Any building project that involves metal components will at some point require that metal to be manipulated. That’s where rollforming and metal forming come into place. Whether it’s being done on an industrial-grade machine on a factory floor or with a portable machine at the job site, at some point in the production process metal must be bent and formed into shape. Doing that requires precision and planning. New technologies are the driver of change in this sector of the industry.

Characteristics of the Rollforming and Metal Forming Industry

When we compared the markets served by companies engaged in rollforming from the 2024 CSI annual survey to the 2025 survey, we don’t find much of a difference. This year, we had 56 respondents in this category compared to 39 last year, and this year there were a far greater number of companies working the industrial market segment (39.7% compared to 5.4%). Otherwise, there wasn’t a lot of difference.

The largest percentage of respondents doing rollforming came from the Midwest and the West (both at 26.8%) but we did have a few from Canada (5.4%) and some of the survey takers (probably manufacturers) worked nationally (7.1%). Respondents from the South represented 21.4% of the survey takers engaged in rollforming.

Most of the respondents who were engaged in rollforming in 2024, fell in the builder or contractor (33.9%) category. Material dealers (25.0%) and manufacturers (21.4%) made up a larger percentage of companies in this section than in building types covered in the survey. That makes sense since the work covered in this section is specifically related to types of tools or machines more so than types of construction or building types.

Just over 30% of the respondents did about half of their work in new and half in remodel, but predominantly companies who were engaged in rollforming did new construction with 17.9% saying they did at least 90% of their work in new construction. Only 3.6% of survey takers said 90% or more of their work was remodeling, while 46.4% did at least 60% of their work in new construction.

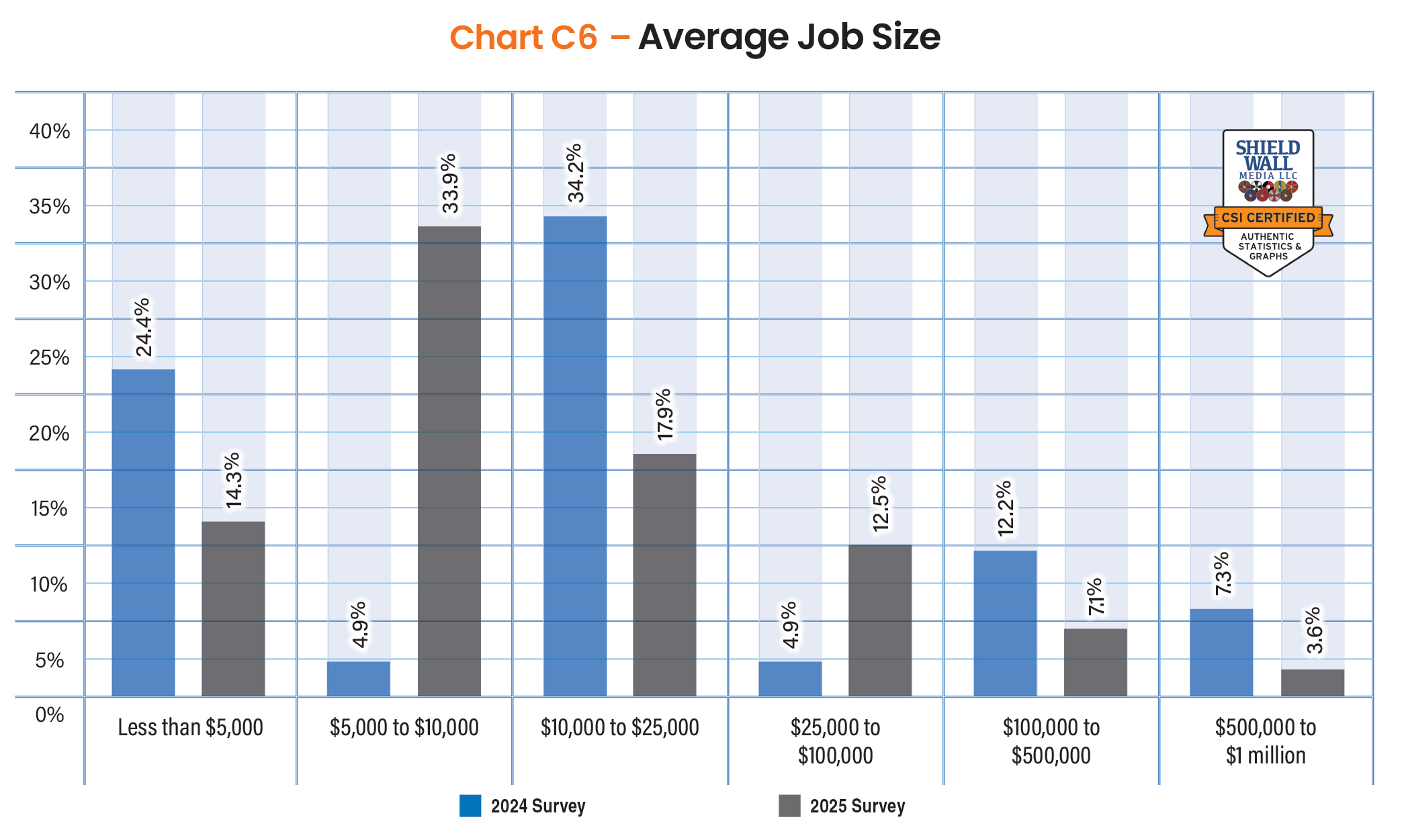

As with other sections of this report, there was a greater preponderance of companies doing smaller jobs this year compared to last year. In the 2024 report, 41.5% of survey takers had an average job size below $25,000. This year 58.9% reported average job size below $25,000, although there did seem to be a shift within the smaller jobs from the extremely small (less than $5,000) to those in the $5,000 to $10,000 range. It’s hard to get any construction project done for less than $5,000 so even a slight inflationary push would get those projects into the next cohort.

Companies doing rollforming who reported an average job size greater than $100,000 were almost identical in the 2024 survey (24.4%) to the 2025 survey (23.2%).

Projected Industry Growth

We asked companies engaged in rollforming activity how they felt the general business climate would be in the construction industry in 2025. More than half (57.1%) expected it to improve. Last year’s respondents were not quite as optimistic about 2024, when only 51.2% expected the construction economy to improve. The percentage who anticipated the following year’s construction economy would be poorer did decline from 2024 survey takers (12.2%) to 2025 (10.7%).

Of note, there seems to be a much greater certainty about the upcoming year. Only 1.8% of our respondents were unsure compared to 12.2% last year. That may have something to do with the presidential election, which always brings uncertainty, being decided.

When asked how specific market segments would perform in 2025, companies engaged in rollforming had very different ideas. The commercial market got the most positive attention with 57.2% of respondents expecting that market segment to grow in 2025.

The other three segments – residential, agricultural, and industrial – all had similar responses from companies engaged in rollforming. About 40% to 45% of survey takers thought those individual markets would increase in 2025 and between 41% and 48% expected them to hold their own.

Generally, about 10% of the respondents thought any given market would decline in 2025.

Company Size and Growth Projections

Englert is a company that distributes nationally, both machinery and finished metal products, giving them a comprehensive perspective on the industry. James Hazen, national roofing sales manager for the Perth Amboy, N.J.-based company says about 2024, “Despite some slowdown prior to the election in the economy, we continued to add new business, customers, products, and marketing efforts that resulted in year-over-year growth.”

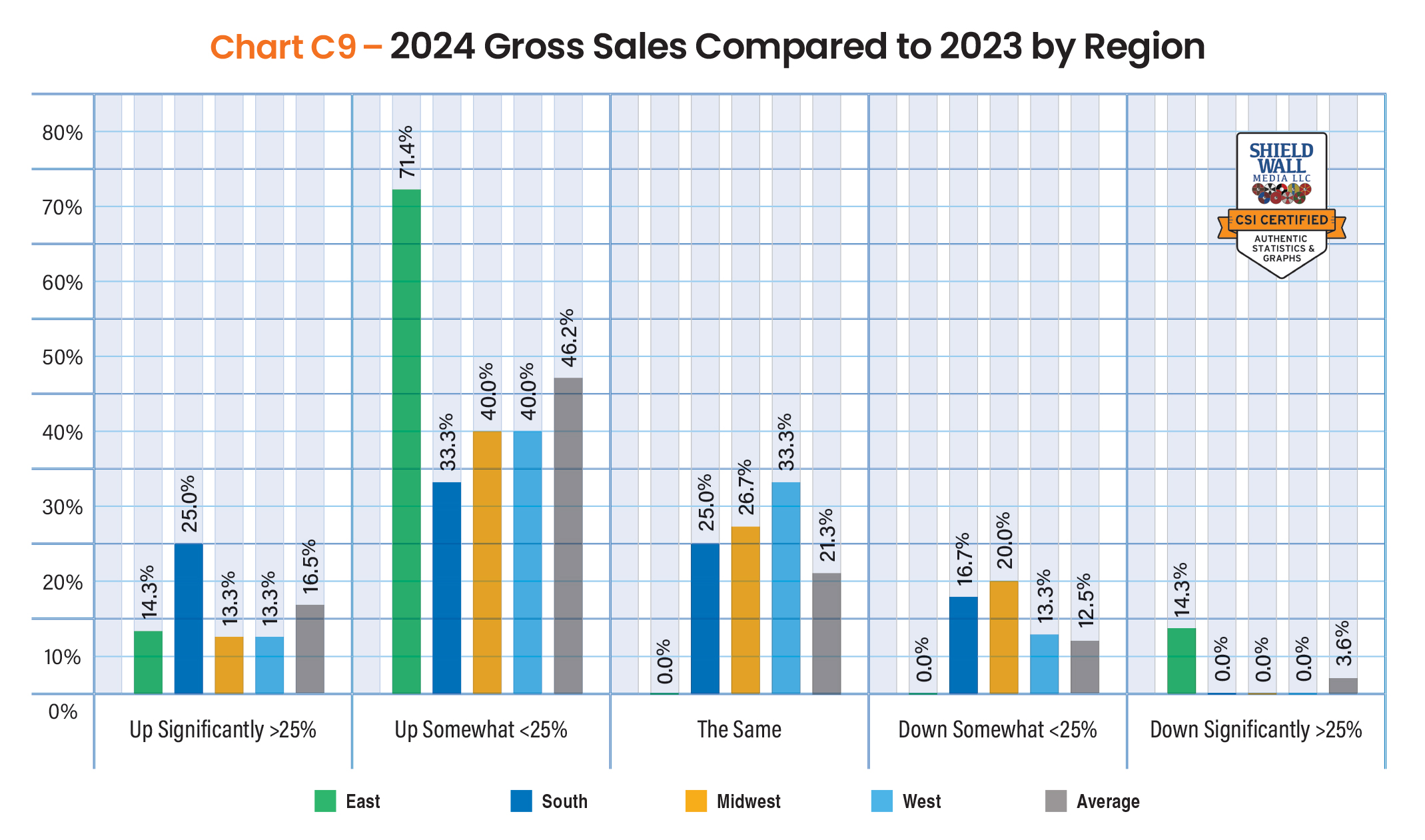

The total number of respondents who were engaged in rollforming was 56 for this survey, so analyzing information about specific regions, where participation can be slight, may lead to conclusions with a greater variability. That shows when we looked at the growth of gross sales, where survey takers in the East offered significantly different responses, so it’s important to keep an eye on the average growth.

On average, 62.7% of companies engaged in rollforming reported growth in 2024 and 16.5% of them said their growth was significant or greater than 25%. Respondents in the East were most likely to report gross sales increases. Only 16.1% of the companies reported a gross sales decline in 2024, and only companies in the East said they experienced a decline.

In 2024, 50% of the survey takers saw their gross sales increase year-over-year, and 10.7% experienced sales growth greater than 25%. On the other side of the ledger, 16.1% had declining gross sales last year, but only 1.8% said that decline was significant or greater than 25%.

In keeping with the general optimism of the construction industry, and the sense of confidence that comes after an election year, our respondents were optimistic about their company’s growth. More than two-thirds said the their gross sales would increase in 2025 and 21.4% expected the growth to be greater than 25%. A third of respondents (33.9%) said 2024 sales were the same year over year, and 21.4% projected them to stay the same in 2025.

Future Opportunities and Challenges

Companies engaged in rollforming have different expectations of expanding their business depending on what market segment they serve. Companies in the multifamily market were most likely to have plans to expand with only 2.8% of them saying they had no plans. But companies in the commercial (15.2%) and industrial (15.0%) sectors were less likely to have plans.

Single-family residential companies engaged in rollforming (48.2%) were more likely to plan to expand in 2025 than the other segments, but not by a significant amount. Companies doing agricultural work (36.0%) were least like to lay out plans for expansion in 2025.

When asked about resources they would add in 2025, companies engaged in rollforming addressed the labor shortage with 68.6% saying they would add support staff and 49.7% looking to add construction employees. Neither of those were surprising. The skilled labor shortage is well documented. Since these types of companies were less likely to have employees on the jobsite compared to companies such as metal roofing, the need for support staff would certainly outweigh the need for construction employees.

Companies engaged in rollforming also had their eyes on adding resources that might require capital investments, and that included manufacturing equipment (43.6%), metal forming equipment (43.2%), and trucks (36.1%). The more general category of capital equipment also got a nod from these companies with 41.2% saying they would add those resources in 2025.

Adding employees – support and construction – as well as investing in equipment could all help companies prepare to expand their businesses by offering additional products or taking on new building types. Among companies doing rollforming, 53.0% said they planned to add new products or building types in 2025.

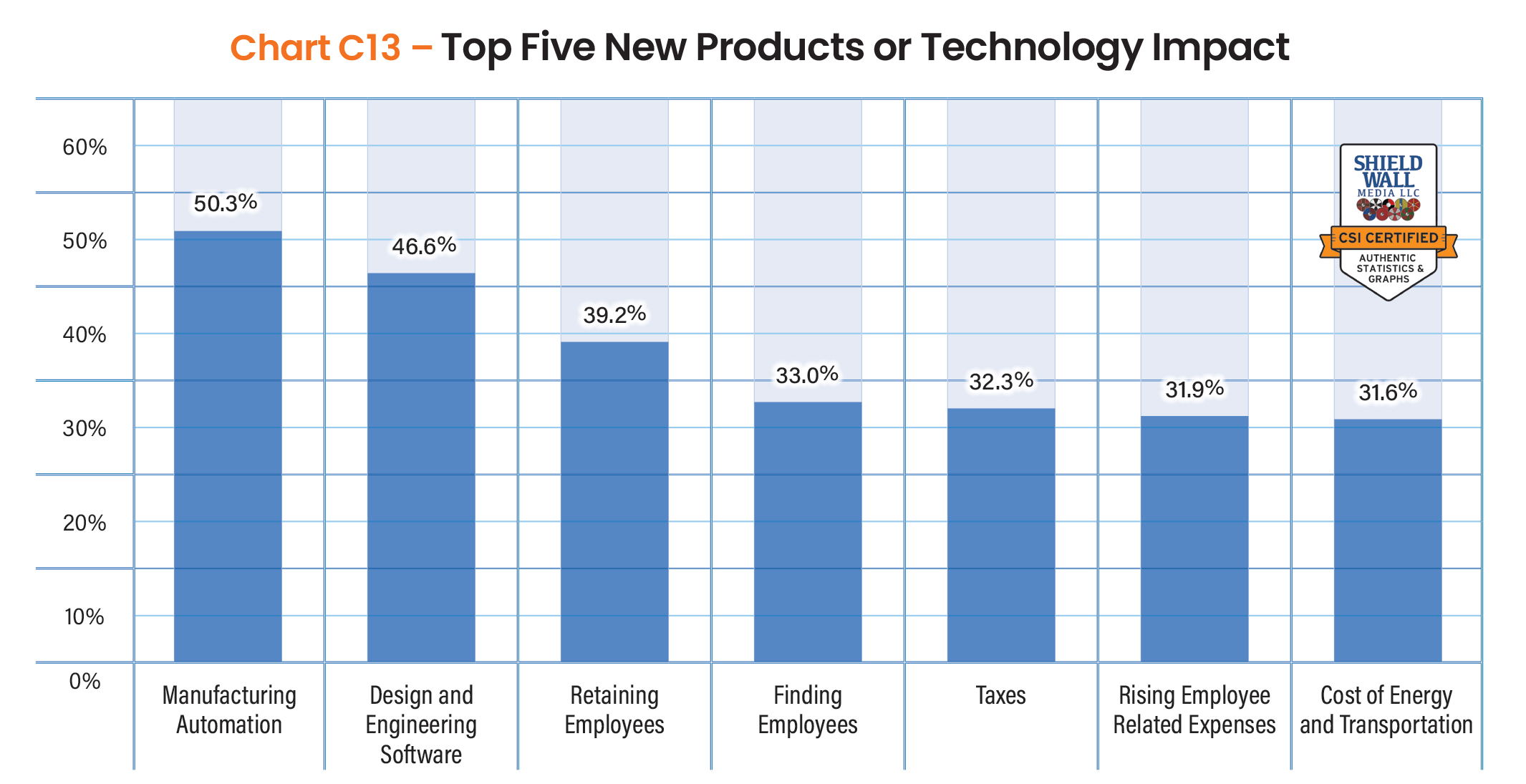

Companies that were engaged in rollforming were more likely to see manufacturing equipment (50.3%) as the innovation having the greatest impact on their businesses. Given that 21.3% of respondents in this section were manufacturers and 25% were material distributors that was not surprising. It was also not surprising that the innovation that took second spot in the impact on their businesses was design and engineering software with 46.6% of respondents reporting that.

Business management software (32.3%) and automation to save labor (31.6%) both relate to manufacturing automation and business efficiency. For companies engaged in rollforming, those innovations were among the most likely to impact their businesses.

Artificial intelligence (AI) continued to grab the attention of survey takers, and 39.2% of companies doing rollforming said it will impact their businesses. AI could be part of the manufacturing automation or manufacturing software. About a third of survey takers said those two innovations would have an impact.

In a bit of a one-off, the companies engaged in rollforming also identified structural material product (31.9%) innovations as likely to impact their business.

Companies engaged in rollforming were no different in their attitudes about the challenges of rising material costs than companies doing any other building type we surveyed. Almost three quarters (73.8%) said material costs would be a challenge for 2025.

Englert’s James Hazen says, “Uncertainty in the market, a new administration, new policies, and supply chain policies” are all challenges his company expects to face. All of those elements could have a negative impact on material costs.

In spite of that potential, Wayne Troyer, sales manager, Acu-Form, Millersburg, Ohio, was robust in his attitude about the prospects for 2025. His biggest challenge? “Not being able to produce machines fast enough,” he says. Increased demand and constraints on manufacturing space could combine to limit growth, and his comments speak also to the impact manufacturing automation will have on businesses.

It wouldn’t be a survey in the construction industry if one of the major challenges companies faced was finding (52.9%) and retaining (50.6%) employees. Even though far fewer respondents were likely to identify those challenges than rising material costs, still more than half of them said employee related issues would challenge their businesses.

Interest rates (41.2%) and inflation (40.0%) also made the top of our list of challenges for companies engaged in rollforming. Standing as a bridge between them and employee recruitment and retention challenges were concerns about rising employee expenses (49.5%).