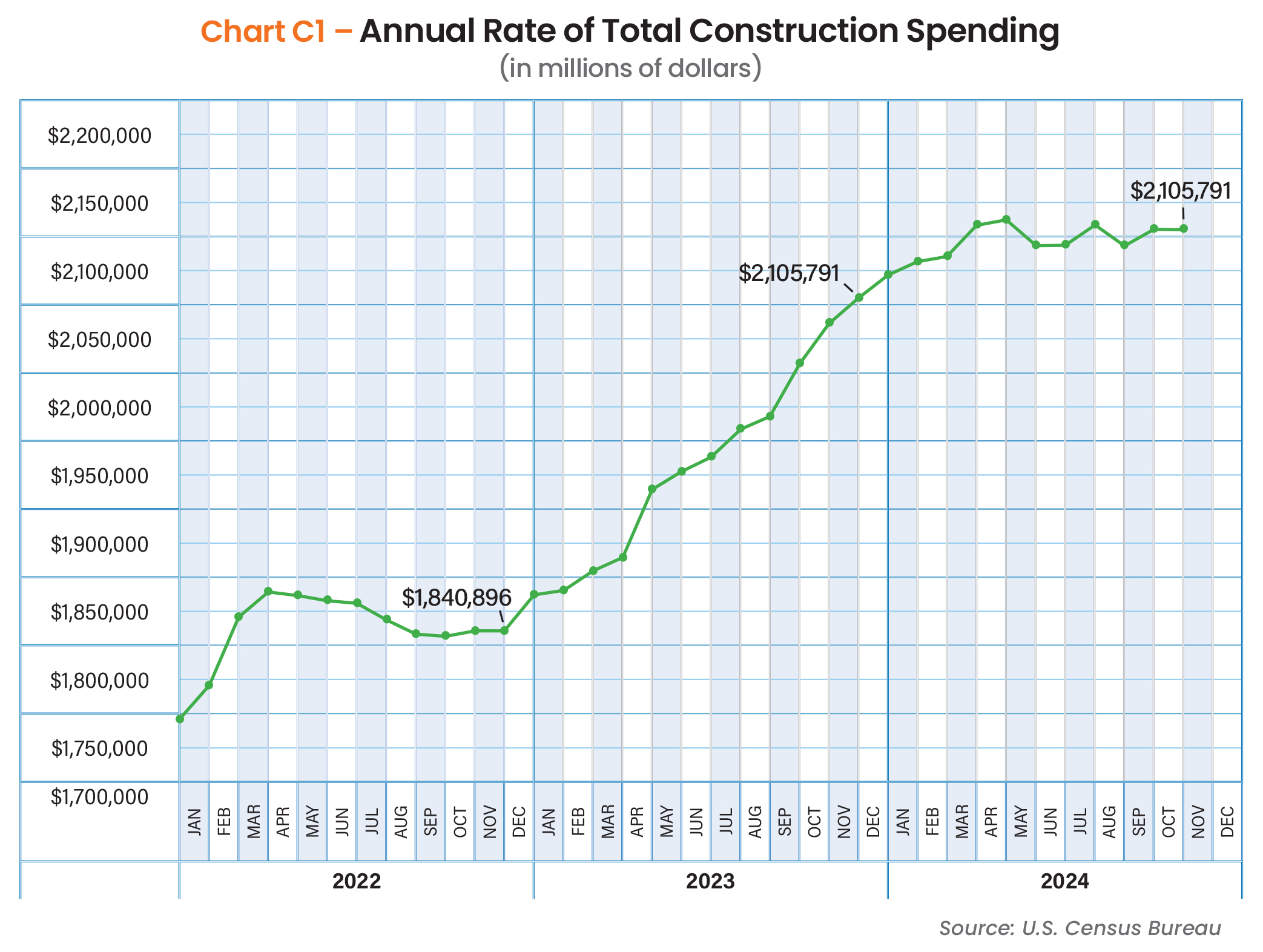

Between 2022 and 2024, U.S. construction spending exhibited notable growth. In 2022, total construction expenditures were approximately $2.02 trillion. By December 2024, this figure had risen to $2.19 trillion, marking an increase of about 8.5% over the three-year period.

Residential construction played a significant role, accounting for 43% of all construction spending in 2024, with expenditures reaching $930 billion annually. Within this sector, single-family homes comprised 45%, multi-family units 15%, and renovations 40%.

The implementation of IIJA contributed to this upward trend, with approximately $400 billion allocated to over 40,000 projects by November 2023. By November 2024, funding had increased to $568 billion for 68,000 projects, indicating accelerated investment in infrastructure.

Overall, the period from 2022 to 2024 saw steady growth in U.S. construction spending, driven by significant investments in both residential and infrastructure projects.

Total private construction spending from 2022 to 2024 showed fluctuations driven by economic conditions, interest rates, and supply chain factors. In 2022, private construction spending was robust, fueled by post-pandemic demand, low interest rates early in the year, and ongoing residential growth. However, as the Federal Reserve raised interest rates to combat inflation, residential spending slowed, impacting overall private construction investment.

In 2023, spending growth remained mixed. The residential sector faced affordability challenges due to high mortgage rates, leading to a slowdown in new home construction. However, multifamily and nonresidential sectors, including manufacturing and infrastructure-related projects, saw gains, buoyed by reshoring efforts and federal incentives.

By 2024, private construction spending showed signs of stabilization. Easing inflation and expectations of potential interest rate cuts improved housing demand, supporting residential construction. Nonresidential investment, particularly in industrial and commercial projects, remained strong, driven by technology sector growth and federal investments in manufacturing. Despite lingering economic uncertainties, private construction spending in 2024 reflected a more balanced trajectory, with resilience in nonresidential sectors offsetting continued affordability concerns in housing.

Since 2022, public construction spending in the United States experienced notable growth. In 2022, the federal, state, and local governments collectively invested nearly $451 billion in public construction projects. According to the U.S. Census Bureau, public construction spending in December 2024 was approximately $503.6 billion, measured at a seasonally adjusted annual rate.

This upward trend was significantly influenced by the IIJA. Spending on highway and street construction saw consistent increases, reflecting federal and state priorities in transportation upgrades. Educational facility construction also trended upward, supported by local bond measures and funding for school modernization. Additionally, public spending on water supply and sewage systems expanded as cities focused on climate resilience and sustainability.

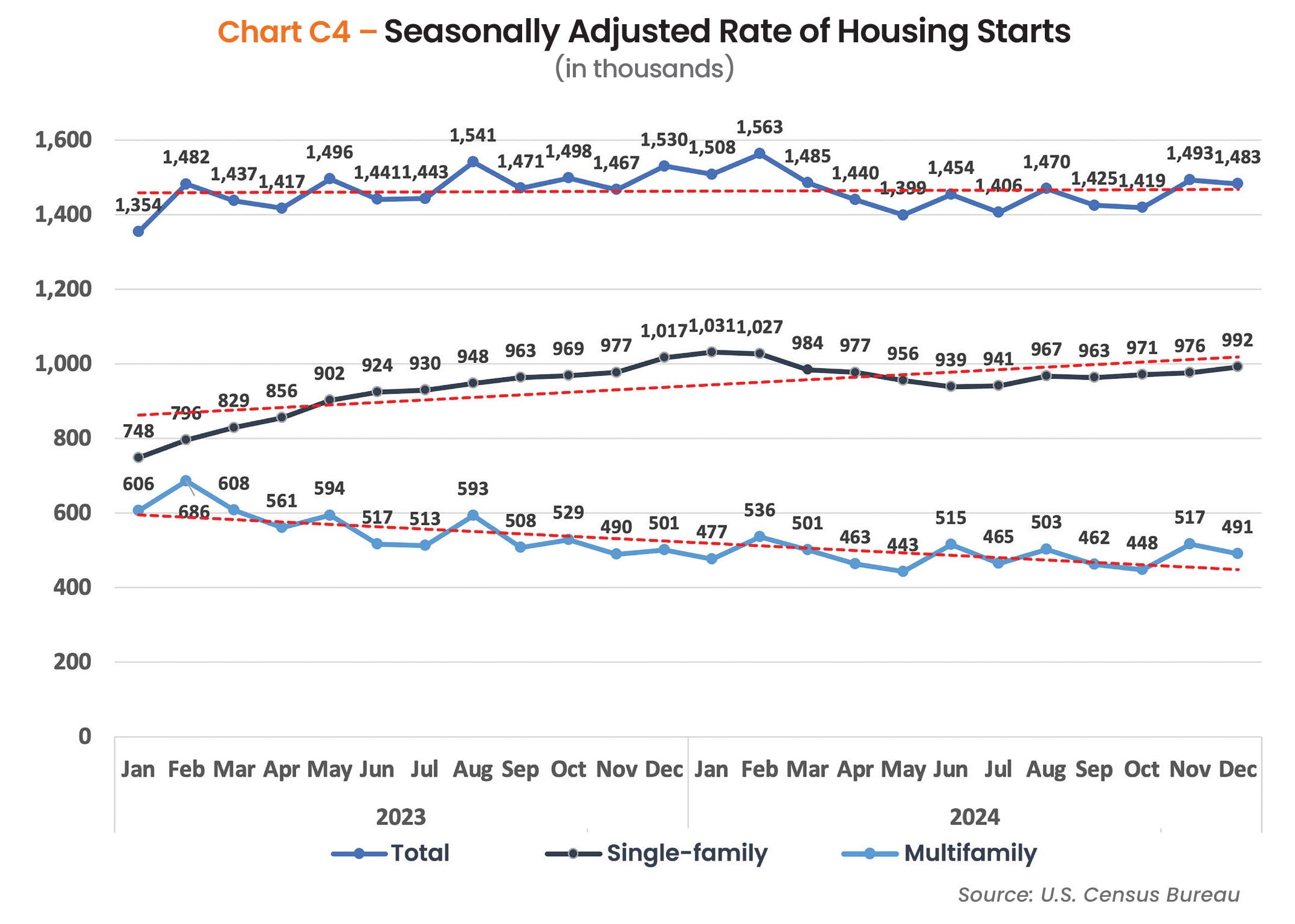

Housing starts in 2023 faced challenges from high mortgage rates, persistent inflation, and supply chain disruptions. The year began with a slowdown as affordability concerns dampened demand. However, as inflation cooled and interest rates stabilized in late 2023, homebuilder confidence improved, leading to a gradual recovery.

Single-family housing starts saw a modest rebound, driven by pent-up demand and a shortage of existing homes. Multifamily starts, however, declined due to oversupply in some markets and tightening financing conditions. Builders responded by focusing on smaller, more affordable homes and offering incentives to buyers.

In 2024, housing starts showed signs of strengthening as the Federal Reserve signaled potential rate cuts, improving affordability. Supply chain conditions also improved, helping construction costs stabilize. However, regulatory constraints, labor shortages, and high land costs remained barriers to rapid expansion.

The National Association of Home Builders noted that builders added more supply in response to the housing affordability crisis, despite elevated mortgage interest rates and higher construction costs.

The NAHB Remodeling Index (RMI) from 2022 to 2024 has shown fluctuating trends in the remodeling industry, however it has remained above the 50 point mark, indicating remodeling contractors felt market conditions were good. In 2022, the index remained strong due to high demand for home improvements, driven by pandemic-related shifts in work and lifestyle. However, by 2023, rising material costs and interest rates began to impact consumer spending and project affordability. In 2024, the RMI stabilized, showing modest growth as the market adapted to economic pressures.

Between 2023 and 2024, the U.S. construction industry experienced notable employment growth. In the first eight months of 2024, approximately 1.475 million jobs were added, averaging 184,000 new positions per month. This rate is slightly below the 251,000 monthly average gain observed in 2023.

State-level data reveals that between June 2023 and June 2024, 35 states added construction jobs, while 14 states and the District of Columbia saw declines. Texas led with an increase of 36,100 jobs (4.4%), followed by Florida with 29,900 jobs (4.8%), Michigan with 14,400 jobs (7.6%), and Nevada with 12,800 jobs (11.5%).

In spite of a skilled labor shortage, the construction sector employed over 8 million people in November 2024, marking the highest employment level since 2008.

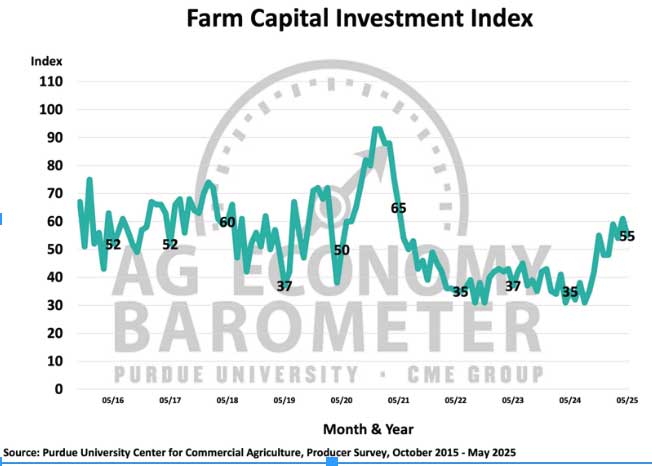

CSI Survey Attitudes

Shield Wall Media surveyed more than 550 contractors, designers, manufacturers, and suppliers who answered questions about the construction industry performance in 2024 and what they expected to see in 2025.

When it comes to industry and economic trends, all perceptions are local. No matter how the industry or market segment is doing, what matters is whether their business is growing and profitable. The following charts show how the respondents felt about the industry through the lens of their businesses.

We asked survey takers about their gross sales growth in 2024 compared to 2023, and how they expected the growth to change in 2025. One very quick conclusion could be drawn. Our respondents didn’t expect much change from 2024 to 2025.

Just under 13% said business was up significantly in 2024, and almost the exact same percentage said they expected the same kind of growth in 2025.

It didn’t matter if we asked if they were up somewhat (less than 25%), business held steady, declined somewhat (less than 25%) or down more than 25%, the percentage of survey takers who said their business would continue on the same growth trajectory was almost exactly the same.

Mark Stover, president, Perma-Column LLC, Ossian, Ind., put some the activity in a different perspective. “The pace of activity has slowed down,” he says, “and is more normalized and seasonal.” After COVID, the pace and normality seemed to be upended.

Unless a company experienced steady, controlled growth, it’s incredibly difficult to match growth with profitability. Too often gross sales jump so rapidly, that costs accelerate beyond the normal mark-up and profits plummet.

Interestingly, respondents were more likely to report significant profitability increases than gross sales jumps. As mentioned earlier, 12.8% of respondents reported gross sales increases of greater than 25% in 2024, but 13.6% said profits increased more than 25%. The difference in expectations for 2025 among those who expected significant gross sales increases (12.6%) also was less than those who expected significant profitability increases (14.6%)

The real differences showed among respondents who had more modest gross sales increases. In 2024, 30.3% of our survey takers say gross sales increased less than 25% and 29.6% expected a similar increase in 2025.

But far more companies reported modest profit increases than modest gross sales increases. Last year, 32.3% saw profits increase less than 25%, which isn’t a lot more than reported gross sales increased, but 36.8% expect profitability to improve moderately in 2025. That is a noticeable difference to those expecting gross sales to climb moderately next year.

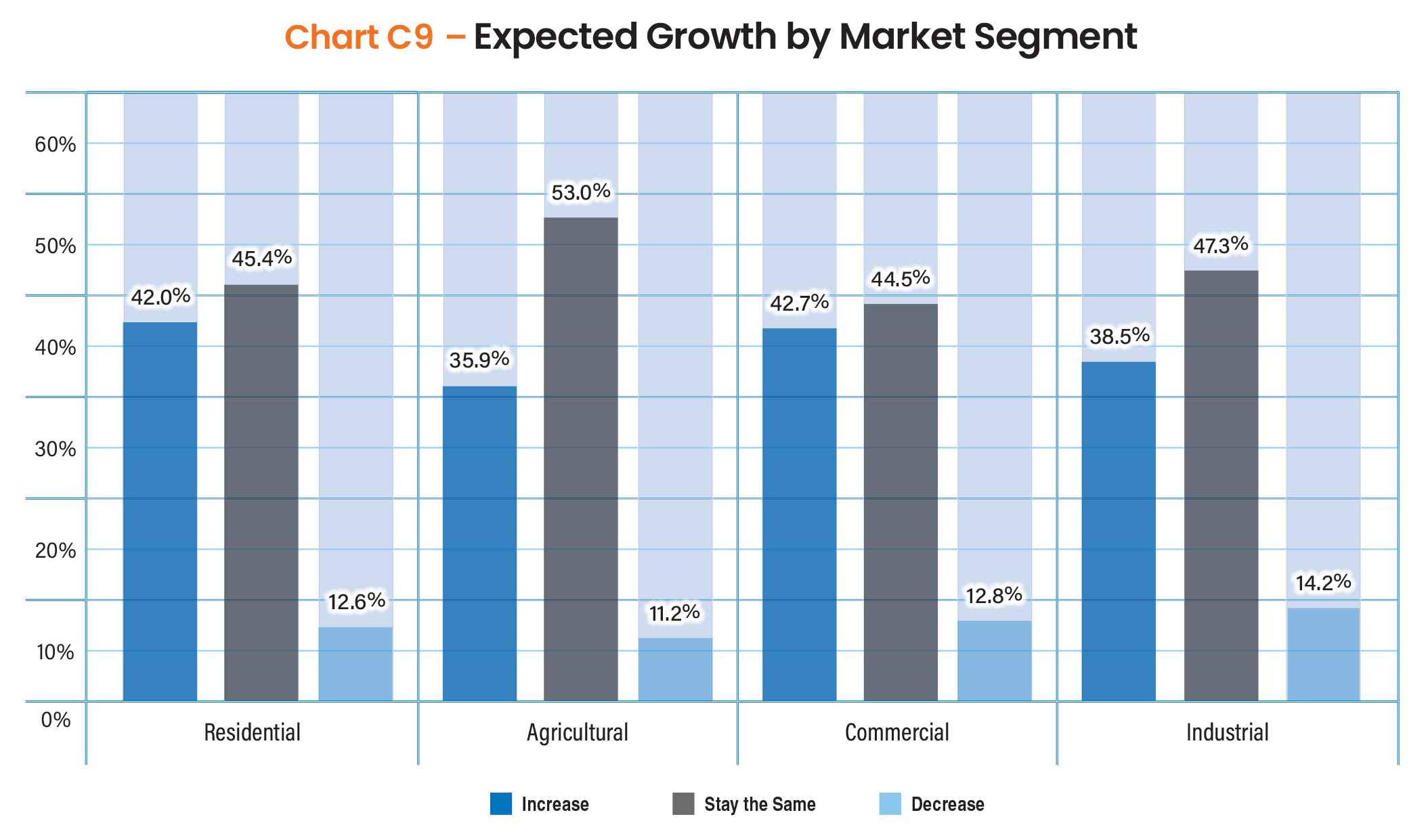

The following charts look at the overall expected growth in different market segments, then dig into what the growth in specific regions by each market segment is expected to be.

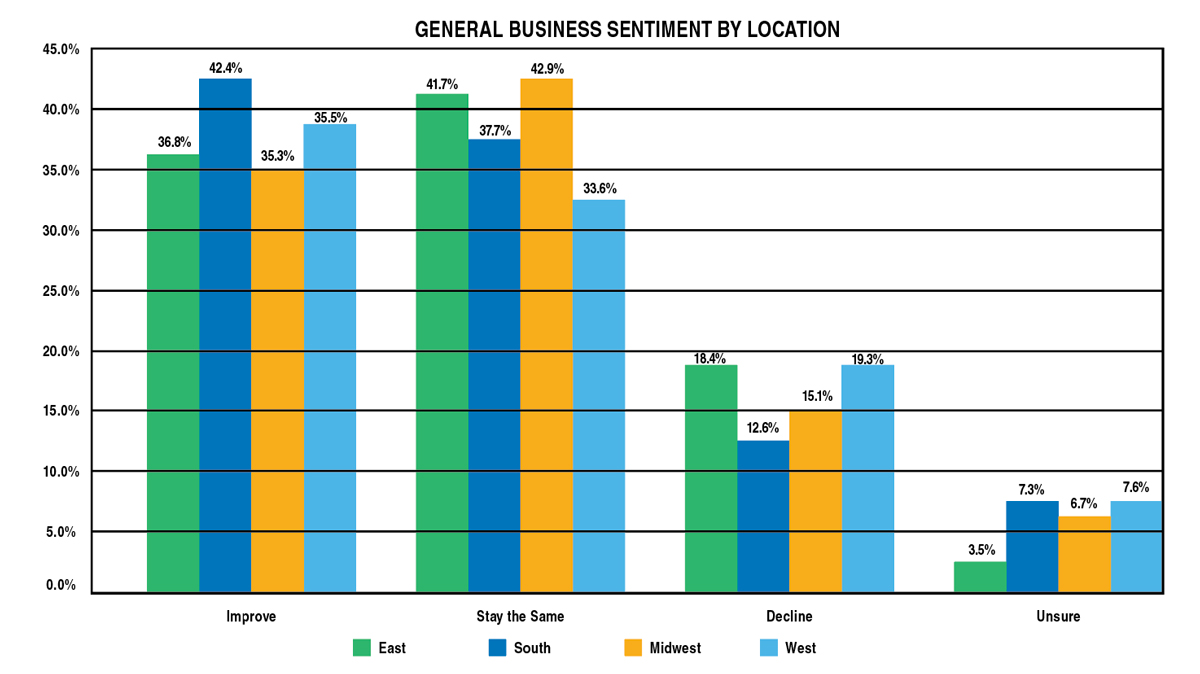

More of our respondents expected to see growth in the commercial (42.7%) and residential (42%) markets than either agricultural (35.9%) or industrial (38.5%). But a much higher percentage of survey takers (53%) believed the agricultural market would hold steady than thought any of the other markets would remain constant.

Consequently, expectations for declines in residential, agricultural, and commercial building segments were almost identical. And just slightly more (14.2%) of respondents expected a decline in the industrial market.

Chance Shalosky, Roofing Product Manager, ProVia, says, “Anticipated economic recovery and continued growth in construction activities, especially in sectors like residential housing and commercial developments, are likely to increase demand for reliable and innovative roofing solutions.”

When we asked if respondents had plans to expand their business in the next year or the immediate future, we received slightly different responses between last year’s survey and this year’s. In the 2024 survey, nearly 30 percent of respondents expected to expand in 2024. But only 22.8% of respondents in this year’s survey had immediate expansion plans.

However, this year’s survey takers were more optimistic about future expansion plans. Ben Nystrom, CEO of MWI Components, Spencer, Iowa, says, “Everyone I talk to – builders, wholesalers, lumber yards, and rollformers – say they are busy booking and quoting jobs.”

There are a lot of positive signs, but companies still seem to be holding capital in check against a rainy day.

Of the top ten things our respondents plan to add to their businesses in 2025, the first two are employees – both construction and support. The chronic skilled labor shortage makes it obvious that a third of respondents would say they need construction employees. But the 30.6% who say they need support staff suggests that growth is outstripping their ability to keep up with all the back office work needed to control growth and serve customers. That can be good for profitability (see the previous charts) in the short run but can slow growth in the long run.

The bottom six items (jobsite equipment, trucks, real estate or facilities, manufacturing equipment, material handling equipment, and metal forming equipment) all support the ongoing work and represent an investment – either through a capital influx or leasing contracts – in the company.

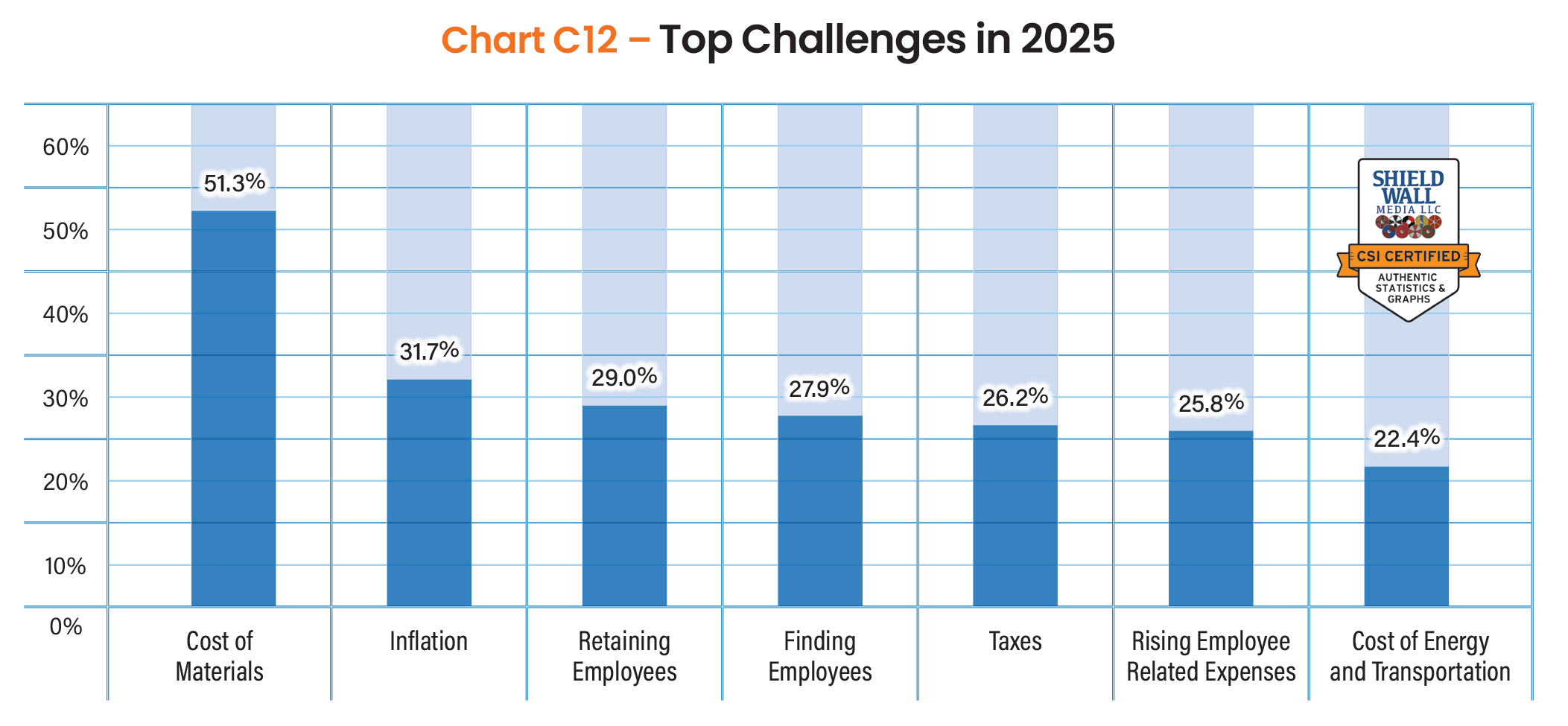

Our respondents pointed to two items at the top of their list that are related to controlling cost of materials (51.3%) and inflation (31.7%). That more than half of survey takers identified concerns about the cost of materials as one of their biggest challenges in 2025, speaks to the ongoing difficulty of managing those costs since the beginning of the pandemic. First it was supply chain issues (no longer a challenge for most respondents) and now it is increasing inflation and worries about tariffs.

Retaining employees in a rapidly increasing costs environment is always a challenge. Combine that with the now decades-old difficulty of finding qualified skilled labor and it’s surprising that employee recruitment and retention aren’t identified by even more respondents.

Among a long list of potential product or technologies that could impact their businesses, our respondents identified a few they thought would be most impactful. Compared to last year, though, not a lot changed about those attitudes. Design and engineering software, artificial intelligence, and manufacturing automation were all identified by about a quarter of respondents as most likely to have the greatest impact on their businesses.

Last year, all three of these impacts were selected by about the same percentage of respondents. Two years ago, before this annual survey kicked off, artificial intelligence probably would not have warranted a second thought, but the introduction of ChatGPT and other generative AI programs changed that. They have become more integrated into business operations, especially in marketing.

Not on this chart, but in the list provided, were 3D printing and augmented reality, two technologies that a few years ago were thought to be poised for a significant impact on businesses in the construction industry. None of that has panned out, and fewer than 10% of our respondents expected either of those to impact them.