Since 2021, the U.S. economy has experienced significant shifts driven by inflation, interest rate hikes, labor shortages, and supply chain disruptions. The post-pandemic recovery saw strong consumer demand, but inflation surged to a 40-year high in 2022, prompting aggressive Federal Reserve rate increases.

These actions slowed economic growth, cooled the housing market, and led to higher borrowing costs. While inflation has eased, construction costs remain elevated due to labor constraints and material price volatility. Job growth has been steady, yet skilled worker shortages persist. Understanding these economic trends is crucial for assessing their ongoing impact on the construction industry.

Two Years of Battling Inflation

Inflation has been a dominant economic challenge for nearly four years, peaking at 9.1% in mid-2022—the highest in four decades. The Federal Reserve responded with aggressive interest rate hikes, which helped cool inflation but also increased borrowing costs for businesses and consumers. While inflation has since moderated, construction costs remain stubbornly high due to persistent labor shortages and supply chain disruptions. Contractors continue to navigate fluctuating material prices and tighter financing conditions, making cost management a critical priority in the industry.

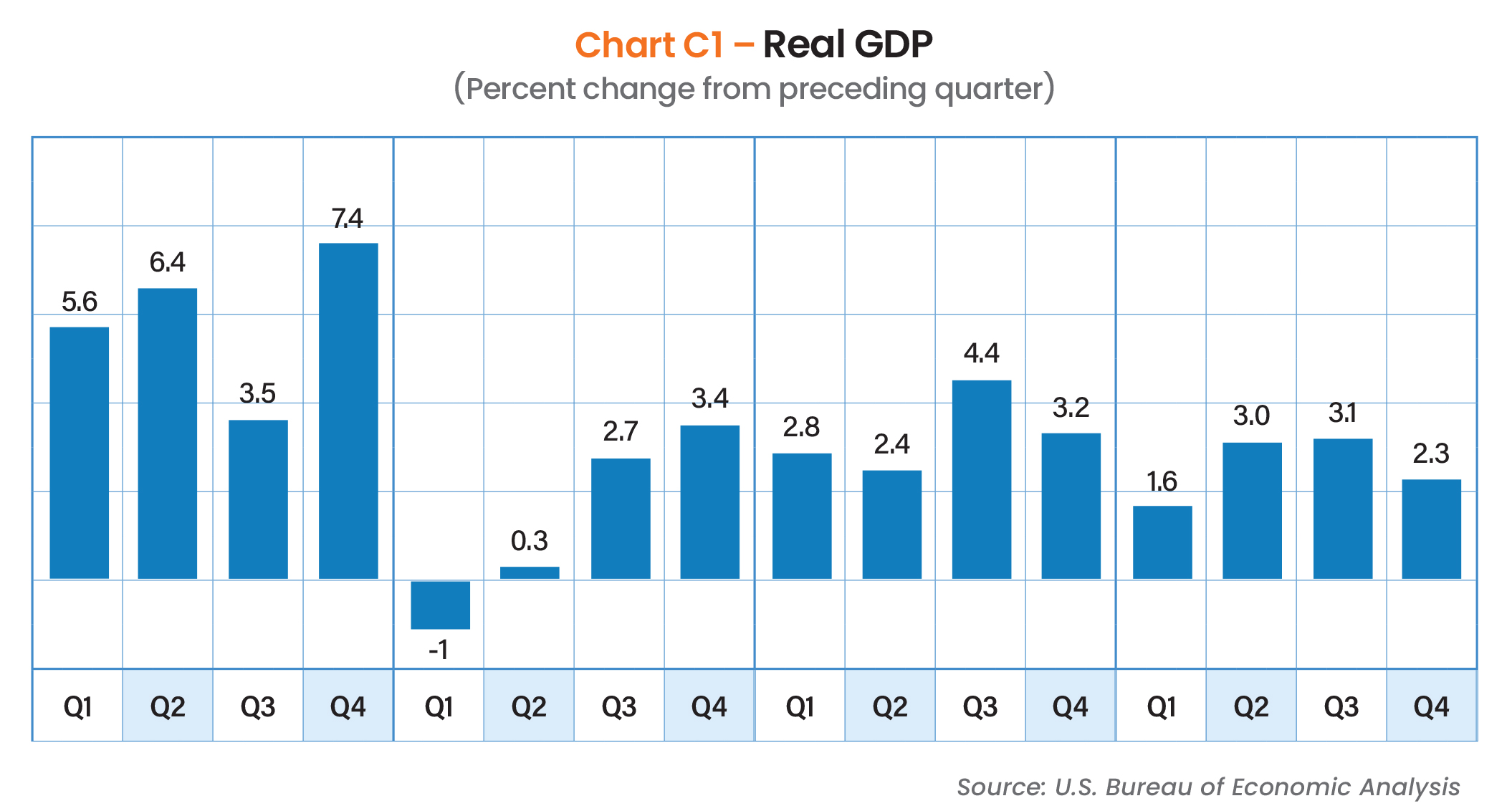

GDP

After the pandemic, U.S. GDP growth has fluctuated due to the economic recovery, inflationary pressures, and Federal Reserve policy. In 2021, the economy rebounded strongly, growing by 5.9% as consumer spending surged and businesses reopened. However, in 2022, growth slowed to 2.1% as inflation soared and interest rates rose. The first half of the year saw negative GDP growth, raising recession fears, but the economy avoided a prolonged downturn.

In 2023, GDP remained resilient, growing by approximately 2.5% despite high interest rates. Consumer spending, a strong labor market, and government investments in infrastructure helped sustain momentum. However, sectors like housing and construction faced headwinds due to rising borrowing costs. Entering 2024, growth remains positive but at a moderated pace as businesses and consumers adjust to higher costs. While inflation has eased, economic uncertainty persists, with GDP expansion depending on labor market stability, Fed policy, and global economic conditions.

Wages

Driven by inflation, labor shortages, and a competitive job market, employee compensation for civilian workers has risen significantly. According to the U.S. Bureau of Labor Statistics (BLS), total compensation—including wages, salaries, and benefits—has increased steadily each year. In 2021 and 2022, wages grew at their fastest pace in decades as employers struggled to attract and retain workers amid the Great Resignation. Private sector wages saw annual increases of over 4%, with some industries experiencing even higher growth.

However, these gains were often offset by inflation, which peaked at 9.1% in mid-2022. As a result, real (inflation-adjusted) wages declined during much of 2022, eroding purchasing power for many workers. In 2023 and early 2024, compensation growth remained strong, but inflation slowed, allowing for modest real wage gains.

Benefits costs have also risen, particularly for health insurance and retirement contributions, adding to employer expenses. Sectors like construction have had to offer higher wages and improved benefits to address persistent labor shortages. Looking ahead, compensation growth may moderate as the job market stabilizes, but demand for skilled labor, particularly in construction and manufacturing, will likely keep upward pressure on wages in those fields.

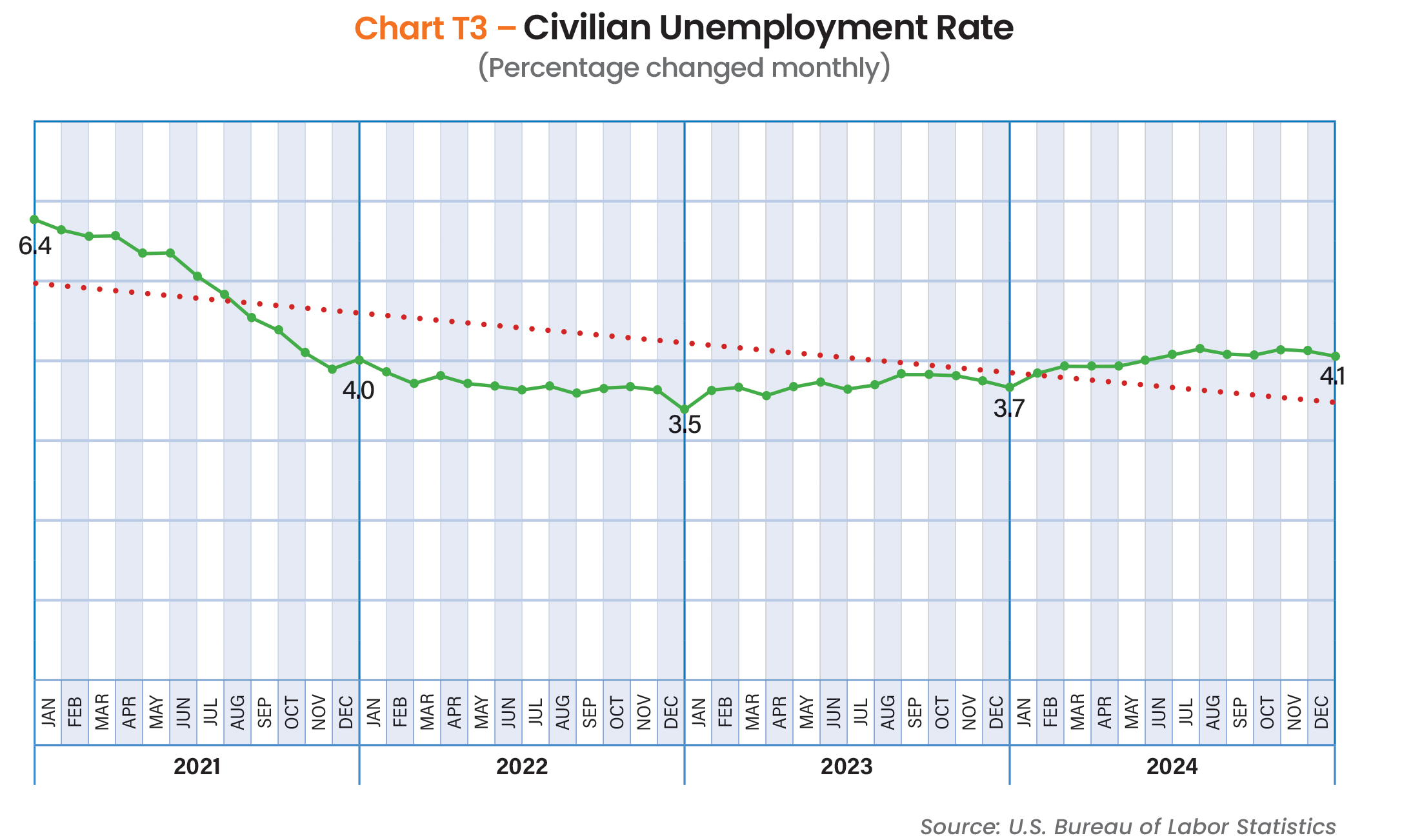

Unemployment

The U.S. unemployment rate has undergone significant shifts, reflecting the economy’s post-pandemic recovery, labor shortages, and monetary policy effects. In early 2021, unemployment remained elevated at around 6% as businesses reopened and rehired workers. However, strong economic growth and government stimulus fueled rapid job creation, bringing unemployment down to 3.9% by the end of the year.

In 2022, despite rising inflation and interest rate hikes, the job market remained resilient. Unemployment hovered between 3.5% and 3.7% for most of the year, indicating a tight labor market. However, employers struggled to fill positions, particularly in industries like construction and manufacturing, where skilled labor shortages persisted.

In 2023, the labor market remained strong, with unemployment staying near historic lows at around 3.5%–3.8%, even as the Federal Reserve raised interest rates to slow economic growth. Job openings declined slightly, but demand for workers remained high, especially in sectors like healthcare, hospitality, and construction.

As 2024 unfolds, unemployment remains low, though signs of softening have emerged. While job growth continues, some industries face hiring slowdowns due to higher borrowing costs and economic uncertainty. However, overall labor market conditions remain favorable, supporting continued wage growth and consumer spending.

Manufacturing

Since 2021, manufacturing employment has seen steady growth, driven by strong demand, supply chain adjustments, and government investments. After initial pandemic-related job losses, the sector rebounded, adding hundreds of thousands of jobs in 2021 and 2022.

However, labor shortages and rising wages created challenges. In 2023, manufacturing employment remained stable, supported by infrastructure spending and reshoring efforts, though higher interest rates slowed expansion in some areas. Entering 2024, job growth has moderated, with some sectors facing softer demand. Despite this, manufacturing remains a key employment driver, particularly in advanced manufacturing, clean energy, and semiconductor production.

Consumer Sentiment

The University of Michigan’s Consumer Sentiment Index has fluctuated significantly over the past four years, reflecting economic uncertainty, inflation, and interest rate changes. In 2021, sentiment was relatively strong as the economy rebounded from the pandemic, though concerns about rising prices emerged. By mid-2022, sentiment plunged to a record low of 50.0 due to soaring inflation, supply chain disruptions, and Federal Reserve rate hikes, indicating widespread consumer pessimism.

In 2023, as inflation eased and the job market remained strong, consumer sentiment gradually improved, though it remained below pre-pandemic levels. Rising borrowing costs and economic uncertainty kept confidence restrained. By early 2024, sentiment showed continued recovery, reaching its highest level in over two years as inflation moderated and wage growth outpaced price increases. However, consumer outlooks remain sensitive to economic conditions, with factors such as interest rates, job stability, and geopolitical events influencing future sentiment trends.

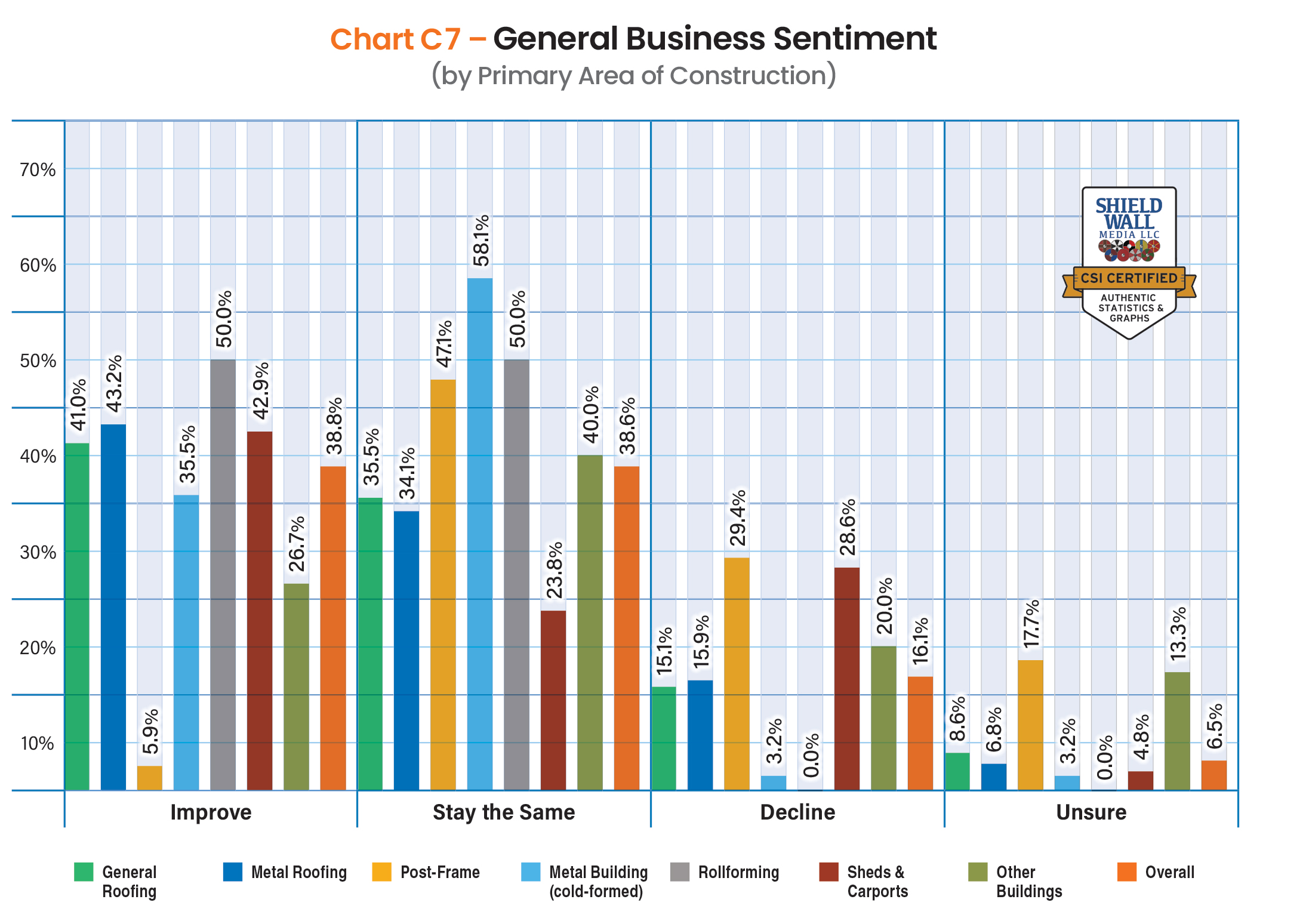

CSI Survey Attitudes Toward the Future

When asked what the business climate will be across the industry, 546 respondents were almost perfectly divided between saying it will improve (38.8%) or stay the same (38.6%).

The CSI survey went out after the November 5 national election, so there was no ambiguity about how economic policies might be implemented. Our survey takers had every reason to understand that the changes in the administrative and legislative branches would be certain and the policies discussed during the election would be put in place.

This represents a bit of sea change over the last several years where there was considerable partisan sentiment about handling inflation and other issues affecting the economy. Now, there is one sustained vision, although the University of Michigan’s Joanne Hsu, director of its Surveys of Consumers, said in December 2024, “Uncertainty over both short- and long-run inflation expectations… are considerably higher now than a year ago. One reason for the elevated uncertainty is the dispersion in beliefs about the consequences of anticipated economic policy changes.”

So, maybe it’s not much of a surprise that the sentiments expressed about the future in this year’s survey were not significantly different than last year. In the previous survey, 32.4% of respondents expected the general business environment to improve in 2024, and this year it rose slightly to 38.8%. Those who thought the economy would worsen in the next year declined slightly this year to 16.1% of survey takers versus 18.9% last year.

It is notable that there was less uncertainty. Overall, only 6.5% of respondents expressed they were unsure about the business environment in 2025, whereas 7.9% felt uncertain about 2024.

Across the different regions, there was very little variation about business sentiment, although people in the South did tend to be a little more positive with more than 80% of them saying the economy would improve or stay the same. Western respondents, however, were more inclined to say the economy would decline with 19.3% reporting such.

When we broke down how respondents viewed the general business climate based on their primary area of construction, a couple of significant outliers quickly drew notice. First, was companies in the post frame segment were far less likely to see the business climate in 2025 as improving with only 5.9% reporting that, which was well below overall sentiment of 38.8% of respondents. Companies in the post frame segment not only didn’t expect improvement in 2025, 29.4% thought the business climate would decline.

Mark Stover, president, Perma-Column LLC, Ossian, Ind., doesn’t share that sentiment. He says he’s optimistic about 2025. “We have a lot of quotes going out,” he says. “Big ones.”

About half of respondents who said rollforming was their primary business looked for an improved business climate, and none of them expected any decline. When you add “improved” responses to “stay the same,” the survey takers in the cold-formed metal building segment (93.5%) and temporary or modular building segment (90.9%) were the most optimistic.

We also looked at the general business sentiment based on how large the company was. For the most part, larger companies (greater than $10 million gross sales in 2024) were more likely to say the economy would improve in 2025. Over 45% of them felt that. And smaller companies (less than $2 million in annual sales) were less inclined to see improvement with 34.5% of them feeling positive.

While the big companies were more likely to be optimistic, they were also more likely to be pessimistic. Respondents from companies with gross sales between $10 and $20 million felt the economy would decline in greater percentages (22.5%) than other cohorts.