Companies serving the rural construction market fill a unique niche in the construction industry. Agricultural buildings – often the mainstay of the rural builder – are different from commercial or other buildings. Contractors need to be more flexible and can’t specialize in one type of building or one type of customer. Architects often feel they are working with more utilitarian design concepts instead of high design.

The Shield Wall Media CSI annual survey looked at companies serving the rural builder market by focusing on companies engaged in single-family, multifamily, commercial, and agricultural construction. As is shown later, there is considerable crossover among these market segments within one company.

Characteristics of Rural Builders

We surveyed more than 550 designers, contractors, suppliers and manufacturers, and according to them, companies doing agricultural construction do post-frame buildings and cold-formed metal buildings at a much higher rate than other market segments.

Nearly 30% of agricultural construction companies do post-frame buildings (29.3%), which compares to the average across single-family residential, multifamily, and commercial companies of 20.5%. Companies engaged in single-family residential work were the least likely of the market segments to do post-frame buildings, clocking in at only 13.9%.

Looking at cold-formed metal buildings, again the companies engaged in agricultural construction were far more likely to execute this kind of construction (25.9%). The average across all market segments was only 15.5% with companies engaged in single-family construction the least likely to do cold-formed metal buildings (9.0%).

Interestingly, our respondents reported that those doing agricultural construction were less likely to do general roofing work (17.2%) than the other market segments, although they were the most likely to do metal roofing work (31.0%)

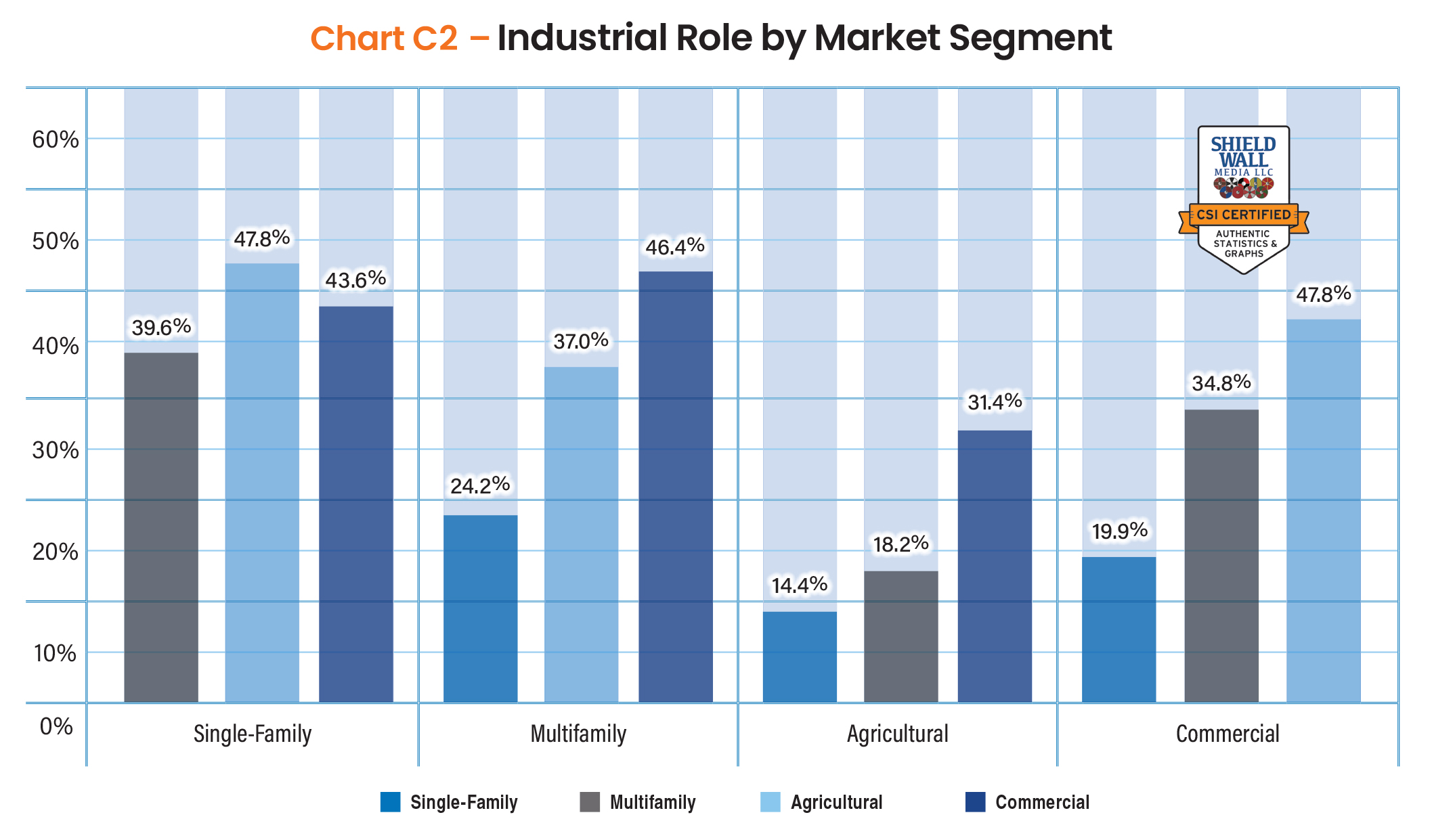

Obviously, a hundred percent of companies engaged in single-family construction do single-family work. But how much work do those companies do in the other market segments: multifamily, agricultural, and commercial.

This is the measurement of how flexible rural builders are. Single-family home builders are the least likely to do construction in other market segments. Only 24.2% of companies engaged in single-family construction do multifamily, and they are least likely to do agricultural construction (14.4%).

In contrast, companies engaged in agricultural construction were very likely to also do single family (47.8%), multifamily (37.0%), and commercial (47.8%). The same is generally true of the companies engaged in commercial construction. They participate at a 43.6% rate in single-family residential work, 46.4% in multifamily, and 31.4% in agricultural.

Of the four segments, the market segment other cohorts are least likely to participate in is agricultural. Single-family, multifamily, and commercial companies don’t make the leap to agricultural as much as agricultural companies make the leap to those other segments.

There are about 150 million existing housing units in the United States, which includes occupied and vacant properties. In 2024, we added about 1.5 million homes to that inventory, or about 1 percent of the total. The percentage of existing to new on the commercial side is even lower. So, it’s no wonder that the construction industry is gradually moving to more work being done on existing structures than new.

Shield Wall Media surveyed more than 550 people in the construction industry across all market segments. On average, only 7.4% of respondents said more than 10% of their work was on existing structures, but more than a fifth (21.2%) said more than 10% was new construction. An almost identical response came through for those doing between 60% and 90% of new construction (29.2%) and between 40% and 60% (29.0%) new work.

But when we looked at how that broke out by market segment, there were some more notable differences. Very few companies engaged in multifamily (4.3%) or agricultural (4.4.%) did less than 10% new construction. In fact, a total of 13.1% of companies engaged in agricultural construction reported doing less than 40% of their work in new construction. Nearly 60% of agricultural companies did more than 60% of their work in new construction.

Projected Industry Growth

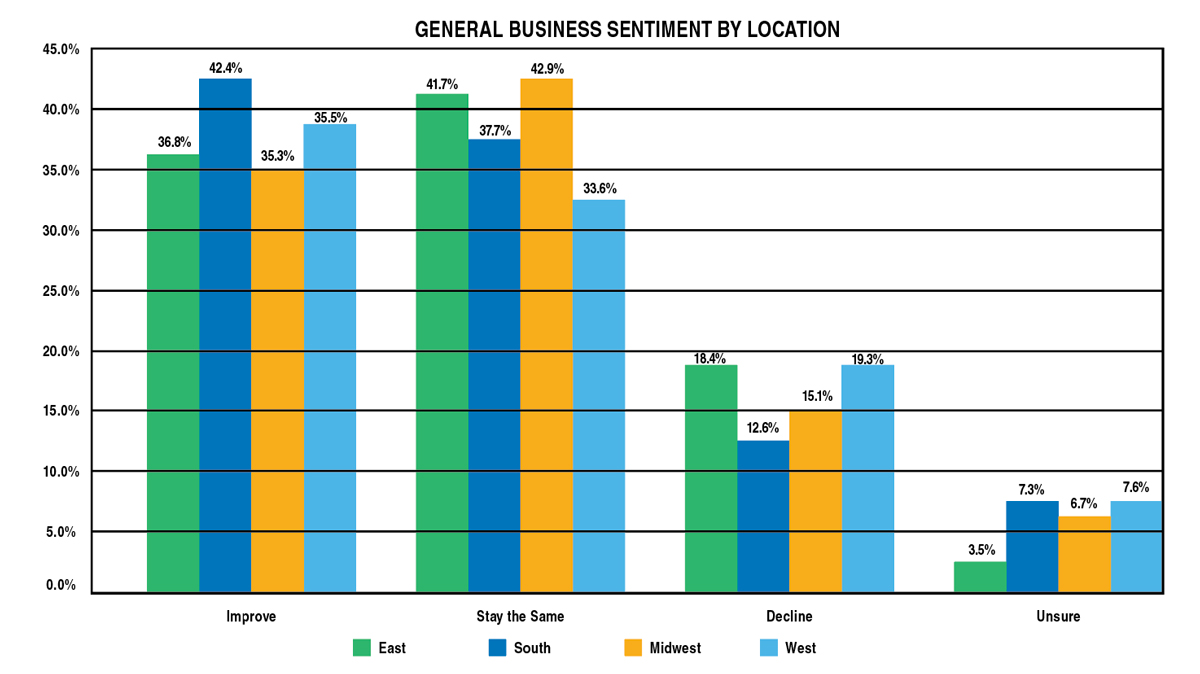

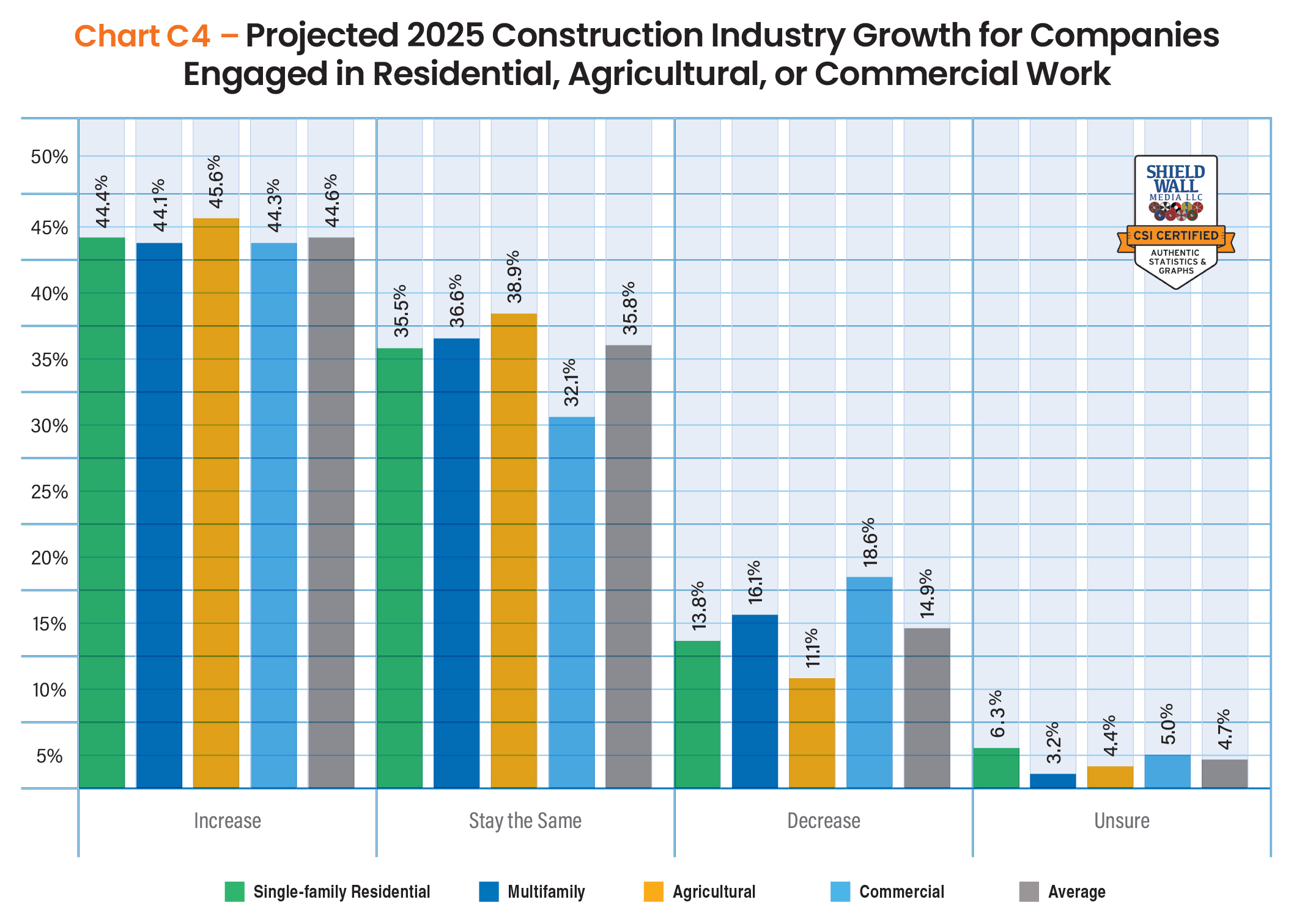

The general sentiment about the construction industry in 2025 was remarkably consistent among companies engaged in single-family residential, multifamily, agricultural, and commercial. All of those segments expected the general business climate across the construction industry to improve at the same rate—just around 45%.

Slight differences in attitude begin to show among those who think the general business climate might decrease. On average, 14.9% said it will decline, but 18.6% of companies engaged in commercial construction anticipated a decline where only 11.1% in the agricultural segment saw a decline across the construction industry.

We also asked survey takers how they thought individual market segments would perform in 2025. Of the more than 500 respondents who said they were engaged in single-family residential, multifamily, or commercial construction, most were least optimistic about the growth of the agricultural market (36.7%). More than half of the respondents thought that market segment would stay the same in 2025.

Survey takers were evenly split about the residential market, with just around 44% saying it would increase or stay the same. Also evenly viewed were the growth sentiments for residential (43.5%), commercial (43.7%), and industrial (40.5%) markets.

Company Size and Growth Projections

On average, about a third (34.7%) of the respondents in single-family, multifamily, agricultural, and commercial markets had revenues less than $2 million, and only about a fifth (21.8%) reporting gross sales greater than $10 million.

The biggest outlier was the in the single-family residential market segment, where nearly half of the survey takers said they had gross sales in 2024 below $2 million. There were a number of companies in the home improvement and handyman markets, who responded to the survey, which likely drove down the size of the companies reporting.

The companies reporting gross sales greater than $20 million were more likely to be companies working in the commercial or agricultural markets. It’s important to remember that included in these numbers are manufacturers, and in the agricultural market in particular, they may be driving the larger gross sales numbers.

Companies engaged in agricultural construction report that their gross sales increased significantly in 2024 compared to 2023 at a higher percentage (17.4%) than companies in single single-family residential, multifamily, or commercial market segments. But they also report at a lower rate that sales growth in 2024 was only up somewhat (less than 25%) in 2024.

When we added significant growth reporting to some growth reporting and compared them across all the market segments, the percentage of respondents identifying sales growth in 2024 was nearly the same. At the high end, 48.2% of companies engaged in single-family residential work said their gross sales increased year over year, and at the low end, 42.2% of commercial segment companies reported growth.

We averaged across all those market segments, and 45.2% of these respondents reported increased sales last year, 17.9% reported decreased sales, and 36.9% said sales held steady.

Befitting the general optimism within the construction industry, companies engaged in single-family residential, multifamily, agricultural, or commercial market segments anticipated gross sales increases in 2025. Commercial market companies were most robust with 54.3% expecting gross sales jumps and 13.6% of them said the increase would be greater than 25%.

Companies engaged in single-family residential work were most likely to expect significant declines but even that, at 5.3% of survey takers, was a relatively small percentage.

In last year’s survey, the companies engaged in agricultural work were much more volatile in their reporting. This year, with more than 550 survey participants – compared to 300 last year – that volatility seems to have decreased, and we are seeing more consistency across the board in this market segment.

Later, we’ll talk about challenges in this market, but one of the concerns being reported by many respondents is the issue of material costs. Paul Short, president of Combilift North America, points to the difficulty in predicting this as the potential for tariff increases. “Material prices could have an effect both positive and negative,” he says.

Future Opportunities and Challenges

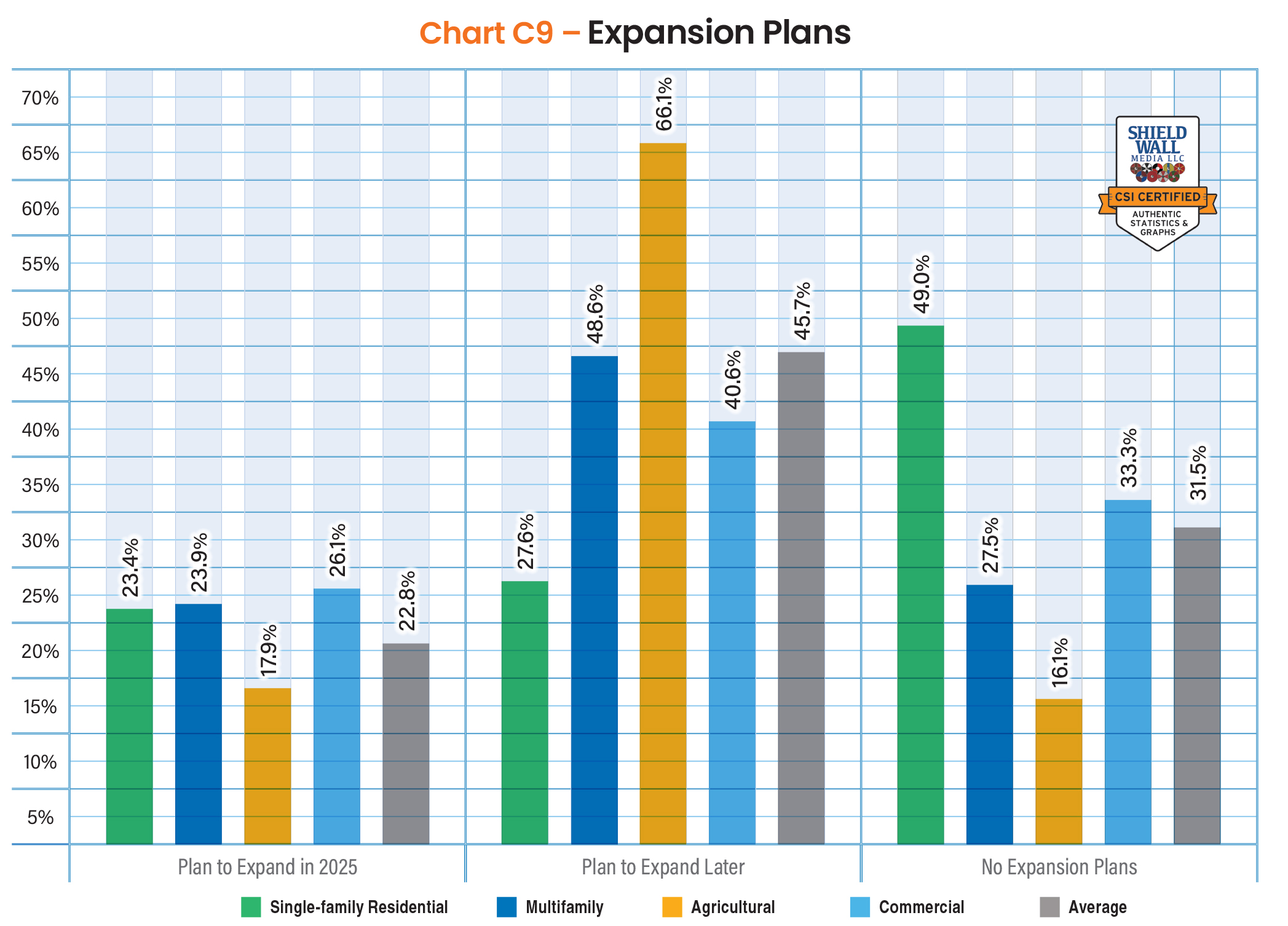

On average, 68.5% of companies expect to expand their operations at some point in the future, with 22.8% of them stating they intend to do so in 2025. The market segment most likely to have plans for expansion were companies engaged in the agricultural segment as 84% say they’ll expand, most (66.1%) pushing those plans to some point in the future.

The least likely to have expansion plans were companies engaged in the agricultural market segment. Only 16.1% said they had plans to expand. Considering that this market segment was the most likely to report a decline in sales in 2024, and least optimistic about growth in 2025, having expansion plans on the board seems a stretch.

Another measure of how optimistic companies were about the future of their market segment was the kind of resources they planned to add or increase in 2025. We offered a list of 12 options to survey takers. The top two were no surprise since adding employees is a perennial problem for companies in the construction industry as a whole, especially on the skilled labor side. In a bit of surprise, support employees tipped the chart just above construction employees, but only by a fraction. On average, 32.9% of respondents said they would add support employees in 2025, while 32.4% pointed to construction employees as a need.

Companies engaged on commercial construction (36.2%) were the most likely to need support employees, identical to the percentage who reported the need for construction employees. Single-family residential companies (36.4%) also pointed to the need for construction employees as their most important resource to add.

In the agricultural market segment, only 8.9% of respondents said they would add jobsite equipment in 2025, which is well below other market segments and the average of 18.1%. In a big contrast multifamily companies plan to add jobsite equipment at a 29.4% rate.

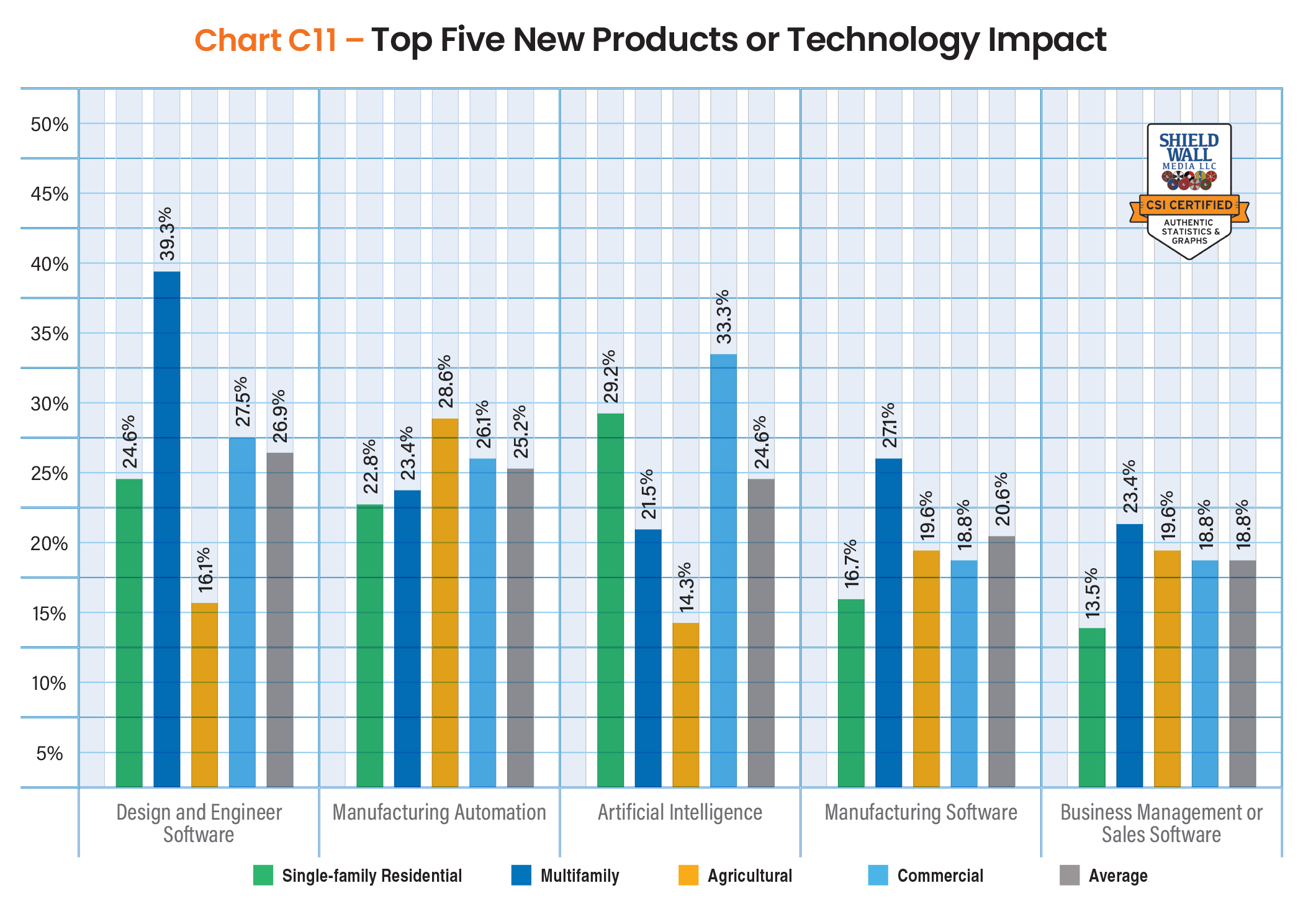

The five new technologies or products that companies engaged in single-family residential, multifamily, agricultural, or commercial thought would have the greatest impact on their businesses were design and engineering software, manufacturing automation, artificial intelligence, manufacturing software, and business management or sales software.

Technologies that didn’t scrape the top five included drones, 3D printing, and structural material products among others.

The biggest outlier was that 39.3% of multifamily companies identified design and engineering software as the technology most likely to impact them. But commercial companies identified artificial intelligence as having the greatest impact.

Paul Short of Combilift identified material costs and their variability as one of the main challenges his company expected to face in 2025. He was not alone. Of the more than 500 respondents to this question from the residential, agricultural, and commercial market segments, nearly half (49.1%) identified material costs as the biggest challenge for 2025.

Only companies engaged in agricultural construction (37.5%) responded at a rate lower than half. Those companies thought rising employee costs with 37.5% selecting that as the greatest challenge in 2005.

While nearly half of the companies, on average, identified material costs as the biggest challenge, the next highest percentage of companies (30.8%) engaged in residential, agricultural, or commercial construction believed inflation would be a challenge. That’s a 20 point gap between the most prevalent challenge and the next most prevalent.

Of course, many of the challenges identified impact material costs, such as inflation, rising employee costs, and interest rates, but that respondents overwhelmingly see material costs as the biggest challenge speaks to the focus on the problem the industry faces.